Survey

* Your assessment is very important for improving the work of artificial intelligence, which forms the content of this project

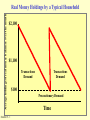

Chapter 19 The Demand for Real Money Balances and Market Equilibrium ©2000 South-Western College Publishing Real Money Balances •The quantity of money expressed in real terms •The nominal money supply, M, divided by overall price level, P, or M/P 2 Transaction Motive A motive for holding money based on the need to make payments 3 Precautionary Motive A motive for holding money based on a precaution against unforeseen developments 4 Average holdings of real money balances over the month Real Money Holdings by a Typical Household $2,100 $1,100 Exhibit 19 - 1 Transactions Demand Transactions Demand $100 Precautionary Demand Time 5 Benefits of Holding Real Money Balances The stream of services that real balances yield defined as time and distress saved by having money on hand for immediate use 6 How Households and Firms Decide What Amount of Real Balances to Hold The benefits of holding real money balances are: • To fulfill a stream of services related to having money available when needed, including not having to pay a brokerage fee to get money and not having to wait to get money • To be able to make payments when due Exhibit 19 - 2 7 Costs of Holding Real Money Balances The additional foregone interest that holding nonmonetary financial assets would have yielded 8 How Households and Firms Decide What Amount of Real Balances to Hold The costs of holding real money balances are: • The foregone interest that the nonmonetary balances of households and firms would have earned Decision Rule: • Hold real money balances as long as the benefits are greater than the costs Exhibit 19 - 2 cont. 9 A Demand Curve for Real Money Balances Interest Rate (percent) Demand Real Money Balances 10 Exhibit 19 - 3 Liquidity Preference A theory of the demand for money developed by John Maynard Keynes that results in an inverse relationship between the quantity of money demanded and the interest rate 11 Speculative Demand for Money The theory that individuals will demand to hold: •money when interest rates are low (bond prices high) to avoid capital losses when interest rates rise, and •bonds when interest rates are high (bond prices low) to capture capital gains when interest rates fall 12 Liquidity Trap When interest rates are very low (bond prices very high), the demand for money becomes perfectly horizontal and the economy is in a liquidity trap; the Fed is unable to lower interest rates by increasing the supply of money 13 A Demand Curve for Real Money Balances Interest Rate (percent) MS MS Liquidity trap Real Money Balances 14 What is real income? Nominal income divided by a price index 15 A Demand Curve for Real Money Balances Interest Rate Decrease in Demand Increase in Demand D' D D'' Real Money Balances 16 Exhibit 19 - 4 Factors That Affect the Demand for Real Money Balances An increase in … Will cause the demand for money to ... Income Increase Wealth Increase Payment Technologies Decrease Expected Inflation Decrease Risk of other Financial Assets Increase Liquidity of Other Financial Assets Decrease Exhibit 19 - 5 17 Factors That Affect the Demand for Real Money Balances A decrease in … Will cause the demand for money to ... Income Decrease Wealth Decrease Payment Technologies Increase Expected Inflation Increase Risk of other Financial Assets Decrease Liquidity of Other Financial Assets Increase Exhibit 19 - 5 cont. 18 Market Equilibrium in the Market for Real Money Balances Money Supply Interest Rate (percent) 6 A Demand Real Money Balances 19 Exhibit 19 -6 Market Equilibrium in the Market for Real Money Balances MS Interest Rate (percent) MS' Increase Decrease Real Money Balances Exhibit 19 - 7 20 Increases in the Supply of Real Balances MS MS' Interest Rate (percent) A B Demand Real Money Balances 21 Exhibit 19 -8 Expansionary Open Market Operations May Eventually Lead to Increases in Demand MS MS' Interest Rate (percent) A C D' B D Real Money Balances Exhibit 19 - 9 22 Other Changes Can Also Shift the Demand for Real Balances Curve MS Interest Rate (percent) D' D Real Money Balances Exhibit 19 - 10 23 Monetarism The school of thought that emphasizes the importance of changes in the nominal money supply as a cause of fluctuations in prices, employment, and output 24 Equation of Exchange M V = GDP = P Y 25 Velocity The number of times the money supply turns over during a year to mediate all the purchases of goods and services comprising GDP 26 Quantity Theory of Money The theory that velocity is stable or fixed and that changes in the money supply lead to proportional changes in GDP 27 Average Daily Holding of Funds •A household’s demand for real money balances during the month •The amount of each withdrawal divided by two 28 Average Daily Holdings of Funds Number of Broker Calls per Month and the Average Holdings of Real Balances (Transactions Demand for Real Balances) $2,000 Income = $2,000 / month Price level = 1 0 Calls to Broker $1,000 Exhibit 19 - 11 30 Days 29 Average Daily Holdings of Funds Number of Broker Calls per Month and the Average Holdings of Real Balances (Transactions Demand for Real Balances) $2,000 Income = $2,000 / month Price level = 1 1 Calls to Broker $1,000 $500 Exhibit 19 - 11 cont. 30 Days 30 Average Daily Holdings of Funds Number of Broker Calls per Month and the Average Holdings of Real Balances (Transactions Demand for Real Balances) $2,000 Income = $2,000 / month Price level = 1 2 Calls to Broker $666.67 $333.33 Exhibit 19 -11 cont. 30 Days 31 Benefits and Costs of Additional Calls to the Broker (A) = Transactions demand for money if call not made (B) = Transactions demand for money if call made Benefit = Interest on Additional bonds held Call (A) 0 $1,000 1 1,000 2 500 3 333 4 250 Exhibit 19 - 14 (B) -----$500 333 250 200 (A) - (B) -----$500 167 83 50 Benefit $2.50 .83 .43 .25 32 Benefits and Costs of Calls to Broker if the Interest Rate Increases to 1 % Per Month (A) = Transactions demand for money if call not made (B) = Transactions demand for money if call made Benefit = Interest on Additional bonds held Call (A) 0 $1,000 1 1,000 2 500 3 333 4 250 Exhibit 19 - 15 (B) -----$500 333 250 200 (A) - (B) -----$500 167 83 50 Benefit $5.00 1.67 .83 .50 33