Survey

* Your assessment is very important for improving the workof artificial intelligence, which forms the content of this project

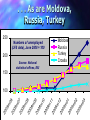

Financial crisis: Socioeconomic impact, political economy of response Ben Slay Senior economist UNDP Bureau for Europe and CIS 7 July 2009 Who’s the worst hit region? We are . . . 10% 9.8% 8.6% 5.4% 5.7% 6.3% 6.2% 2.5% 2.0% 3.3% 0% -1.5% -3.7% -5.1% -10% CIS SEE/NMS Latin America Regional GDP growth trends Africa Middle East Source: IMF World Economic Outlook, April 2009 2007 2009 Asia IMF forecasts for Caucasus, neighbouring economies 23.4% 25% 13.8% 8.1% 5.6% 11.6% 7.8% 4.5% 6.8% 4.7% 2.0% 1.1% 0% 1.0% -6.0% -5.1% Russia Turkey 2.5% 3.2% -5.0% 2007 -25% 12.4% Armenia 2008 2009 Georgia Azerbaijan Source: IMF World Economic Outlook, April 2009 Iran How bad is it? GDP reductions in 2009:Q1 0% -6% -6% -7% -6% -10% -5% -2.5% -4.5% -9% -12% -15%-14% -20% -25% -19% UKR LAT EST TUR LIT RUS SLO MOL ARM GEO SVK HUN EU Change relative to 2008:Q1. Sources: Eurostat, CIS Statistical Committee, national statistical offices, JPMorgan, press reports. US Why so bad? Trade shock: Russian, EU import trends 50% 43% 38% 27% 9% 7% Russia's CIS imports EU27 external imports 4% 0% -13% -6% -15% “Crisis hits home” -50% 2008:Q1 2008:Q2 2008:Q3 2008:Q4 -45% 2009:Q1 Year-on-year changes in imports, in value terms. Sources: Roskomstat, Eurostat. Unemployment: Baltics, Cyprus hard hit . . . 400 Numbers of unemployed (LFS data), June 2008 = 100 Lithuania 300 Estonia Latvia EU-12* Cyprus 200 EU-27 * Romania not included m 04 20 09 m 02 20 09 m 12 20 08 m 10 20 08 m 08 08 20 20 08 m 06 100 Source: Eurostat . . . As are Moldova, Russia, Turkey 250 Moldova Russia Turkey Croatia Numbers of unemployed (LFS data), June 2008 = 100 200 Source: National statistical offices, EIU 150 03 02 m Source: Eurostat 20 09 m 20 09 01 m 20 09 12 m 20 08 11 m 20 08 10 m 20 08 09 m 20 08 08 m 20 08 07 m 20 08 20 08 m 06 100 Crisis impact on Armenia 40% 24% 32% 7% 7% 0% -1% -14% -40% GDP -11% 2008 2009 -34% Trade turnover Monthly wage Registered ($) unemployment 2009 data are for January-May. Sources: National Statistical Service, UNDP calculations. What is to be done? Shortterm macro policy response G-20 countries: – Coordinated fiscal, monetary expansion Longer-term inflationary impact? – Keep global markets open, resist protectionism Fate of Doha Round? IMF, World Bank: – Preventing global financial contagion – Focus on Europe, Central Asia Coordination with EC, bilateral donors (including Russia) Actual policy responses in Europe, Central Asia Most countries unable to significantly boost domestic demand – Exceptions: Countries with reserve funds (Russia, Kazakhstan, Azerbaijan, Estonia) – Other must wait for trade to recover . . . and hope protectionism can be avoided Domestic policy: What can be done? – Better regulation of financial systems, to: Reduce capital outflows Prevent further demonetisation, dollarisation – Strengthen social policies, via: Increase share of GDP for social protection Better targeting of social protection Do social safety nets protect the poor? Social protection capacity 5.0% 100% Social protection (% of GDP) 4.5% % of poor covered 4.0% 90% 80% Source: World Bank. Social insurance (e.g., pensions) not included 3.5% 70% 40% 1.5% 30% 1.0% 20% 0.5% 10% 0.0% 0% P A G E TA LI T S R B C R O LA T R O M B EL R U S H U N 2.0% Z 50% O L B iH K O S A LB K FY AZ R O M M O L B U L A R M K YR U K R U ZB E ST 2.5% O 60% J 3.0% Social policy reform implications % of GDP devoted to social protection % of poor covered by social protection Below average Above average Below average Above average Weakest ability to protect: Biggest pay-offs to social policy reform: Albania, Armenia, Bulgaria, Georgia, Kazakhstan, Kyrgyzstan, Kosovo, Poland, Tajikistan BiH, FYR Macedonia, Ukraine, Uzbekistan Good at targeting; more resources needed: Best performers: Azerbaijan, Belarus, Latvia, Lithuania, Romania, Russia, Serbia Croatia, Hungary National crisis responses: Political economy issues Policy weaknesses: – Recognition lags – Implementation lags – Uncertain implementation capacity Policy fault lines: – Whom to protect? Key sectors and firms? Middle class? Most vulnerable? – Increase social benefits, or public works? Policy lags: Causes, implications Recognition lags: – Economics: Different points of business cycle Technical issue: Forecasts have been too optimistic – Politics: Electoral cycles, other factors Implementation lags: – Exchange rate policy: Devaluation works fastest . . . . . . But is not an option for many non-CIS countries – Monetary policy effectiveness limited by: Fixed exchange rates/euro adoption Deleveraging, dollarisation, demonetisation – Fiscal policy: Windows of opportunity? 2009 budget revisions—now 2010 budget formulation—2009:Q3 key Longer-term: Counter-cyclical responses to development challenges Environmental sustainability: – Climate change: Pricing energy correctly Tax carbon, not employment or value added – “Green jobs”: Alternative energy public works – Poverty and Environment Initiative (UNDP-UNEP) Food security: – Global food prices have bottomed out well above January 2007 levels, and are now rising again – Development opportunities for poor farmers? Demographics and migration: – Keep migration routes open; redress demographic imbalances in Russia, Europe, USA – Subject of UNDP’s 2009 Human Development Report Conclusion: Crisis implications for the region Break in economic growth: Stagnation or recession for most CIS economies Increases in: – Income poverty, inequality – Other dimensions of poverty Much development progress could be lost When growth resumes: – How strong will it be? – Will it be driven by: “Recovery” growth? Favourable external conditions? Reforms?