Survey

* Your assessment is very important for improving the work of artificial intelligence, which forms the content of this project

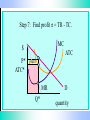

Monopoly Monopoly is a situation in which there is a single seller of a product for which there are no good substitutes. When a monopoly exists, there are generally high barriers to entry into the industry. What are the reasons for these barriers? (1) Legal Barriers patent - grant of an exclusive right to use a specific process or produce a specific product for a period of time (17 years in the U.S.) licenses and franchises - permission, granted by a government, to enter an industry or occupation (2) A single firm has sole control of a resource essential to an industry. (3) Economies of Scale Costs per unit in an industry may be low only when a firm produces a lot of output. Consequently, small firms will be unable to enter the industry because costs are too high. Market Demand Curve price Because the monopoly firm is the only seller of a good, the market demand curve for the good is the same as the demand curve for the firm’s product. Demand quantity Remember for a perfectly competitive firm: MR = P. This is not true for the monopolist. For a monopolist, MR < P. So the MR curve lies below the demand curve. Quantity 10 11 Price 20 19 TR 200 209 MR --9 Drawing the MR curve when the demand curve is a straight line: MR has the same Y-intercept and is twice as steep as the demand curve . $ MR Demand quantity Determining the optimal output and price, and the maximum profit: 7 Steps Step 1 a. Draw and label the axes. $ quantity Step 1 b. Draw and label the ATC and MC curves. $ MC ATC quantity Step 1 c. Draw and label the D and MR curves. MC $ ATC MR D quantity Step 2: Find the profit-maximizing output where MR = MC MC $ ATC MR Q* D quantity Step 3: Determine the price from the demand curve, above Q*. MC $ ATC P* MR Q* D quantity Step 4: Determine the cost per unit from the ATC curve, above Q*. MC $ ATC P* ATC* MR Q* D quantity Step 5: Determine the TR = PQ box. MC $ ATC P* ATC* MR Q* D quantity Step 6: Determine the TC = ATC . Q box. MC $ ATC P* ATC* MR Q* D quantity Step 7: Find profit p = TR - TC. MC $ P* ATC* ATC profit MR Q* D quantity In the previous set of graphs, the monopolist was earning a positive economic profit. It is also possible for the monopolist to have a loss or to breakeven. Let’s look at a monopolist with a loss. Step 1: Draw and label the axes and curves. (For a loss, the ATC curve must be entirely above D.) MC ATC $ AVC MR D quantity Step 2: Find the profit-maximizing (or lossminimizing) output where MR = MC MC ATC $ AVC MR Q* D quantity Step 3: Determine the price from the demand curve, above Q*. ATC MC $ AVC P* MR Q* D quantity Step 4: Determine the cost per unit from the ATC curve, above Q*. MC ATC $ ATC* P* AVC MR Q* D quantity Step 5: Determine the TR = PQ box. MC ATC $ ATC* P* AVC MR Q* D quantity Step 6: Determine the TC = ATC . Q box. MC ATC $ ATC* P* AVC MR Q* D quantity Step 7: Find profit or loss p = TR - TC. MC $ ATC* P* ATC AVC loss MR Q* D quantity A Monopolist Breaking Even (Zero Economic Profit) Step 1: Draw and label the axes and curves. (To break even, D must be tangent to the ATC curve.) MC $ ATC MR D quantity Step 2: Find the profit-maximizing output where MR = MC MC $ ATC MR Q* D quantity Step 3: Determine the price from the demand curve, above Q*. MC $ ATC P* MR Q* D quantity Step 4: Determine the cost per unit from the ATC curve, above Q*. MC $ ATC ATC* = P* MR Q* D quantity Step 5: Determine the TR = PQ box. MC $ ATC ATC* = P* MR Q* D quantity Step 6: Determine the TC = ATC . Q box. MC $ ATC ATC* = P* MR Q* D quantity Step 7: Find profit p = TR - TC. Since TR = TC, p = 0 MC $ ATC ATC* = P* MR Q* D quantity Monopoly Possibilities short run: positive profits, losses, or breaking even. long run: positive profits, or breaking even. What is bad about monopoly? Consumer options are limited. Profits do not signal firms to enter the industry. (They can’t get in because of the barriers to entry.) There is allocative inefficiency. ( P > MC ) The monopolist does not produce all units that consumers value more than it costs to make them. Allocative Inefficiency ( P* > MC* ) MC $ ATC P* ATC* MC* MR Q* D quantity Natural Monopoly a situation in which ATC declines continually with increased output. So a single firm would be the lowest cost producer of the output demanded. ATC doesn’t turn upward until a very high output level, beyond the amounts that consumers will buy. $ ATC quantity Remember: the MC curve is below the ATC curve when ATC is sloping downward. $ MC ATC quantity Draw the demand and MR curves. $ D MR MC ATC quantity What can the government do about a natural monopoly? government take over the industry let it operate freely government regulation of monopolist Natural Monopoly: operating freely $ D P* MR MC ATC Q* quantity Regulation marginal cost pricing (P = MC) average cost pricing (P = ATC) Natural Monopoly: marginal cost pricing regulation $ D MR MC Pm ATC Qm quantity Natural Monopoly: marginal cost pricing regulation $ D P < ATC Firm has a loss! So this won’t work. MR MC Pm ATC Qm quantity Natural Monopoly: Average Cost Pricing Regulation $ D MR Pa ATC MC Qa quantity Natural Monopoly: Average Cost Pricing Regulation Zero economic profits: this can work. $ D MR Pa ATC MC Qa quantity