Survey

* Your assessment is very important for improving the work of artificial intelligence, which forms the content of this project

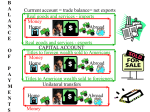

Migrants’ Transfers 1993 SNA para. 14.92 Current treatment (1) Personal effects: SNA para. 14.92/BPM5 says exports/imports, by implication offsetting entry is capital transfer. (2) Financial assets that are actually transferred to the new country of residence: BPM5 says financial account transaction and capital transfer entry. (3) Financial assets and liabilities that are not transferred: BPM5 says change of economy of residence is transaction; financial account and capital transfer entries. 2 Concerns Change of residence of owner seems more like a reclassification than a transaction. (Minor) effect of exports and imports on GDP by expenditure approach. 3 Question 1 Does the Group agree with the proposal not to record migrants’ personal effects under imports and exports of goods (and to amend SNA paragraph 14.92 accordingly)? The IMF Committee on Balance of Payments Statistics adopted the proposal that movements of personal effects should not be recorded as transactions. 4 Question 2 Would the Group like to clarify the recording of the changes in financial assets and liabilities due to changes in residence? If so, should the changes in assets and liabilities position of individuals who change their residence be recorded under “other changes in volume of assets”? The Committee adopted the proposal that other migrants’ transfers would be treated as other changes in assets. The Committee decided that no supplementary information on “classification changes due to change of residence” under “other changes in volume of assets” should be required. It was noted that the BPM5 term “Migrants’ transfers” assumes there is a transfer, so it would need to be changed.. 5 Question 3 Should the same principles apply to corporations that change their residence (either due to relocation or to boundary changes)? The Committee agreed that the principles established for individuals changing residence should also apply to corporations in the case of boundary changes or a single corporation that changed location, which could arise in the case of a societas europea. However, it noted that these cases would be exceptional, as most instances labeled as relocations actually involve assets being transferred to a new entity. The exceptional case was identified for societas europea (i.e., a company able to operate in any EU member country). 6 Question 4 Should clarifying text be added to SNA chapters 11 and 12, so that the special nature of these economic events is explicitly outlined? 7 8