Survey

* Your assessment is very important for improving the workof artificial intelligence, which forms the content of this project

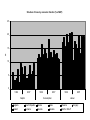

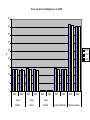

Tax competition and coordination within the EU – the case of the EU-10 Zoltán Pitti and Magdolna Sass (Corvinus University, Budapest and Institute of Economics of HAS, Budapest) Outline Selected problems addressed by the article • Characteristics of the tax systems of EU10 • Roots of tax system differences in EU-10 • Raising efficiency of tax collection – one way of mitigating the EU’s tax problems Characteristics of the EU-10 tax system • EU-10 tax capital at a lower rate than the EU average • this is compensated for by either a higher labour tax (Czech Republic and Hungary) • and/or by a higher consumption tax (Hungary, Estonia and Slovenia) • or by the overall lower taxation of economic activities and consumption, entailing smaller state involvement (Latvia, Lithuania and Slovakia) • Only gradual changes, the only country which turned its tax structure ‘upside down’ was Slovakia, which reduced all taxes significantly Implicit tax rates by economic function (%) 50 45 40 35 % 30 25 20 15 10 5 0 1996 2007 Implicit tax rate on capital 1996 2007 Implicit tax rate on consumption 1996 2007 Implicit tax rate on labour Bulgaria Czech Republic Estonia Latvia Lithuania Poland Romania Slovenia Slovakia EU-25 or EU-27 Hungary Structure of taxes by economic function (% of GDP) 25 20 % 15 10 5 0 1996 2007 1996 Capital 2007 1996 Consumption 2007 Labour Bulgaria Czech Republic Estonia Latvia Lithuania Poland Romania Slovenia Slovakia EU-25 or EU-27 Hungary Taxes and social contribution as a % of GDP 45 40 35 30 EU-15 % 25 EU-12 20 EU-27 15 10 5 0 2000 2008 2000 2008 2000 2008 taxes taxes taxes Indirect Direct Capital 2000 2008 Social contributions 2000 2008 Total tax revenue Roots/factors 1. the heritage of the Socialist period 2. half of EU-10: new states 3. transition-related issues, esp. being in a catch-up phase 4. certain conditions of EU accession 5. global developments U-27: fiscal problems becoming ever severe • We acknowledge the need for further tax harmonisation, but realistically list the factors against it • Conflicting demand towards fiscal policy: more welfare state – meaning higher taxes, but it should not harm competitiveness • The way out? • Not a solution but mitigating the problem Tax competition and tax coordination: raising a related question of efficiency • VAT comprises on average around 1/3 of total tax revenues and amount on average to 7-8 % of GDP, ranging from below 6 % (LU, ES) to above 10 % (BG, CY, DK) • Our very rough estimation reveals significant gaps between collected and ‘potential’ value added taxes (presumably not all related to the black/grey economy) • High ‘reserves’ for increasing collected taxes • we expect there may be similarly high ‘reserves’ (uncollected taxes) for other taxes as well • Improving the efficiency of tax collection could improve quite significantly fiscal positions of governments 38,6 40,0 LV EL RO 49,9 45,1 45,6 44,3 52,5 53,5 54,5 54,7 75,4 90,0 LT 57,7 56,1 52,1 47,3 50,0 IT ES PL FR PT UK SK MT BE 67,1 62,4 61,1 68,8 67,8 63,7 59,0 60,0 BG CZ HU EE SI FI SE 69,7 70,0 69,0 70,0 NL DE DK IE 76,4 80,0 AT CY 89,9 compliteness index (%) Calculated VAT effectiveness index in the EU-27, 2000 and 2007 100,0 2000 2007 30,0 20,0 10,0 - Thank you for your attention!