Survey

* Your assessment is very important for improving the work of artificial intelligence, which forms the content of this project

* Your assessment is very important for improving the work of artificial intelligence, which forms the content of this project

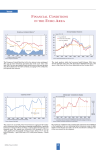

Trends EURO AREA INDICATORS The figures for aggregate euro area fiscal balances have been revised: The structural deficit remained unchanged in 2000, at 0.9% of GDP; the financial deficit actually declined from 1.3% in 1999 to 0.8% in 2000. Projections by the OECD for 2001 see the financial deficit increase to 1.2% of GDP as the result of the economic slowdown; the structural deficit is forecast to stay at 0.9% of GDP. In October, the seasonally adjusted unemployment rate remained unchanged compared to the previous month at 8.4% for the euro zone and at 7.7% for EU15. For both areas this is a decline from a year ago when it stood at 8.5% and 7.9% respectively. The lowest unemployment rates were achieved by the Netherlands (2.2% in September), Luxembourg (2.5%), Ireland (3.9%), Austria (4%), Portugal (4.3%) and Denmark (4.4%). At 12.9%, Spain continued to have the highest unem- CESifo Forum a) BIS calculations; to December 1998, based on weighted averages of the euro area countries’ effective exchange rates; from January 1999, based on weighted averages of bilateral euro exchange rates. Weights are based on 1990 manufactured goods trade with the trading partners United States, Japan, Switzerland, United Kingdom, Sweden, Denmark, Greece, Norway, Canada, Australia, Hong Kong, South Korea and Singapore and capture third market effects. Real rates are calculated using national CPIs. Where CPI data are not yet available, estimates are used. The real effective exchange rate of the euro (1999Q1 = 100), based on the broad group and CPI, declined from 89.2 in January to 85.5 in June and then appreciated to 89.3 in September. In October it weakened again to 89.2. It seems to have truly recovered from the low levels of 2000, when it had reached 82.2. The annual rate of inflation for the euro zone is forecast at 2.1% in November. This would be a continuation of the decline which started from the peak of 3.4% reached last May. Core inflation, which is not yet available for November had levelled off in October. 74