Survey

* Your assessment is very important for improving the work of artificial intelligence, which forms the content of this project

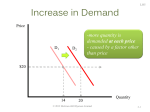

SAYRE | MORRIS Seventh Edition CHAPTER 3 Demand and Supply: an Elaboration © 2012 McGraw-Hill Ryerson Limited 3-1 Determinants of Supply and Demand Determinants of Demand Determinants of Supply Consumer preferences Prices of productive resources Consumer incomes Business taxes Prices of related products Technology Expectations of future prices, incomes, or availability Population: its size, income distribution, and age Distribution Prices of substitutes in production LO1 Future expectations of suppliers Number of suppliers © 2012 McGraw-Hill Ryerson Limited 3-2 Simultaneous Changes in Supply and Demand LO1 • Increase in both demand and supply leads to an increase in equilibrium quantity; price may rise or fall © 2012 McGraw-Hill Ryerson Limited 3-3 LO2 How Well Do Markets Work? Problems with markets: 1. Markets do not always adjust as quickly as we would like 2. Markets do not always produce equitable results 3. Competitive markets may not exist for some goods or services © 2012 McGraw-Hill Ryerson Limited 3-4 LO3 Price Controls Price Controls • government regulations to set either a maximum or minimum price for a product Price Ceiling • a government regulation stipulating the maximum price that can be charged for a product Price Floor • a government regulation stipulating the minimum price that can be charged for a product © 2012 McGraw-Hill Ryerson Limited 3-5 LO3 Price Ceiling • • • Used when present market price for a particular product is considered too high for many buyers The product is felt to be a necessity Example: rent control © 2012 McGraw-Hill Ryerson Limited 3-6 LO3 Price Ceiling • Price ceilings cause shortages © 2012 McGraw-Hill Ryerson Limited 3-7 LO3 Allocating Shortages • • • • The market (supply and demand) First come, first served Producers’ preferences Rationing © 2012 McGraw-Hill Ryerson Limited 3-8 LO4 Price Floor • • Used when present market price for a particular product is considered too low for producers Often used in agricultural markets © 2012 McGraw-Hill Ryerson Limited 3-9 LO4 Price Floor • Price floors cause surpluses © 2012 McGraw-Hill Ryerson Limited 3-10 LO4 Price Floor • Minimum wage laws can cause unemployment © 2012 McGraw-Hill Ryerson Limited 3-11 LO4 Dealing with Surpluses • • • • • Store it Convert it Sell it abroad at a reduced price (dump) Donate it Destroy it © 2012 McGraw-Hill Ryerson Limited 3-12 LO3 Quota • A quota, or restricting output, can raise price without causing a surplus © 2012 McGraw-Hill Ryerson Limited 3-13 LO5 Vertical Demand Curve • A vertical demand curve suggests that price does not matter • Same quantity is demanded no matter what the price • Some goods seen as necessities (eg, insulin) may have a perfectly inelastic (vertical) range • Eventually, quantity demanded decreases as income is insufficient to pay for the good © 2012 McGraw-Hill Ryerson Limited 3-14 Demand Curve Price Quantity • Price is irrelevant. • This product is a ultra-necessity. (cigarettes, drugs) • There is a maximum price for all of us. Our demand is limited by our income. © 2012 McGraw-Hill Ryerson Limited 2- 15 LO5 Upward Sloping Demand Curve • Upward sloping demand curves may be true for some individuals over a limited range of prices © 2012 McGraw-Hill Ryerson Limited 3-16 LO5 The Demand for Water • The effect of a change in supply depends very much on the shape of the demand curve © 2012 McGraw-Hill Ryerson Limited 3-17