Survey

* Your assessment is very important for improving the workof artificial intelligence, which forms the content of this project

* Your assessment is very important for improving the workof artificial intelligence, which forms the content of this project

Global financial system wikipedia , lookup

Real bills doctrine wikipedia , lookup

Great Recession in Russia wikipedia , lookup

Fractional-reserve banking wikipedia , lookup

Helicopter money wikipedia , lookup

Modern Monetary Theory wikipedia , lookup

Quantitative easing wikipedia , lookup

FINANCIAL SYSTEMS: HISTORY

AND THEIR ROLE

Hasan Ersel

HIGHER SCHOOL OF ECONOMICS,

MOSCOW

May 20, 2011

I. HISTORY OF FINANCE IN A NUTSHELL

THE BIRTH OF FINANCE

3000 BC: Banking originated in Babylonia: Temples

and palaces were used as safe places for the

storage of valuables. Initially the valuable that can

be deposited was only grain, but later cattle and

precious materials are also included.

In the Sumerian city Uruk in Mesopotamia

(population 10.000) trade was supported by lending.

Interest was paid.

“INTEREST” IN ANCIENT CULTURES

In Sumerian “interest” was mas, which also meant

calf.

In Greece and Egypt the words used for interest

(tokos and ms respectively) also meant “to give

birth”.

In these cultures interest indicates an increase in

something. They seem to consider it from lenders

point of view.

EARLY STATE INTERVENTION TO

FINANCE

• 2250-2150 BC: Cappadocian rulers guaranteed the

weight and purity of silver ingots.

• 1792-1750 BC : Reign of Hammurabi in Babylon (the

capital city of Babylonia). The famous Code of

Hammurabi

includes

laws

governing

banking

operations; e.g. Article 100 on the timely payment of

interest.

• The Babylonians, were accustomed to charge interest at

the rate of 20 per cent per annum. Nearly, if not quite, all

of their contract tablets show this rate of increase.

OLD TASTEMENT AND INTEREST

1300 BC: The Old Testament takes a negative attitude against

interest:

“25

If you lend money to any of my people with you who is poor, you shall not

be him as a creditor, and you shall not exact interest from him. “ The Old

Testament-Exodus 22(25), The Bible, Standard Version, New York:

William Collins, p. 67.

However the following quotation implies that taking

interest is forbidden among Jews, but Jews are allowed

to take interest from others (Gentile):

“19You shall not lend upon interest to your brother, interest on money,

interest on victuals [foodstuff] interest on anything that is lent for interest.

20To a foreigner you may lend upon interest , but to your brother you shall

not lend upon interest…” The Old Testament-Deuteronomy 23(19-20),

The Bible, Standard Version, New York: William Collins, p. 176.

WHY RECEIVING INTEREST FROM

GENTILE IS NOT PROHIBITED FOR

JEWS?

• The reason for the non-prohibition of the receipt by a

Jew of interest from a Gentile, and vice versa, is held by

modern rabbis to lay in the fact that the Gentiles had at

that time no law forbidding them to practice usury; and

that as they took interest from Jews, the Torah

considered it equitable that Jews should take interest

from Gentiles.

• Conditions changed when Gentile laws were enacted

forbidding usury; and the modern Jew is not allowed by

the Jewish religion to charge a Gentile a higher rate of

interest than that fixed by the law of the land.

INTEREST IN HEBREW

• In Hebrew, interest is neshek.

• It also means a bite… Something taken apart…

• In contrast to ancient civilizations “interest is

considered from borrowers point of view.

1200 BC-570 BC

• 1200 BC: Cowrie shell is used as “money” in China.

• 640-630 BC: Lydians started to use coin money. Lydia

was the first place where permanent retail shops

opened. [Herodotus mentioned the use of crude coins in

Lydia in an earlier date, i.e. 687 BC.]

• 600 BC: Pythius became identified as the first banker

that had records. He was operating both in Western

Anatolia and in Greece.

• 600-570 BC: Coin usage became widespread: (1)

Chinese started to use coins made of base metal. The

city-states (2) Aegina (595 B.C.), Athens (575 B.C.) and

Corinth (570 B.C.) started to mint their own coins

VIEWS ON INTEREST IN ANCIENT

GREECE

• 427-348 BC: Platon in his Laws (Book V;

paragraph 742) opposed receiving interest.

• 405 BC: First known statement of the Gresham

Law, i.e. bad money drives out good:

Aristophanes’ The Frogs

• 384-322 BC: Aristotoles in his Politics

(paragraph 1258) characterized interest as the

most unnatural category of earning.

INTEREST AND FINANCE IN ANCIENT

GREECE

• 350 BC: According to Demosthenes in Greece

the interest rate was 10% for ordinary business.

For risky business, such as shipping, lending

rates were between 20-30%.

• 200 BC: The Greek island Delos became the

first financial center.

THE VIEWS ON INTEREST IN THE

ROMAN EMPIRE

• Leading thinkers and statesmen, such as Marcus

Pocius Cato Censorius [Cato the Elder] (234 BC-149

BC) and Marcus Pocius Cato Uicensis [Cato the

Younger] (95 BC-46 BC) as well as Marcus Tallius

Cicero (106 BC-43 BC), Lucius Annaeus Seneca (4

BC-AD 65) and Masterius Plutarch (46 AD-120 AD)

were against usury.

• In Republican Rome (340 BC) interest was outlawed

altogether.[Lex Genucia reforms]

• Under the banner of Julius Caesar, a ceiling on interest

rates of 12% was set, and later under Justinian, it was

lowered even further to between 4% and 8%

JESUS CHRIST AND INTEREST

30 AD: Jesus Christ reacted against usury:

“And

Jesus entered the temple of God and drove out all

who sold and bought in the temple and overturned the

tables of the money changers and the seats of those

who sold pigeons. He said to them “It is written ’My

house shall be called a house of prayer’; but you make it

a den of robbers.”

The New Testament-Mathew 21(12-13), The Bible,

Standard Version, New York: William Collins, p. 21.

MONETARY POLICY IN ROME

• 250 AD: Silver content of Roman coins reduced down to

40%. Inflation in Rome…

• 295 AD: Gresham’s Law proves itself: The almost pure

silver coins issued by Aurelian were driven out by the

old, impure coins… Inflation accelerates…

• 301 AD: Emperor Gaius Aurelius Valerius

Diocletianus (244-311), [commonly known as

Diocletian], introduced direct controls on prices and

wages. This move defeated by markets… First

unsuccessful incomes policy experiment!…

• 305 AD: Diocletian introduced world’s first system of

annual budgets to Rome…

INFLATION AND THE FALL OF ROME

• 307 AD: The value of Denarii (the coin that was

introduced by Diocletian in 301 AD) declined to

half of its original value… One pound of gold is

100.000 Denarii…

• 324 AD: Inflation further accelerates in Rome:

One pound of gold is 300.000 Denarii…

• Then towards 350 AD Denarii loses its value

dramatically: one pound of gold 2 120 000 000

Denarii!!!

• 410 AD: Rome falls to the Visigots… (No wonder

why!!!)

KORAN’s ATTITUTE TOWARDS USURY

AD 610-632: Koran prohibits usury (riba):

“2: 275 Those that live on usury shall rise before Allah

like men whom Satan has demented by his touch; for

they claim that usury is like trading. But Allah has

permitted trading and forbidden usury…” Koran, AlBaqara,

2:275,

translated

by

N.J.

Dawood,

Hammondsworth, Middlesex: Penguin Books, 1974, p.

363.

HINDU AND BUDDHIST VIEWS ON

INTEREST-1

• Vedic texts of Ancient India (2,000-1,400 BC) in

which the “usurer” (kusidin) is interpreted as any

lender at interest. More frequent and detailed

references to interest payment are to be found

• In the later Sutra texts (700-100 BC), as well as the

also made detailed references to interest.

• Vasishtha, a well known Hindu law-maker of that

time, made a special law which forbade the higher

castes of Brahmanas (priests) and Kshatriyas

(warriors) from being usurers or lenders at interest.

HINDU AND BUDDHIST VIEWS ON

INTEREST-2

• In the Buddhist Jatakas (600-400 BC), usury is referred

to in a demeaning manner: “hypocritical ascetics are

accused of practicing it”.

• By the 2nd century AD, however, usury had become a

more relative term, as is implied in the Laws of Manu of

that time: “Stipulated interest beyond the legal rate

being against (the law), cannot be recovered: they call

that a usurious way (of lending)”

• The dilution of the concept of usury seems to have

continued through the remaining course of Indian history

so that today, while it is still condemned in principle,

usury refers only to interest charged above the prevailing

socially accepted range and is no longer prohibited or

controlled in any significant way.

FINANCIAL INNOVATIONS: PAPER

MONEY and FOREIGN EXCHANGE

CONTRACT

• 806-821 AD: In China, Emperor Hien-Tsung is

reigning… Shortage of copper causes emperor to issue

paper money… Chinese liked the idea.

• In 1032 AD there were 16 note-issuing houses in China.

Paper money increased so much that in 1166 China

went into hyperinflation…. In 1455 China abandoned

paper money.

• 1156: First foreign exchange contract: two brothers

borrowed 115 Genoa pounds and agreed to pay 560

bezants in Constantinople one month after their arrival to

the that city.

INTEREST IN CHRISTIANITY-1

• The Church, declared any extra return upon a

loan as against the divine law, and this

prevented any mercantile use of capital by pious

Christians.

• As the canon law1 did not apply to Jews, these

were not liable to the ecclesiastical punishments

which were placed upon usurers by the popes

• ------------------------1Canon

law is the body of laws and regulations made by or adopted by

ecclesiastical authority, for the government of the Christian organization and

its members. It is the internal ecclesiastical (of or relating to the Christian

Church or its clergy) law governing the Roman Catholic Church, the Eastern

and Oriental Orthodox Churches and the Anglican Communion Churches

INTEREST IN CHRISTIANITY-2

• Pope Alexander III, in 1179, having

excommunicated all manifest usurers.

• Christian rulers gradually saw the advantage of

having a class of men like the Jews who could

supply capital for their use without being liable to

excommunication, and the money trade of

western Europe by this means fell into the hands

of the Jews.

EARLY MODERN BANKING IN EUROPE

• Banking in the modern sense of the word can be

traced to medieval and early Renaissance Italy, to

the rich cities in the north like Florence, Venice and

Genoa.

• The Bardi and Peruzzi families dominated banking

in 14th century Florence, establishing branches in

many other parts of Europe.

MEDIEVAL BANKING IN EUROPE

• 1151 The first bank in Venice was established.

• 1255, Orlando Bonsignori formed a consortium

called the Gran Tavola ("Great Table"), which soon

became the most powerful bank in Europe.

• 1345 first bank was established in Geneva

• 1397 The Medici Bank (1397–1494) was created by

the Giovanni Medici in Florance, Italy.

XVth CENTURY DEVELOPMENTS IN

FINANCE (1)

• 1401: Bank of Barcelona founded.

• 1403: The lawyer and theologian Lorenzo di

Antonio Ridolfi won a legal case which led to

legalization of the interest payments by the

Florentine government.

• 1407: Fugars Bank is founded in Augsburg.

• 1407 The earliest known state deposit bank,

Ufficio di San Giorgio in Genoa (Casa di San

Giorgio) was established as a financial institution of

the Republic of Genoa

XVth CENTURY DEVELOPMENTS IN

FINANCE (2)

• 1444: Fatih Sultan Mehmet’s debasement of

“akçe”. He was the first Ottoman Sultan who used

debasement to raise public revenue. [see Pamuk

(1999; Chapter III)]

• 1472 Monte dei Paschi di Siena was established in

Siena, Italy. (Still Operating)

• 1494: First book on double entry bookkeeping is

published in Italy: It is Friar Luca Pacioli’s Summa

di Arithmetica, Geometrica, Proportioni et

Proportionalita…

XVIth CENTURY THOUGHT

ON FINANCE-1

• 1515: John Egk from Bologna University published a

thesis that advocated the freeing certain types of

interest. His research financed by the rulers of Augsburg.

Augsburg was competing with Florence in controlling

trade in that region. Egk was a student of Conrad

Summenhart who advocated the abandonment of

Aristotoles’ views on interest.

• 1526: Nicholas Copernicus published his Treatise on

Debasement. He argued that the buying power of

currency depends on the total number of coins in

circulation rather than the weight of metal they contain.

XVIth CENTURY THOUGHT

ON FINANCE-2

• 1536: John Calvin ended the discussion on

prohibiting interest by arguing that “If I buy a piece

of land, isn’t it still true that money will bear money?”

• [NOTE: Obviously any scholastic can challenge this idea

by pointing out that, what bears money is the land and

labor not money. John Calvin, anyway, won the case -not

because of his intellectual superiority but because of the

support he got from traders and his followers military

superiority] .

XVIth CENTURY DEVELOPMENTS

• 1542-1551: Henry VIII debases the coinage of

England

• 1545: Henry VIII legalizes interest charges on loans

(An upper limit of 10% per annum is set)

• The first English joint stock company is founded

• Queen Elisabeth I recalled the debased coins.

• 1585: Bank of Genoa founded

• 1587:

Banco della Piazza del Rialto, first

government bank in Europe, founded

• 1590 Barenbank was established in Hamburg (Still

operating)

XVIIth CENTURY-1

• 1615: Sir Lionell Cranfield and Mr. Wolstenholme

made the first balance of trade and balance of

payments calculations for England.

• 1661: Bank of Stockholm issued banknotes and

became first chartered bank in Europe to do so.

• 1668: Swedish Parliament established world’s first

central bank: Rikens Ständers Bank (today known

as Svierges Riksbank).

XVIIth CENTURY-2

• 1682:

Sir

William

Petty

published

Quantulumcuque Concerning Money that argues

development of banking is a major stimulus to the

English economy and world trade.

• 1694: Bank of England is established as a quasicentral bank.

XVIIIth CENTURY-1

• 1705: John Law published Money and Trade

Reconsidered and advocated the view that the

banknotes issued and managed by a public bank

would remove the brakes on the economy…

• 1729: Benjamin Franklin published Modest

Inquiry into Nature and Necessity of Paper

Currency. Following that publication, he was

awarded the contract for printing Pennsylvania Land

bank’s third issue of notes.

XVIIIth CENTURY-2

• 1762: Baring Bank was founded (When it went bankrupt

after a scandal in 1995, it was the oldest merchant bank

in Britain)

• 1768: Catherine the Great of Russia established two

state owned banks to finance the war against Ottomans.

The Assignat Bank was entrusted to issue paper money.

• 1776: Adam Smith, in his famous book The Wealth of

Nations defended paper money on the ground that it

stimulated business in Scotland and American colonies.

• 1781 The first American bank, Bank of North America,

was founded.

• 1792: The Dollar is adopted as the money unit in the

United States.

XIXth CENTURY-1

• 1800: Bank de France established as the central

bank of France.

• 1856: Bank-ı Osmani (Ottoman Bank) established.

• 1857: World wide banking crisis started in the USA

(contagion problem)

• 1863: Bank-ı Osmanii Şahane started to play the

role of a central bank

• 1873: The Great Depression in Britain (Continued

until 1885)

XIXth CENTURY-2

• 1875: Deutsche Reichsbank is established as

Germany’s central bank.

• 1882: Nippon Ginkō (Bank of Japan) was

established as Japan’s central bank.

• 1886: Ziraat Bankası was established. (Although

the date for the establishment of the Ziraat Bankası

is given as 1863 it is not exactly correct. That date

refers to the establishment of Menafi Sandıkları,

which were rather simple credit institutions for

farmers.)

• 1890: (First) Baring Bank crisis in England,

Uruguay and Argentina.

FIRST HALF OF XXth CENTURY-1

• 1913: U.S. Federal Reserve System was

established.

• 1923: Inflation in Weimar Germany reached to

3,25x106 %!

• On November 15, 1923 Rentenbank introduced a

new currency, Rentenmark (Security Mark), which

was equal to 1.1 trillion Papiermarks. The

Papiermark was pegged to US Dollar with a parity of

one US$ = 4,2 trillion Papiermarks! (It even climbed

up to 11,7 trillion papiermarks in French occupied

Cologne)]

FIRST HALF OF XXth CENTURY-2

• 1924: Reichmark became the legal tender in

Germany

• 1924: Türkiye İş Bankası was established.

• 1929: Great Depression

• 1930 Bank of International Settlements (BIS) was

founded

• 1931: On October 3, Türkiye Cumhuriyet Merkez

Bankası became operational.

POST II.WW DEVELOPMENTS-1

• 1944: Bretton Wood international monetary

agreements.

• 1947: International Monetary Fund became

operational.

• 1971: United States devalues dollar and gold

convertibility for all currencies ends.

• 1973: The US abandons the gold standard

• 1979: European Monetary System created

POST II.WW DEVELOPMENTS-2

•

•

•

•

•

•

•

1982: Mexican Debt Crisis

1985: Savings and Loan Association Crisis

1991: BCCI scandal- biggest banking fraud

1992: Maastrich Treaty

1994: Financial Crisis in Turkey

1995: Barings Bank fails for a second time.

1997: East Asian Financial Crisis

LAST DECADE-1

• 1998: Russian Financial Crisis

• 1999: Eleven European countries introduced Euro

as an accounting currency

• 2001: Turkish Financial Crisis

• 2002: Euro banknotes and coins are launched

LAST DECADE-2

• 2005: China emerged as a major player in the global

financial system

• 2006: Problems in the US Mortgage Market

• 2007: US Mortgage Crisis and Recession

• 2008-?: Global Economic Crisis

ON THE DANGERS OF BANKING!

"I believe that banking institutions are more

dangerous to our liberties than standing armies. If

the American people ever allow private banks to

control the issue of their currency, first by inflation,

then by deflation, the banks and corporations that

will grow up around the banks will deprive

the people of all property until their children wakeup homeless on the continent their fathers

conquered.“

Thomas Jefferson 1802

MACROFINANCIAL SYSTEM-1

Goods Market

Goods

Expenditure

Households

Firms

Factors Market

Labor

Wages

II. THE ROLE OF THE FINANCIAL

SYSTEM

MACROFINANCIAL SYSTEM-2

Goods Market

Goods

Expenditure

Households

Firms

Factors Market

Labor

Wages

Savings

Investment

MACROFINANCIAL SYSTEM-3

Goods Market

Goods

Expenditure

Households

Firms

Factors Market

Labor

Wages

Savings

Investment

Financial System

STRUCTURE OF THE FINANCIAL

SYSTEM

Financial Markets

Households

Firms

Banks

COMPONENTS OF FINANCIAL SYSTEM

1.

Money

To pay for purchases and store wealth

2.

Financial Instruments

To transfer resources from savers to investors and to transfer risk to those best

equipped to bear it.

3.

Financial Markets

Buy and sell financial instruments

4.

Financial Institutions.

Provide access to financial markets, collect information & provide services

5.

Central Banks

Monitor financial Institutions and stabilize the economy

FINANCIAL MARKETS

• Markets in which funds are transferred from

people who have an excess of available funds to

people who have a shortage of funds.

FUNCTIONS OF FINANCIAL MARKETS

• Perform the essential function of channeling

funds from economic players that have

saved surplus funds to those that have a

shortage of funds

• Promotes economic efficiency by producing

an efficient allocation of capital, which

increases production

• Directly improve the well-being of consumers

by allowing them to time purchases better

STRUCTURE OF FINANCIAL MARKETS

• Debt and Equity Markets

• Primary and Secondary Markets

– Investment Banks underwrite securities in primary markets

– Brokers and dealers work in secondary markets

• Centralized vs. and Over-the-Counter (OTC) Markets

• Money and Capital Markets

– Money markets deal in short-term debt instruments

– Capital

markets

deal

in

longer-term

debt

equity instruments

and

THE BOND MARKET AND THE INTEREST

RATE

• A security (financial instrument) is a claim on

the issuer’s future income or assets

• A bond is a debt security that promises to make

payments periodically for a specified period of

time

• Interest rate is the cost of borrowing or the price

paid for the rental of funds

THE STOCK MARKET

• Common stock represents a share of ownership

in a corporation

• A share of stock is a claim on the earnings and

assets of the corporation

INTERNATIONALIZATION OF FINANCIAL

MARKETS

• Foreign Bonds—sold in a foreign country and

denominated in that country’s currency

• Eurobond—bond denominated in a currency

other than that of the country in which it is sold

• Eurocurrencies—foreign currencies deposited

in banks outside the home country

– Eurodollars—U.S. dollars deposited in foreign

banks outside the U.S. or in foreign branches of

U.S. banks

• World Stock Markets

THE FOREIGN EXCHANGE MARKET

• The

foreign

exchange

price

of

one

currency

another currency

rate

is

the

in

terms

of

• The foreign exchange market is where funds are

converted from one currency into another and

the foreign exchange rate is determined.

BANKING AND FINANCIAL

INSTITUTIONS

• Financial

Intermediaries—institutions

that

borrow funds from people who have saved

and make loans to other people

• Banks—institutions that accept deposits and

make loans

• Other

Financial

Institutions—insurance

companies, finance companies, pension

funds, mutual funds and investment banks

• Financial Innovation—in particular, the advent

of the information age and e-finance

FUNCTION OF FINANCIAL

INTERMEDIARIES: INDIRECT FINANCE

• Lower transaction costs

– Economies of scale

– Liquidity services

• Reduce Risk

– Risk Sharing (Asset Transformation)

– Diversification

• Asymmetric Information

– Adverse Selection (before the transaction)—more likely to select

risky borrower

– Moral Hazard (after the transaction)—less likely borrower will

repay loan

WELL KNOWN (!) “CORE PRINCIPLES”

FROM MICROECONOMICS

1.

2.

3.

4.

Time has value

Risk requires compensation

Information is the basis for decisions

Markets determine prices and allocation

of resources

5. Stability improves welfare

TIME HAS VALUE

– Time affects the value of financial instruments

– Interest payments exist because of time

properties of financial instruments

RISK REQUIRES COMPENSATION

– In a world of uncertainty, individuals will

accept risk only if they are compensated in

some form.

INFORMATION IS THE BASIS FOR

DECISIONS

– The collection and processing of information

is the basis of foundation of the financial

system.

– Information Theory and Economics:

John Maynard Keynes/Frank Knight

KennethJ. Arrow

Joseph E. Stiglitz/Michael Spence/Geoge Akerlof

Claude Elwood Shannon/Christopeher Sims

MARKETS DETERMINE PRICES AND

ALLOCATE RESOURCES

Markets are “places” where buyers & sellers

“meet”.

In a market based system prices (as well as

quantities) are determined by markets.

Therefore markets allocate resources.

STABILITY IMPROVES WELFARE

A stable economy is believed to reduce risk.

Lowering risk may lead to an improvement in

everyone's welfare.

Is the competitive market mechanism stable?

Kenneth J. Arrow, Leonid Hurwicz, Frank Hahn

et. al.’s contributions: What they really show?

Stability of the competitive equilibrium or its

general instability?)

MONEY

MONEY AND THE PAYMENTS SYSTEM

1. What is money?

2. How do we use money?

3. How do we measure money?

DEFINITION OF MONEY

Money is an asset that is generally accepted as

payment for goods and services or repayment of

debt.

MONEY: CHARACTERISTICS

1. Means of payment: Used in exchange for

goods & services

2. Unit of account: Used to quote prices

3. Store of value: Used to move purchasing

power into the future

HOW WE PAY FOR THINGS-1

• Commodity Money: Objects with intrinsic value

• Fiat Money: Value comes from government

decree (or fiat)

• Checks: Instructions to the bank to shifts funds

from your account to that of the person or firm

whose name is written in the “Pay to the Order

of” line.

HOW WE PAY FOR THINGS-1

•

•

•

•

•

Credit Cards

Debit Cards

Electronic Funds transfers:

Stored Value Cards

E-Money

CREDIT AND DEBIT CARDS

• Credit cards:

– Deferred payment

– Issuer makes payment for you

– You have to pay it back

• Debit cards:

– Like a check

– Electronic message to your bank to transfer

funds immediately

THE FUTURE OF MONEY

Question: Which function of money will be with

us for a long time?

Answer:

– Means of payment: disappearing

– Unit of account: likely to remain

– Store of value: disappearing

TECHNOLOGICAL ADVANCES AND

PAYMENT METHODS

• Technological advances create new methods of

payment.

• Cell phones and other types of hand-held mobile

devices are providing access to the payments

system.

• What will be next?

MEASURING MONEY

• Changes in the quantity of money are

related to

– Interest Rates

– Economic Growth

– Inflation

• How do we measure money?

DEFINITION OF LIQUIDITY

Liquidity a measure of the ease an asset

can be turned into a means of payment

(Money).

THE LIQUIDITY SPECTRUM

MEASURING MONEY

Different Definitions of money are based upon

degree of liquidity.

M1: Narrowest definition, only most liquid assets

M1 (TURKEY)= Currency in Circulation

+ Sight Deposits

M2: Broader definition ,includes assets, in

general, not used as means of payment.

M2 (TURKEY)= M1+ Time Deposits

MONEY AND BUSINESS CYCLES

• Evidence suggests

important

role

business cycles

that

money plays an

in

generating

• Recessions

(unemployment)

(inflation) affect all of us

and

booms

• Monetary theory ties changes in the money

supply to changes in aggregate economic

activity and the price level

INFLATION

• Inflation: The rate at which the general price

level is increasing over time

• Inflation rate: The measure of the inflation

process

MONEY AND INFLATION

• The general (aggregate) price level is the

average price of goods and services in an

economy

• Question: Asset prices?

• A continual rise in the price level (inflation)

affects all economic players

• Data shows a connection between the money

supply and the price level

CONSUMER PRICE INDEX (CPI)

• The CPI answers the question:

"How much more would it cost for people to

purchase today the same basket of goods and

services that they actually bought at some fixed

time in the past?“

MONEY AND INTEREST RATES

• Interest rate is the price of money

• In the USA prior to 1980, the rate of money

growth and the interest rate on long-term

Treasury bonds were closely tied

• Since then, the relationship is less clear but still

an important determinant of interest rates

MONETARY AND FISCAL POLICY

• Monetary policy is the management of the

money supply and interest rates

– Conducted by the TCMB in Turkey [by the Federal

Reserve Bank (Fed) in the USA]

• Fiscal policy is government spending

and taxation

– Budget deficit is the excess of expenditures over

revenues for a particular year

– Budget surplus is the excess of revenues over

expenditures for a particular year

– Any deficit must be financed by borrowing

III. WHAT IS A BANK? A CLOSER

LOOK

What is robbing a bank compared

to founding one....

Bertold Brecht (1898-1956)

BANK CONCEPT IN A NUTSHELL

A Bank is an institution whose current

operations consist in granting loans and

receiving deposits from the public.

ANALYSIS OF THE DEFINITION

i) “Current”: “Temporary Landing is not counted”

ii) “and”: Mutual Funds only collect “deposits”, they

do not extend loans, instead they hold portfolios,

“finance companies” only lend by issuing equity or

debt instruments.

iii) “public”: Service is given to “general public” and

not to specialists.

BANKING FUNCTIONS

I. Liquidty and Payment Services

i) Money Changing

ii) Payment Services

II. Asset Transformation

i) Convenience of Denomination (unit size)

ii) Quality Transformation (better risk return characteristic)

iii) Maturity Transformation

III. Managing Risk

i) Estimating Risk on Bank Loans

ii) Managing Interest Rate and Liquidity Risk

iii) Off-Balance Sheet Operations

IV. Monitoring and Information Processing

BANKS AND THE REAL ECONOMY

• Do banks really play an important role in an

economy? Are banking services indispensable?

• In order to answer this question one needs to

formulate the working mechanism for an

economy and examine the role of banks in it.

• The general equilibrium approach to the market

economy may serve the purpose.

• This approach was initiated by Leon Walras

(1834-1910) and became a major tool of

economists after the contributions made,

notably,

by Kenneth J. Arrow & Gerard

Debreu in early 1950s.

Leon WALRAS (1834-1910)

Kenneth ARROW (1921)

Gerard DEBREU (1921-2004)

ARROW-DEBREU ECONOMY

1) Consider a two period, competitive economy with three

type of agents: i) consumers, ii) firms and iii) banks.

2) Suppose that there is one physical good which is initially

owned by households. Households can consume

part (or all) of it in the first period or it can be invested

by firms to produce consumption in the second

period.

3) Firms finance their investments either by issuing bonds

(Bf) or through loans (credits) from banks (L-) (Loan

Demand) .

4) Banks finance their loans (L+) (Loan Supply) by

collecting deposits (D-), or issuing bank bonds, (Bb).

5) Households hold their savings (S) either in the form of

bonds (Bh) or deposits (D+) (Deposit Supply).

MARKETS IN AN ARROW-DEBREU

ECONOMY

In this economy there are four markets:

1) Goods Market (Equilibrium Condition: I=S)

2) Deposit Market (Equilibrium Condition: D+= D-)

3) Loan (Credit) Market (Equilibrium Condition L+= L-)

4) Financial Market (Equilibrium Condition Bh= Bf+Bb)

In the (Walras-) Arrow-Debreu framework the general

equilibrium of an economy is achieved when all four

markets are in equilibrium.

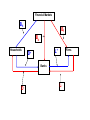

Financial Markets

Bh

Bf

Bb

Households

Firms

L+

D+

Banks

D-

L-

CONSUMER-1

Consumer maximizes her utility by allocating her savings

(S) between securities (Bh) and bank deposits (D+).

max u(C1,C2 )

(1)

subject to

C1 Bh D 1

(2)

C2 f b (1 r )Bh (1 rD )D

(3)

CONSUMER-2

• Consumer’s instruments are bonds and deposits.

• Her problem is to maximize her utility.

• She will determine optimum levels of bonds and

deposits, given her initial wealth, interest rates and

profits she expects to get at time 2.

CONSUMER-3

U

U

U

( 1)

(1 r ) 0

Bh C1

C2

U

U

U

(

1)

(1 rD ) 0

D

C1

C2

from these

U C1

(1 r )

U C2

U C1

(1 rD )

U C2

and therefore

r=rD

(4)

FIRM-1

The firm chooses its investment level (I) and its mode of

financing; i.e. by bank credit (L) or through issuing

securities Bf. The firm’s problem is, then, can be

formulated as:

max f

(5)

f f (I ) (1 r )Bf (1 rL )L

(6)

I Bf L

(7)

FIRM-2

f f

(1) (1 r ) 0

Bf I

f f

(1) (1 rL ) 0

L I

from these two equations we obtain

f

(1 r ) (1 rL )

I

or

r rL

(8)

BANK-1

• Bank determines its credit volume (L+), and

finances it through collecting deposits (D-) or

issuing securities (Bb).

max b

(9)

b rLL rBb rD D

(10)

L Bb D

(11)

BANK-2

• Substituting (1) and (11) into (9) and taking derivatives

with respect to D- and Bb, the following two equations are

obtained:

b

rL rD 0

D

b

rL r 0

Bb

from these two equations we get

r rD

(4)

and

r rL

(8)

EQUILIBRIUM

•

•

•

•

•

•

By definition in equilibrium all markets clear, i.e.

I=S (Goods market)

D+=D- (Deposit market)

L+=L- (Credit market)

Bh= Bf +Bb (Financial market)

Consider the profit function of a bank in equilibrium.

Using (4) and (8) and equilibrium conditions one gets

ˆb r (Bb D ) rBb rD =0

that is in equilibrium, bank profit is zero!

(12)

BANKS IN AN ARROW-DEBREU

ECONOMY:CONCLUSION

•

Moreover, notice that bank decisions have no impact

on other agents, since:

1) Consumers are indifferent between making deposits

and holding securities;

2) Firms also do not make any distinction between

financing themselves by bank credit or through issuing

bonds.

•

Are banks useless?