Survey

* Your assessment is very important for improving the work of artificial intelligence, which forms the content of this project

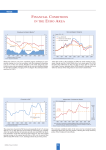

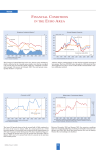

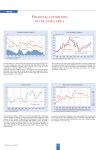

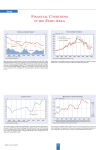

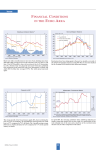

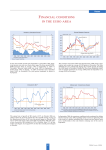

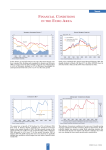

Trends FINANCIAL CONDITIONS IN THE EURO A REA The European Central Bank has left its key interest rates unchanged. The rate on main refinancing operations has stood at 2% since early June 2003. Ten-year government bond yields, however, did turn up again after their all-time low of 4.02% in March, averaging 4.39% in May. The yield spread thus widened. The stock markets, which had recovered until February 2004, have moved sidewards since then. The broad Euro STOXX index lost a bit more in May than the Dow Jones Industrial and the German DAX. The annual rate of growth of the broad monetary aggregate M3 continued its downward trend, reflecting an ongoing normalisation of portfolio behaviour of money holders, involving a cautious shift towards long-term financial assets. The annual rate of growth of M3 declined to 5.6% in April, pushing the three-month moving average down to 6.1% for the period February – April 2004 from 6.4% in the period January – March 2004. The monetary conditions index continued the upward trend established at the beginning of the year, indicating further monetary easing. A slight decline of real interest rates and a rise in the real effective exchange rate of the euro caused this development. CESifo Forum 2/2004 48 Trends EU SURVEY RESULTS Euro-zone and EU25 real GDP both grew by 0.6% in the first quarter of 2004, compared to the previous quarter, according to first estimates of Eurostat. Compared to the first quarter of 2003, GDP grew by 1.3% in the euro-zone and by 1.6% in the EU25, after 0.7% and 1.1% respectively in the previous quarter. Private consumption and exports accelerated, whereas investment and imports slowed down. The economic sentiment indicator for the EU rose by 1.2 points in May, reaching a level of 103.3. This improvement reflects primarily mounting confidence in the industry and services sector, which more than offset a slight dip in consumer sentiment. Economic sentiment improved strongly in the Czech Republic, Estonia, Latvia, Luxembourg, the Netherlands, Portugal, Sweden and the UK, while it dropped noticeably in Denmark, Greece, Ireland, Lithuania, Hungary and the Slovak Republic. * The industrial confidence indicator is an average of responses (balances) to the questions on production expectations, order-books and stocks (the latter with inverted sign). ** New consumer confidence indicators, calculated as an arithmetic average of the following questions: financial and general economic situation (over the next 12 months), unemployment expectations (over the next 12 months) and savings (over the next 12 months). Seasonally adjusted data. The assessment of order books had improved noticeably in April and remained unchanged in May (as did production expectations). Capacity utilisation increased marginally in the second quarter, from 80.5 to 80.6%. Industrial confidence in the EU continued its upward trend that had started in mid-2003, increasing by 1 point to a level of – 3. Behind the increase was a strong improvement in the assessment of stocks of finished goods. Luxembourg and the UK showed double-digit increases, whereas Hungary saw the most pronounced fall. Consumer confidence for the EU dipped slightly to – 13 after having remained unchanged at – 12 in the previous three months. Large improvements in consumer confidence were recorded in the Czech Republic, Hungary and Poland, whereas Estonia experienced a big drop. 49 CESifo Forum 2/2004 Trends EURO AREA INDICATORS The economic climate indicator for the euro area fell slightly in April after having risen five times in succession. Both, the assessments of the current situation and the outlook for the next six months contributed to the worsening. Nevertheless, the experts surveyed expect the economy of the euro area to grow by 1.7% in 2004 after a mere 0.4% in 2003. The euro was subject to relatively wide oscillations against the US dollar in May and early June. The euro initially appreciated against the dollar before depreciating rather sharply in the second week of May. In the second half of May and early June, however, following US data releases showing a further widening of the current account deficit in March, the euro more than regained its earlier losses. On 22 June it stood at $1.22. Euro-zone seasonally adjusted unemployment stood at 9% in April 2004, unchanged compared to March. It was 8.9% in April 2003. In April 2004, the lowest rates were registered in Luxembourg (4.2%), Ireland and Austria (4.5%) and the Netherlands (4.7% in March). The unemployment rate was highest in Spain (11.2%), followed by Germany (9.8%), France (9.4%) and Italy (8.5% in January). The Harmonised Index of Consumer Prices continued to rise in May 2004, to 2.5% from 2% in April. The continued rise in energy prices (prices of processed food remaining roughly stable) meant that core inflation rose only modestly from April to May. CESifo Forum 2/2004 50