Survey

* Your assessment is very important for improving the work of artificial intelligence, which forms the content of this project

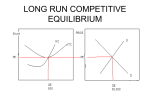

A Lecture Presentation in PowerPoint to accompany Exploring Economics Second Edition by Robert L. Sexton Copyright © 2002 Thomson Learning, Inc. Thomson Learning™ is a trademark used herein under license. ALL RIGHTS RESERVED. Instructors of classes adopting EXPLORING ECONOMICS, Second Edition by Robert L. Sexton as an assigned textbook may reproduce material from this publication for classroom use or in a secure electronic network environment that prevents downloading or reproducing the copyrighted material. Otherwise, no part of this work covered by the copyright hereon may be reproduced or used in any form or by any means—graphic, electronic, or mechanical, including, but not limited to, photocopying, recording, taping, Web distribution, information networks, or information storage and retrieval systems—without the written permission of the publisher. Printed in the United States of America ISBN 0030342333 Copyright © 2002 by Thomson Learning, Inc. Chapter 11 Monopolistic Competition Copyright © 2002 by Thomson Learning, Inc. 11.1 Monopolistic Competition Many goods and services are traded in circumstances that contain elements of both monopoly and competition. Theories of monopolistic competition and oligopoly deal with markets that lie between the extreme cases of perfect competition and monopoly. Copyright © 2002 by Thomson Learning, Inc. 11.1 Monopolistic Competition Monopolistic competition is a market structure where many producers of somewhat different products compete with one another. Copyright © 2002 by Thomson Learning, Inc. 11.1 Monopolistic Competition Monopolistic competition has features in common with both monopoly and perfect competition. Like monopoly, individual sellers believe that they have some market power. Unlike monopoly, there are many close substitutes coming from other monopolistically competitive firms. Copyright © 2002 by Thomson Learning, Inc. 11.1 Monopolistic Competition Firms in monopolistically competitive markets recognize the existence of competitors. They impose a limit on the prices they can charge and still sell a particular level of output. But they do not consider competitors as rivals who are watching them closely. Copyright © 2002 by Thomson Learning, Inc. 11.1 Monopolistic Competition Monopolistic competition is similar to perfect competition. the relatively free entry of new firms the long-run price and output behavior zero long-run economic profits However, the monopolistically competitive firm produces a differentiated product, which leads to some degree of monopoly power. Copyright © 2002 by Thomson Learning, Inc. 11.1 Monopolistic Competition In a sense, each seller in a market of monopolistic competition may be regarded as a “monopolist” of its own particular brand of the commodity Unlike a firm in the monopoly model, there is competition by many firms selling similar (but not identical) brands. Copyright © 2002 by Thomson Learning, Inc. 11.1 Monopolistic Competition The theory of monopolistic competition is based on three characteristics: product differentiation, many sellers, and free entry. Copyright © 2002 by Thomson Learning, Inc. 11.1 Monopolistic Competition Product differentiation is the accentuation of unique product qualities, real or perceived, to develop a specific product identity. With differentiation, buyers believe that the products of the various sellers are not the same, whether the products are actually physically different or not. Copyright © 2002 by Thomson Learning, Inc. 11.1 Monopolistic Competition Product differentiation leads to preferences among buyers to deal with particular sellers or to purchase the products of particular sellers. Sources of differentiation physical differences prestige considerations location service considerations Copyright © 2002 by Thomson Learning, Inc. 11.1 Monopolistic Competition When many firms compete for the same customers, any particular firm has little control over or interest in what other firms do. Copyright © 2002 by Thomson Learning, Inc. 11.1 Monopolistic Competition Entry in monopolistic competition is relatively unrestricted: New firms may easily start the production of close substitutes for existing products. Economic profits tend to be eliminated in the long run, as is the case in perfect competition. Copyright © 2002 by Thomson Learning, Inc. 11.2 Price and Output Determination in Monopolistic Competition Monopolistically competitive sellers are price searchers; they do not regard price as a given by market conditions. Because each firm sells a slightly different product, each firm’s demand curve is downward sloping, but quite flat (elastic) because of many close substitutes. Copyright © 2002 by Thomson Learning, Inc. 11.2 Price and Output Determination in Monopolistic Competition In perfect competition, each firm’s demand curve was horizontal because each firm, one of a great many sellers, sold the same homogenous product. Copyright © 2002 by Thomson Learning, Inc. 11.2 Price and Output Determination in Monopolistic Competition Given the position of an individual firm’s demand curve, we can determine short-run equilibrium output and price using a method similar to that used to determine monopoly output and price. The intersection of MR and MC curves indicates the short-run equilibrium output under monopolistic competition. Copyright © 2002 by Thomson Learning, Inc. 11.2 Price and Output Determination in Monopolistic Competition By observing the price on the demand curve at which that output can be sold, we then find the short-run equilibrium price. Copyright © 2002 by Thomson Learning, Inc. Short-Run Equilibrium in Monopolistic Competition MC P* C Total Profits ATC A B D P* Total Losses MR ATC A B C Price Price MC D MR 0 q* (Profit Maximizing Output) Quantity Copyright © 2002 by Thomson Learning, Inc. 0 q* (Loss Minimizing Output) Quantity 11.2 Price and Output Determination in Monopolistic Competition The three-step method for monopolistic competition is the same as for monopoly . . . Copyright © 2002 by Thomson Learning, Inc. 11.2 Price and Output Determination in Monopolistic Competition Find q* where MR= MC. Go up to the demand curve then to the left to find the market price. Go up from the profit-maximizing quantity to ATC. If TR > TC (P is greater than ATC), the firm is generating profits; if TR < TC (P is less than ATC), the firm is generating losses. Copyright © 2002 by Thomson Learning, Inc. 11.2 Price and Output Determination in Monopolistic Competition The short-run equilibrium situation, whether involving profits or losses, will probably not last long because there is entry and exit in the long run. If market entry and exit are sufficiently free, new firms will enter when there are economic profits, and some firms will exit when there are economic losses. Copyright © 2002 by Thomson Learning, Inc. 11.2 Price and Output Determination in Monopolistic Competition If existing firms are earning economic profits, new firms enter to take advantage of the economic profits; the demand curves for each of the existing firms will fall and become more elastic due to increasing substitutes. Copyright © 2002 by Thomson Learning, Inc. 11.2 Price and Output Determination in Monopolistic Competition This decline in demand continues until ATC becomes tangent with the demand curve, and economic profits are reduced to zero. Copyright © 2002 by Thomson Learning, Inc. 11.2 Price and Output Determination in Monopolistic Competition When monopolistically competitive firms are making economic losses, some firms will exit the industry; the demand curves for the remaining firms shift to the right and makes them more inelastic due to reduced substitutes. Copyright © 2002 by Thomson Learning, Inc. 11.2 Price and Output Determination in Monopolistic Competition The higher demand results in smaller losses for the existing firms until the losses disappear where the ATC curve is tangent to the demand curve. Copyright © 2002 by Thomson Learning, Inc. Price Market Entry and Exit in the Long Run MC ATC PLR = ATC MR 0 q* Quantity Copyright © 2002 by Thomson Learning, Inc. MC ATC PLR = ATC DSHORT RUN DLONG RUN MR 0 q* Quantity DLONG RUN DSHORT RUN 11.2 Price and Output Determination in Monopolistic Competition Long-run equilibrium will occur when demand is equal to average total cost for each firm at a level of output at which each firms’ demand curve is just tangent to its ATC curve. Copyright © 2002 by Thomson Learning, Inc. 11.2 Price and Output Determination in Monopolistic Competition The point of tangency will always occur at the same level of output as where MR = MC. At this equilibrium point, there are zero economic profits and no incentives for firms to either enter or exit the industry. Copyright © 2002 by Thomson Learning, Inc. Long-Run Equilibrium for a Monopolistically Competitive Firm Price MC ATC PLR = ATC DLONG RUN MR 0 Copyright © 2002 by Thomson Learning, Inc. q* Quantity 11.3 Monopolistic Competition Versus Perfect Competition Both monopolistic competition and perfect competition have many buyers and sellers and relatively free entry. However, product differentiation allows a monopolistic competitor the ability to have some influence over price. Copyright © 2002 by Thomson Learning, Inc. 11.3 Monopolistic Competition Versus Perfect Competition A monopolistic competitive firm has a downward-sloping demand curve, but it tends to be more elastic than the demand curve for a monopolist because of the large number of good substitutes for its product. Copyright © 2002 by Thomson Learning, Inc. 11.3 Monopolistic Competition Versus Perfect Competition Because of the downward slope of the demand curve, its point of tangency with ATC will not and cannot be at the lowest level of average cost. Therefore, even when long-run adjustments are complete, firms will not be operating at a level that permits the lowest average cost of productionthe efficient scale of the firm. Copyright © 2002 by Thomson Learning, Inc. 11.3 Monopolistic Competition Versus Perfect Competition The existing plant, even though optimal for the equilibrium volume of output, will not be used to capacity. That is, excess capacity will exist at that level of output. Copyright © 2002 by Thomson Learning, Inc. 11.3 Monopolistic Competition Versus Perfect Competition Unlike a perfectly competitive firm, a monopolistically competitive firm could increase output and lower its average total costs. However, increasing output to attain lower average costs would be unprofitable. The price reduction necessary to sell the greater output would cause MR to fall below MC of the increased output. Copyright © 2002 by Thomson Learning, Inc. 11.3 Monopolistic Competition Versus Perfect Competition Consequently, in monopolistic competition, there is a tendency toward too many firms in the industry, each producing a volume of output less than that which would allow lowest cost. Economists call this failing to reach productive efficiency—output production is not minimizing average total costs. Copyright © 2002 by Thomson Learning, Inc. 11.3 Monopolistic Competition Versus Perfect Competition In monopolistic competition, firms are not operating where P = MC. At the intersection of MC and MR, P > MC. This means that society is willing to pay more for the product (the price) than it costs society to produce it. The firm is not allocativally efficient, (where P = MC). Too many firms are producing at output levels that are less than full capacity. Copyright © 2002 by Thomson Learning, Inc. 11.3 Monopolistic Competition Versus Perfect Competition Perfectly competitive firms reach both productive efficiency (P = ATC at the minimum point on the ATC curve) and allocative efficiency (P = MC). However, these drawbacks in the monopolistically competitive market would be far greater in monopoly, where the demand curve is more inelastic (steeper). Copyright © 2002 by Thomson Learning, Inc. 11.3 Monopolistic Competition Versus Perfect Competition In monopolistic competition, the higher average costs and the slightly higher price and lower output may just be the price we pay for differentiated productsvariety. Just because we have not met the conditions of productive and allocative efficiencies, it is difficult to say whether or not society is better off. Copyright © 2002 by Thomson Learning, Inc. Comparing Long-Run Perfect Competition and Monopolistic Competition Price Price Minimum point of ATC MC Minimum point MC of ATC ATC ATC P = MR (Demand curve) P = MC P* MC DLONG RUN MR Excess capacity 0 q* Efficient Quantity Copyright © 2002 by Thomson Learning, Inc. 0 q* = Efficient Scale Quantity 11.3 Monopolistic Competition Versus Perfect Competition Perfect competition meets the test of allocative and productive efficiency and monopolistic competition does not. Copyright © 2002 by Thomson Learning, Inc. 11.3 Monopolistic Competition Versus Perfect Competition The significance of the difference between the relationship of long-run marginal cost to price in monopolistic competition and in perfect competition can easily be exaggerated. As long as preferences for various brands are not extremely strong, the demand for the products of firms will be highly elastic. Copyright © 2002 by Thomson Learning, Inc. 11.3 Monopolistic Competition Versus Perfect Competition Accordingly, the points of tangency with the ATC curves are not likely to be far above the point of lowest cost, and excess capacity will be small. Only if differentiation is very strong will the difference between the long-run price level and that which would prevail under perfectly competitive conditions be significant. Copyright © 2002 by Thomson Learning, Inc. The Impact of Product Differentiation Minimum point of ATC Price Price Minimum point of ATC ATC Excess capacity Excess capacity 0 q* ATC D D Efficient Scale Quantity Copyright © 2002 by Thomson Learning, Inc. 0 q* Efficient Scale Quantity 11.3 Monopolistic Competition Versus Perfect Competition Remember: The theory of the firm is like a road map that does not provide every possible detail, but gives us directions to get from one point to another. Any particular theory of the firm may not tell us precisely how an individual firm will operate, but rather will give us valuable insight into the tendencies of how firms will react to changing economic conditions. Copyright © 2002 by Thomson Learning, Inc. 11.4 Advertising Advertising is an important non-price method of competition that is commonly used in monopolistic competition. By advertising, firms hope to increase the demand and create a less elastic demand curve for their products, thus enhancing revenues and profits. Copyright © 2002 by Thomson Learning, Inc. 11.4 Advertising A successful advertising campaign can increase demand and decrease its elasticity by convincing buyers that a firm’s product is truly different. The result would be greater profits. The degree to which advertising impacts demand varies from market to market. Copyright © 2002 by Thomson Learning, Inc. Price The Impact of a Successful Advertising Campaign DAFTER ADVERTISING DBEFORE ADVERTISING 0 Quantity Copyright © 2002 by Thomson Learning, Inc. 11.4 Advertising Some have argued that advertising manipulates consumer tastes and wastes billions of dollars annually creating “needs” for trivial products, is sometimes based on misleading claims, and/or in itself, advertising requires resources, which raises average costs. Copyright © 2002 by Thomson Learning, Inc. 11.4 Advertising On the other hand, if one believes that people are rational and should be permitted freedom of expression, the argument against advertising loses some of its force. Copyright © 2002 by Thomson Learning, Inc. 11.4 Advertising While it is true that advertising can raise average total costs, it is possible that in situations where substantial economies of scale exist, average production costs may decline more than the amount of per-unit costs of advertising, by allowing firms to operate closer to the point of minimum cost on their ATC curve. Copyright © 2002 by Thomson Learning, Inc. 11.4 Advertising If the increase in demand resulting from advertising is significant, economies of scale from higher output levels may offset the advertising costs, allowing the firm to sell at a lower price. Toys R Us is an example. Copyright © 2002 by Thomson Learning, Inc. Average Total Costs Advertising and Economies of Scale C2 C Increase in cost due to advertising C0 C1 A B ATCAFTER ADVERTISING ATCBEFORE ADVERTISING 0 q0 q1 Quantity Copyright © 2002 by Thomson Learning, Inc. 11.4 Advertising Firms in monopolistic competition are not likely to experience substantial cost reductions as output increases. Therefore, they probably will not be able to offset advertising costs with lower production costs. Copyright © 2002 by Thomson Learning, Inc. 11.4 Advertising Even if advertising does add to total cost, it does convey information. Customers become aware of options in terms of product choice. It informs price-conscious customers about the cost of the product. Copyright © 2002 by Thomson Learning, Inc. 11.4 Advertising Advertising reduces information costs, so customers know about more substitutes. Consequently, this leads to increasingly competitive markets. Studies in the eyeglass, toy, and drug industries have shown that advertising has increased competition and led to lower prices in these markets. Copyright © 2002 by Thomson Learning, Inc.