Survey

* Your assessment is very important for improving the work of artificial intelligence, which forms the content of this project

Fear of floating wikipedia , lookup

Monetary policy wikipedia , lookup

Supply-side economics wikipedia , lookup

Great Recession in Russia wikipedia , lookup

Long Depression wikipedia , lookup

Interest rate wikipedia , lookup

Business cycle wikipedia , lookup

Inflation targeting wikipedia , lookup

Nominal rigidity wikipedia , lookup

Full employment wikipedia , lookup

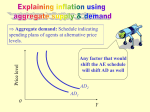

35 Extending the Analysis of Aggregate Supply McGraw-Hill/Irwin Copyright © 2012 by The McGraw-Hill Companies, Inc. All rights reserved. From Short Run to Long Run • Short run • Wages and other input prices don’t • LO1 change. • Upsloping aggregate supply Long run • Wages and other input prices fully flexible • Vertical aggregate supply. 35-2 From Short Run to Long Run • Production above potential output: • Price level increases. • Nominal wages eventually rise to maintain real wages (purchasing power). • Other input prices rise • Short run aggregate supply shifts left because costs are higher. • Return to potential output at a higher price level. LO1 35-3 Extended AD-AS Model Increased Demand -- Short Long Run Price Level LRAS AS2 AS 1 P3 c b P2 P1 a AD2 AD1 Qf Q2 Real Domestic Output LO2 35-4 From Short Run to Long Run • Production below potential output: • Price level decreases. • Nominal wages eventually fall to maintain real labor costs. • Input prices fall. • Short run aggregate supply shifts right because costs are lower. • Return to potential output at a lower price level. LO1 35-5 Extended AD-AS Model Long Run Run Decreased Demand - Short Price Level LRAS AS1 a P1 P2 P3 AS2 b c AD1 AD2 Q1 Qf Real Domestic Output LO2 35-7 From Short Run to Long Run So what is it about full employment that keeps bringing everything back here? Price Level ASLR AS1 a P1 AD1 Qf Real Domestic Output LO1 35-8 From Short Run to Long Run It’s the level of employment at which there is neither upward nor downward pressure on wages and input prices. Price Level ASLR AS1 a P1 AD1 Qf Real Domestic Output LO1 35-9 Extended AD-AS Model Demand-Pull Inflation Price Level ASLR P3 AS1 c b P2 P1 AS2 a AD2 AD1 Qf Q2 Real Domestic Output LO2 35-10 Extended AD-AS Model Cost-Push Inflation Price Level ASLR AS1 c P3 P2 AS2 b a P1 AD2 AD1 Q2 Q f Real Domestic Output LO2 35-11 Extended AD-AS Model Recession Price Level ASLR P3 AS2 a P1 P2 AS1 b c AD1 AD2 Q1 Qf Real Domestic Output LO2 35-12 Inflation and Unemployment • Low inflation and unemployment • Fed’s two major goals • Compatible or conflicting? • Short-run tradeoff between inflation • • LO3 and unemployment Supply shocks cause both rates to rise No long-run tradeoff 35-16 The Phillips Curve • Demonstrates short-run tradeoff between inflation and unemployment Concept Empirical Data 7 6 5 4 3 2 1 0 0 1 2 3 4 5 6 Unemployment Rate (Percent) LO3 7 Annual Rate of Inflation (Percent) Annual Rate of Inflation (Percent) Data for the 1960s 7 69 6 5 68 4 66 67 3 65 2 1 64 63 62 61 0 0 1 2 3 4 5 6 7 Unemployment Rate (Percent) 35-18 The Phillips Curve Annual rate of inflation (percent) 14 13 12 11 10 9 8 7 6 5 4 3 2 1 Unemployment rate (percent) LO4 35-19 The Long-Run Phillips Curve PCLR Annual Rate of Inflation (Percent) 15 PC3 12 b3 PC2 9 a3 b2 PC1 6 c3 a1 c2 b1 3 0 a2 3 4 5 6 Unemployment Rate (Percent) LO4 35-20 The Phillips Curve • No long-run tradeoff between inflation and unemployment • Short-run Phillips curve • Role of expected inflation • Long-run vertical Phillips curve • Disinflation LO4 35-22 Taxes and Aggregate Supply • Supply-side economics • Tax incentives to work • Tax incentives to save and invest • The Laffer curve Tax Rate (Percent) 100 n m Laffer Curve m l Maximum Tax Revenue 0 Tax Revenue (Dollars) LO5 35-24 Taxes and Aggregate Supply • Criticisms of the Laffer curve • Taxes, incentives, and time • Inflation and higher real interest • LO5 rates • Position on the curve Rebuttal and evaluation 35-25 Taxes and Real GDP • New findings suggest tax increases • • • LO5 reduce real GDP (Romer and Romer, 2008) Positive output shocks raise tax revenues Difficult to separate the effects of tax changes from other effects Investment falls sharply in response to tax changes 35-26