Survey

* Your assessment is very important for improving the work of artificial intelligence, which forms the content of this project

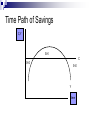

Intertemporal Approach to the Current Account GDP vs. GNP GDP is value of production/ value of income produced within a domestic economy. GNP is value of income earned by residents of domestic economy. GNP = GDP + NFP Net factor payments is income earned from overseas sources by domestic residents less income earned from domestic sources by overseas residents. Current Account The current account is, conceptually, the amount of income earned overseas less the amount of income earned by foreigners from the domestic economies: CA = NX + NFP. Current Account = Balance on Goods (Goods Exports-Goods Imports) + Balance on Services (Services ExportsServices Imports) + Net Investment Income (Investment Income Earned Overseas – Investment Income Paid to Foreigners) +Net Transfers (Donations from Overseas) Global Imbalance Current Account USA Japan China Taiwan Korea -0.06 -0.04 -0.02 0 0.02 % of GDP 0.04 0.06 0.08 0.1 Savings Private Savings is disposable income minus consumption spending. SP = (Y + NFP – T – C) Public savings is the budget surplus (T- G) Capital investment and the budget deficit can be financed by domestic savings or net borrowing from abroad. SP + KA = I + (G-T) Capital & Financial Account The capital account (more accurately the capital & financial account) records capital inflows into the country. The account includes the financial account, the capital account, and change in reserve assets. Capital & Capital Account Financial + Financial Account → Account= + Change in Reserve Assets (Debt Forgiveness, Patents) Direct Investment (FDI of Foreign Companies – FDI by Domestic Companies) + Portfolio Investment (Domestic Securities Purchases by Foreigners – Foreign Securities Purchases by Domestic Residents) + Other Investments (Deposits in Domestic Banks by Foreigners – Deposits in Foreign Banks by Domestic Residents) -Accumulation of Foreign Exchange Reserves Current Account = Negative of Capital Account S = Y + NFP – T – C +KA = I + (G-T) -KA = Y+NFP – I – C – G = [Y - I- C - G] +NFP Y = C + I + G + NX→ NX = [Y - I- C - G] -KA = NX + NFP Intuition: When you buy more from overseas than you earn overseas from exports or other income, you must borrow to make up the difference Hong Kong Current Account & Capital Account 2001 Net Goods Services Income Current Transfers Current Account Capital Account Credit -64970 133468 41175 -13878 95795 Debit 1488982 323087 384595 4719 2201383 -9155 Into HK Direct Investment Portfolio Investment Financial Derivatives Other Investment Change in Reserves Capital &Financial Account 1553952 189619 343420 18597 2105588 Abroad 96948 185424 88476 Foreign Holdings Holdings of of Hong Kong Foreign Assets Assets -322045 -9054 312992 39640 -100507 -140147 133783 -327414 -461197 -36530 -97359 Hong Kong had a 96 million dollar current account surplus in 2001. Hong Kong had a 97 million dollar capital & financial account deficit. The difference is reserve assets. Current account equals the accumulation of wealth Define Net International Investment Position, NIIPt, as a country’s foreign wealth less foreign owned domestic assets including stocks, bonds, real estate etc. NIIPt is end of period wealth accumulateds through current account. NIIPt – NIIPt-1 = CAt = NXt + NFPt Assume that NFP is real investment income (which for the most part is a reasonable assumption). NFPt = r∙NIIPt-1 NIIPt = (1+r)NIIPt-1 +CAt Wealth to GDP ratio Divide both sides of the wealth accumulation equation by Yt NIIPt NIIPt 1 CAt NIIPt 1 r NIIPt 1 CAt 1 r Yt Yt 1 Yt Yt 1 g Yt 1 Yt If current account (as a share of GDP) is below some level it will lead to a loss of wealth relative to GDP and if the ultimately increasing debt. 25 years of current account deficits means US external wealth has turned to deficit. USA 15.00% 10.00% % of GDP 5.00% 0.00% -5.00% 80 82 84 86 88 90 92 94 96 98 00 02 19 19 19 19 19 19 19 19 19 19 20 20 -10.00% -15.00% -20.00% -25.00% -30.00% NIIP CA Sustainable current account A large, perpetually negative current account is unsustainable as it would result in infinite debt. Sustainable current account is a current account that would maintain net international investment position at a constant level Define the sustainable current account npy npy cay NIIPt Yt NIIPt 1 Yt 1 (1 r ) (g r) npy cay npy 1 g 1 g Sustainable current account g>r r<g npy < 0 npy > 0 cay < 0 cay>0 High growth→, economy can keep borrowing without debt growing relative to GDP High growth →, economy must save a lot to keep its wealth high relative to GDP cay < 0, cay<0 High interest rates →, economy High interest rates →, economy can must save to pay interest on consume interest paymens from the debt. rest of the world. Determinants of the Current Account Current account is the gap between domestic savings and the domestic investment and the budget deficit. CA = S – I – (G-T) Examine the determinants of each in turn. Consider a firm considering in owning $1 worth of capital for 1 period. Cost: 1+r (Either borrow funds for 1 period or use own savings and lose chance to get savings. Benefit: Can produce MPK extra goods plus sell any of the capital that hasn’t depreciated Y MPK (1 d ) (1 d ) (1-d) Y Firm adds to profits if benefit is greater than MPKt 1 (1 d ) 1 r cost. Invest if: t 1 MPKt 1 r d t 1 t 1 Capital has diminishing returns, so MPK Y ΔY ΔK r+d K MPK K Different Growth Paths of Current Account Current Account 0.25 0.2 0.15 0.1 Korea 0.05 Taiwan 19 70 19 72 19 74 19 76 19 78 19 80 19 82 19 84 19 86 19 88 19 90 19 92 19 94 19 96 19 98 20 00 20 02 0 -0.05 -0.1 -0.15 % of GDP Investment Choice Increases profits to invest as long as MPK > r+d, but investing pushes down MPK. Investment will occur until MPK = r+d. Firms must invest until they reach target capital stock. Example: Cobb-Douglas MPKt 1 aKt 1a 1 (Qt 1 Lt 1 )1 a r d K t 1 1 Qt 1 Lt 1 r d 1 Kt 1 r d 1 It r d 1 1 a 1 1 a 1 1 a Qt 1 Lt 1 Qt 1 Lt 1 (1 d ) K t Volatile Investment Investment is the most volatile part of demand. A 1% change in technology or increase in employment will increase target capital stock. In any year, investment is one-tenth as large as the capital stock. A 1% change in the capital stock requires a 10% change in investment. Investment Curve r Q: Why does the curve slope down? The greater is interest rate, the more profitable capital must be to invest in it. Q: What shifts the curve? Increases in technology and labor increases profitability of capital. I (r ) I Investment high but falling in Japan and Korea, Investment high but increasing in China. Investment as a % ogf GDP 45 40 35 30 1990-1994 25 1995-1999 20 2000-2003 15 10 5 0 China Japan Korea, Rep. United States Savings high but falling in Japan and Korea, savings high but increasing in China. Savings as a % of GDP 45 40 35 30 1990-1994 & 25 1995-1999 20 2000-2003 15 10 5 0 China Japan Korea, Rep. United States Two Consumption Theories Keynesian: Consumption is dependent on current income. Permanent Income Theory: Consumption decision is a savings decision so households take into account future income as well as outstanding financial wealth. People prefer smooth consumption and save and borrow to do so. Why do People Save? Life Cycle Motives – Income is Not Smooth Across Time. Households save, in part, to transfer income from high income periods to low income periods. Precautionary Motives – Households like to achieve a buffer stock of wealth in the case of a possible bad outcome. If households have a buffer stock of saving, bad outcomes in terms of income don’t result in really bad outcomes in terms of consumption. Life Cycle Motives: Two Period Model To examine life-cycle theory, we use simplest possible model. One good consumed by a household that lives two periods, C0 and C1. Household lives and earns income Y0 and Y21 in each period. Household pays taxes in each period T0 and T1. Household can buy/sell bonds, B, at real interest rate r. Temporal Budget Constrants First period, B0 = Y0 – T0 – C0 Second period, C1=Y1 –T1+(1+r)B0 1) 2) Note B can be either > or < 0. If B > 0, household is a saver. If B < 0, household is a borrower. Intertemporal Budget Constraint C Y T 1 1 1 Combine two budget B constraints 1 r 1 r Present Discounted Value of Lifetime Income equals B Y0 T0 C0 Present Discounted Value of Lifetime Consumption. C1 C0 W 1 r Y1 T1 W Y0 T0 1 r Consider 3 scenarios Baseline Y1 = Y2 =YY implies 2 r Permanent Consumption Hypothesis C1=C2 1 r 1 r 2 r C [W ] Y Y 2r 2 r 1 r W Y Y 1 r 1 r Temporary Rise in Income The propensity to consume is a fraction of the temporary extra income. The remainder is saved for the future. Y 2r Y1 Y , Y2 Y W Y Y 1 r 1 r 1 r 1 r 2 r 1 r 1 r C W Y Y 2r 2 r 1 r 2 r 2r 1 r 1 S Y (Y ) 2r 2r Permanent Rise in Income The propensity to consume is larger when the increase in consumption is permanent. There is no need to save a permanent rise in income for the future. Y 2r Y1 Y , Y2 Y , W Y Y 1 r 1 r 1 r 2 r C W Y Y 2r 2 r 1 r S Y (Y ) 0 1 r Future Rise in Income Consumption may rise when future income increases which will also increase W. Savings will fall as people borrow to enjoy future income 2r today. Y Y , Y Y , W Y Y 1 2 1 r 1 r 2 r 1 r Y 1 r Y 2 r S Y (Y ) 2r 2r 1 r 1 r C W 2r 2r Permanent Income Hypothesis A simplified (and extreme) version of this theory hypothesizes that consumption is equal in each period. * C2 C C W C 1 r 1 r 1 r C [W ] 2r * 1 Income Stream & Consumption Consider three hypothetical increases in income of Δ. 1. 2. 3. A Temporary Increase – Y1 increase by Δ, but Y2 is unchanged. This will increase W by Δ. A Future Increase – Y2 increases by 100, but Y1 is unchanged. W increases by Δ /1+r≈ Δ A Permanent Increase – Y1 & Y2 increase by 100. W increases by Δ(2+r/1+r) ≈2∙ Δ Cases 1 & 2 increase W by nearly identical amounts. But current consumption depends only on W. Thus, cases 1 & 2 will increase C1* , C2* by similar amounts. Case 3 increases W by nearly double the amount. Income Stream and Savings In the first case, future income does not rise but optimal future consumption, C2* does . Current savings must rise. In the second case, current income does not rise, but optimal current consumption. Current savings must fall. What happens to savings with a permanent change in income? Application: Life Cycle of Saving Permanent Income Hypothesis suggests that households like to keep a constant profile of consumption over time. Age profile of income however is not constant. Income is low in childhood, rises during maturity and reaches a peak in mid-1950’s and drops during retirement. This generates a time profile for savings defined as the difference between income and consumption. Time Path of Savings C,Y S>0 C S<0 S<0 Y time East Asian Demographics During last 25 years, East Asian Nations had a sharp decrease in their ‘dependency ratio’. Dependency ratio is the % of people in their non-working years (children & seniors. Dependents are dis-savers and nondependents are savers. East Asian Demographics Due to plummeting birth rates, East Asia had a plummeting ratio of youths as a share of population This put a large share of population in high savings years. Share of prime age adults has hit its peak in most Asian countries and will fall over the next half century. China Hong Kong Indonesia Japan South Korea Malaysia Singapore Taiwan Thailand Change in Age Shares %Below 15 % Prime Age 20-59 1950-1990 2005-2025 -13.56 0.41 -20.64 NA -7.26 5.52 -16.72 -4.03 -18 -4.12 -7.7 7.5 -20.22 8.35 -18.82 NA -14.74 0.25 Interest Rates: Incentives and Effects A rise in interest rates increases the payoff to savings and increases the incentive to save. Substitution Effect (Plus Factor for All) A rise in the interest rate reduces the amount of savings you need to do to meet target level of future consumption. Income Effect (Minus Factor for Net Savers). A rise in the interest rate reduces the amount of borrowing you can do and still meet some target lever of future consumption. Income Effect (Plus Factor for Net Borrowers) Aggregate Savings & Interest Rates Interest rates have a positive impact on savings by borrowers, i.e. borrowers reduce their borrowing. Interest rates have an ambiguous effect on savings by savers. Since there is positive net savings, interest rates have ambiguous effect on aggregate savings. Empirically, impact of interest rates on savings are hard to detect. Saving Curve S (r ) r Q: Why does the curve slope up? Empirical work suggests substitution effect is slightly more powerful than income effect. Q: What shifts the curve? Changes in current income relative to future income. I (r ) I