Survey

* Your assessment is very important for improving the work of artificial intelligence, which forms the content of this project

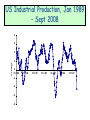

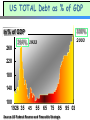

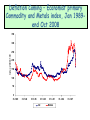

WORLD ECONOMIC CRISIS, DEFLATION, RECESSION AND THE COMING SHIFT IN THE BALANCE OF GLOBAL ECONOMIC POWER 1 OUTLINE • • • • Nature of crisis Sources of crisis Actual and future policy responses Prospects for the advanced countries • Prospects for the developing countries NATURE OF CRISIS General Nature of the Crisis • Financial • Economic • Global Financial crisis • Bursting of housing bubble • Liquidity crunch – shortage of cash • Credit crunch – lending activity ceases • Global crash of stock markets* • Collapse of major financial institutions Beginnings of an Economic Crisis and Recession • Fall in Industrial Production and GDP • Rise in unemployment • Collapse in consumer and business confidence US Industrial Production, Jan 1989 – Sept 2008 8 6 4 % change 2 0 31-1-89 -2 -4 -6 -8 31-1-92 31-1-95 31-1-98 31-1-01 31-1-04 31-1-07 SOURCES OF CRISIS Perceived Sources Of Problems • Burst housing bubble (sub-prime mortgages) which spilt over into other sectors • Greedy bankers and speculators (shorttraders) • Misguided policy makers The Actual Sources • Long business cycle – Long period increases and falls in economic growth, employment and inflation alongside rises and falls in profits, real wages, and interest rates – ….resulting from major changes in the technological base of production • Shift in global power LONG WAVE LONG CYCLE DATING trough 1790 1848 peak 1814 1872 1893 1917 1940 1975 2000 2030 trough duration hegemonic power technology 1848 58 Britain canals 1893 45 Britain railways, steam (steam engine) 1940 47 Britain steel, combustion engine, electricity, chemicals, telephone 2000? 60 United States electronics, plastics, aerospace, nuclear energy 2050 50 United States computers, biotechnology, robotics Source: Goldstein 1988 (modified) What Happens in The DOWNWAVE – i.e., 1980-Present • • • • • Rise of Neo-liberal/Neo-classical type ideology Fall in inflation* Fall in growth rates of advanced economies* Fall in interest rates Rise of financial sector and speculative activity – repeated “asset bubbles” (1)(2)* • Illusion of prosperity US Inflation Period Averages 19502007 12 10 percentage 8 6 4 2 0 1950-59 1960-69 1970-79 Williams 1980-89 Official 1990-99 2000-2007 US Long-Cycle Average Growth Rates: Official vs Williams 5 Williams Official 4 percentage 3 1.1% 2 2.6% 3.6% 1 0 1950-59 -1 1960-69 1970-79 1980-89 1990-99 2000-mid 2008 US TOTAL Debt as % of GDP 330% In % of GDP 2003 264% 1933 260 220 180 140 100 1926 35 45 55 65 75 85 95 03 Source: US Federal Reserve and Financiële Strategie Derivatives Growth Outstanding derivatives contracts As percentage of World GDP 1997 2007 $75 trillion $600 trillion 250% 1100% Source: Bank for International Settlements Relative Decline of The US Economy Using Published Data US share of world economy 60 50 percentage 40 30 20 10 0 1950 1960 1970 1980 1990 2000 2006 INTO THE NEXT LONG UPSWING? What Is Needed For The Upswing To Start And Progress? • • • • A major crisis and a shift in global economic power Destruction of debt (1) Elimination of excess capacity Restoration of productive profit rates from; – Lower costs of capital – Relocation of production to lower cost areas – Less competitive environment • Change in dominant economic thinking and policy making (towards Keynesianism) (2) • More transparency in and regulation of the financial system • Recognition and elimination (or at least reduction) of fraud in economic data computations (3) • New international financial system • New international trading system ACTUAL AND FUTURE POLICY RESPONSES Actual responses • Fixing the financial sector – Injections of liquidity (money) into the system (1) – Bail-outs of banks • Purchase of “toxic assets” (2) • Nationalisations and capital infusions • Guarantees of deposits – Talk about tightening financial regulation • Sharp reductions in interest rates Proposed Responses • More interest rate cuts • Massive increases in budget deficits (1)(2) • Bail-outs of certain sectors • “Nuclear option” (3) - Economist PROSPECTS FOR THE ADVANCED COUNTRIES Short-term (1-2 years) • More turmoil in the financial system – insurance companies and pension funds • Bankruptcies in the productive and non-financial service sector (1) • Fall in GDP to zero or below zero* • Rise in unemployment • Threat of deflation (2)* World Growth Forecasts Deflation Coming – Economist primary Commodity and Metals index, Jan 1989end Oct 2008 350 300 Index 2000=100 250 200 150 100 50 0 31-1-89 31-1-92 31-1-95 31-1-98 All 31-1-01 Metals 31-1-04 31-1-07 Longer-term (1) Stagflation (2) or Depression (3) PROSPECTS FOR THE DEVELOPING COUNTRIES (1) Short-term • Balance of payments and exchange rate weakness problems • Exchange rate/inflation vicious cycle • Sharp falls in economic growth • Worst affected will be those countries where Neo-liberal ideology still dominates policy making (1-3) Balance of Payments and US Dollar (and Yen) Shortage Problems Current account problems(1) • 80 developing countries have current account deficits of more than 5% of GDP • Turkey (-6.4%), Pakistan (-8.7%), South Africa (-7.7%), Bulgaria (-25%) Ukraine (-10%), Hungary (-5.5%), Poland (-4.9%), Baltic states (-6% to -15%) Swap facilities with US (2) • Brazil, South Korea, Singapore and Mexico Yen debt problems • Affecting South-East Asian countries that borrowed in Yen – so-called “carry trades” …..Possible Short-term Silver Linings • Benefit from expansionary policies in the advanced countries and richer developing countries • Relocation of capital from the advanced countries and high cost developing countries • Lower international borrowing costs The Long-term – Shift in Economic Power to The Non-OECD Countries • Non-OECD countries have more flexible production bases • Many developing countries will benefit from increases in primary product prices • Relocation of capital from advanced to developing countries • Increasing South-South cooperation • The rise of Asia and the advent of an Asian currency bloc • Hypocrisy of Neo-liberal development and stabilisation policy prescriptions become apparent The Long-term – The Potential Dangers • Policy makers still steeped in Neoliberal/Neo-classical thinking or jumping into Keynesian follies (1) • New development policy thinking – poverty alleviation and Aid-based infrastructure development • EPAs, Doha Multi-lateral trading round and Breton Woods II