Survey

* Your assessment is very important for improving the work of artificial intelligence, which forms the content of this project

Revenue management wikipedia , lookup

Consumer behaviour wikipedia , lookup

Natural gas prices wikipedia , lookup

Transfer pricing wikipedia , lookup

Yield management wikipedia , lookup

Dumping (pricing policy) wikipedia , lookup

Pricing science wikipedia , lookup

Gasoline and diesel usage and pricing wikipedia , lookup

Service parts pricing wikipedia , lookup

Pricing strategies wikipedia , lookup

Marketing channel wikipedia , lookup

Perfect competition wikipedia , lookup

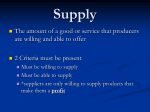

Entrepreneurship 3209 We have discussed the role played by the consumer Influence on Products Influence on Price Influence on Service Producer Consumer Marketplace Competition Pricing Power Customers Consumer Purchasing Power The amount of a good or service that consumers demand, the amount that suppliers can supply, & the price all affect one another. This is the relationship that we will now explore. Demand is the quantity of a good or service that consumers are willing & able to buy at a particular place Since each of us have different needs & wants and different levels of ability to pay for things, we each have different demands When we buy a particular good or use a particular service, we are expressing a demand for it Usually, consumers buy more as price decreases (increase demand) & buy less as price increases (decrease demand) law of demand: The economic principle that demand goes up when prices goes down; and, conversely, comes down when prices go up Consumer must be interested or aware of the good or service (advertising & marketing plays a role here) Enough of it must be available The price must be reasonable & competitive It must be accessible to the consumer (location, location, location) Changing Consumer Income Changing Consumer Tastes Changing Expectations for the Future Changes in Population usually an increase in income means people buy more.(cars, furniture, TVs) For some types of goods the opposite may be true Increased income may see a decrease in grocery items because people are buying more restaurant meals Changes in consumer tastes over time can cause an increase in demand for fashionable items & a decrease in demand for what is perceived as unfashionable Jean styles come in and go out of fashion regular intervals if prices or income are expected to increase consumers may purchase more now in anticipation Upward change in expectations = increase demand Reverse is true if the is a decrease in expectations (demand will decrease). Population increases creates need for more houses, roads, cars, services, etc We also find that as certain segments of the population increases certain things increase in demand. (Seniors in Canada are creating a demand for health care, retirement homes, certain sporting activities such as golf, etc ) If the goods & services consumers demand can be provided at prices they are willing to pay, businesses will supply them Supply: The quantity (amount) of a good or service that producers can provide determined by the costs of producing it and by the price people are willing to pay for it Law of Supply: The economic principle that supply goes up when prices goes up; and, conversely, comes down when prices come down The cost of producing it The price consumers will pay Changes in the Number of Producers Changes in Price Changes in Technology Changing Expectations for the Future Changing Production Costs An increase in producers will increase supply – if demand remains the same, price will drop! If price reduces then people may stop producing it. E.g. If cod prices fall, fishermen will catch other fish Changes in technology can reduce the cost of production, encouraging more businesses to start producing. E.g. CPU wafers, continually getting smaller and smaller and are able to produce more per wafer Many producers attempt to predict economic conditions and consumer demand for two to five years in advance. E.g. Automobile companies They increase or decrease supply accordingly If a local baker owner finds a lower cost for ingredients, they can produce more goods for the same cost. The opposite may be true as well, should the supplier increase costs Relating Price to supply and demand If demand is high while supply is low, prices tend to be high If demand is low while supply is high, prices tend to be low Relating Price to supply and demand The equilibrium price : When the quantity of goods that a producer is willing to supply at a certain price matches the quantity of goods that consumers are willing to buy at that price What would you do if a good or service that you use suddenly increases in price? Think about purchases to meet both needs and wants.