Survey

* Your assessment is very important for improving the work of artificial intelligence, which forms the content of this project

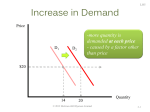

Expectations: The anticipations of consumers, firms, and others about future economic conditions. Expectations have a large effect on economic growth Expectations can become unmet due to shocks ©2013 McGraw-Hill Ryerson Ltd. Chapter 4, LO4 1 Shocks: Situations in which one thing is expected to occur but in reality something different occurs. Two types of shocks: demand shocks and supply shocks. Demand shocks: Sudden, unexpected changes in demand. Supply shocks: Sudden, unexpected changes in aggregate supply Economists believe that most short-run fluctuations are the result of demand shocks ©2013 McGraw-Hill Ryerson Ltd. Chapter 4, LO4 2 Price Flexible Prices $40,000 $37,000 $35,000 DM DH DL 900 LO5 ©2013 McGraw-Hill Ryerson Ltd. Chapter 4, LO4 Cars per week 6-3 3 Price Fixed Prices $37,000 DH DL 700 LO5 ©2013 McGraw-Hill Ryerson Ltd. 900 Chapter 4, LO4 1150 DM Cars per week 6-4 4 If the prices of goods and services could always adjust quickly to unexpected changes in demand, then the economy could always produce at its optimal capacity since prices would adjust to ensure that the quantity demanded of each good and service would always equal the quantity supplied. ©2013 McGraw-Hill Ryerson Ltd. Chapter 4, LO4 5 In reality, many prices in the economy are inflexible and do not change rapidly when demand changes unexpectedly. Manufacturing firms typically attempt to deal with unexpected changes in demand by maintaining an inventory Inventory : Goods that have been produced but remain unsold. If demand falls for many goods and services across the entire economy for an extended period of time, then many firms will find inventories piling up and will be forced to cut production resulting in recession, with GDP falling and unemployment rising. If, however, demand is unexpectedly high for a prolonged period of time, the economy will boom and unemployment will fall. ©2013 McGraw-Hill Ryerson Ltd. Chapter 4, LO4 6 Inflexible prices (sticky prices): Product prices that remain in place (at least for a while) even though supply or demand has changed. Flexible prices: Product prices that react within seconds to changes in supply and demand. ©2013 McGraw-Hill Ryerson Ltd. Chapter 4, LO4 7 Item Months Coin-operated laundry machines 46.4 Newspapers 29.9 Haircuts 25.5 Taxi fare 19.7 Veterinary services 14.9 Magazines 11.2 Computer software 5.5 Beer 4.3 Microwaves ovens 3.0 Milk 2.4 Electricity 1.8 Airline tickets 1.0 Gasoline 0.6 Source: Mark Bils and Peter J. Klenow, “Some Evidence on the Importance of Sticky Prices”, Journal of Political Economy, October 2004, pp 947-985, Used with permission of The University of Chicago Press. LO5 ©2013 McGraw-Hill Ryerson Ltd. Chapter 4, LO4 6-8 8 Companies selling final goods and services know that consumers prefer stable, predictable prices that do not fluctuate rapidly with changes in demand. In certain situations a firm may be afraid that cutting its price may be counterproductive because its rivals might simply match the price cut - a situation often referred to as a price war. ©2013 McGraw-Hill Ryerson Ltd. Chapter 4, LO4 9 Price stickiness moderates over time. If unexpected changes in demand begin to look permanent, many firms will allow their prices to change so that price changes (in addition to quantity changes) can help to equalize quantities supplied with quantities demanded. Prices go from stuck in the extreme short run to fully flexible in the long run. ©2013 McGraw-Hill Ryerson Ltd. Chapter 4, LO4 10