Survey

* Your assessment is very important for improving the workof artificial intelligence, which forms the content of this project

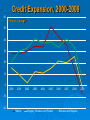

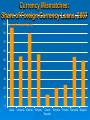

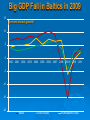

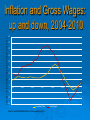

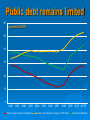

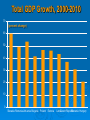

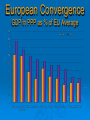

The Last Shall Be the First: The East European Financial Crisis, 2008-10 Anders Åslund Senior Fellow Peterson Institute for International Economics, Washington, DC Queries Causes of crisis? To devalue or not? Outcome? Political economy? Outlook? Causes of the Crisis Loose Monetary policy of the US Fed and ECB Excessive capital inflows (carry trade) Excessive credit expansion Real estate bubble Rising inflation Current account deficit Currency mismatches But decent public finances and little leverage Credit Expansion, 2000-2009 60 Percent Change 50 40 30 20 10 0 2000 2001 2002 2003 2004 2005 2006 2007 2008 -10 -20 Baltics Hungary, Slovakia, and Poland Romania and Bulgaria 2009 Inflation in 2008 18 (average consumer prices, percent change) 16 14 12 10 8 6 4 2 0 Latvia Lithuania Estonia Slovenia Hungary Slovakia Czech Poland Romania Bulgaria Republic Current Account Deficit, 2007, 2009, (Percent of GDP) *2010 figures based on IMF estimates Source: World Economic Outlook , IMF, (accessed on March 24, 2011) Foreign Debt, end 2009 180 (percent of GDP) 160 140 120 100 80 60 40 20 0 Latvia Lithuania Estonia Slovenia Hungary Slovakia Czech Republic Poland Romania Bulgaria Currency Mismatches: 100 Share of Foreign Currency Loans, 2007 90 (percent of total loans) 80 70 60 50 40 30 20 10 0 Latvia Lithuania Estonia Hungary Czech Slovakia Republic Poland Romania Bulgaria Big GDP Fall in Baltics in 2009 15 (percent annual growth) 10 5 0 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 -5 -10 -15 -20 Baltics Central Europe Southeastern Europe Issues Overheating followed by “sudden stop” Large falls in GDP: Latvia 25% Caused big budget deficits Large current account deficits Needed: Liquidity, budget cuts & competitiveness To Devalue or Not? No! No country changed exchange rate policy: Slovenia & Slovakia: euro Poland, Czech, Hungary & Romania – floating Baltics & Bulgaria - fixed Holding the Peg Bank system survived & govt did not have to recapitalize it Bankruptcies avoided Great integration renders devaluation ineffective Internal Devaluation: A crisis is a terrible thing to waste Major fiscal adjustment 10% in 2009 in Baltic countries Reduced public salaries & staff Closed state agencies Closed schools & hospitals Lean & efficient public sector Alternative: Devaluation Advantage: Earlier recovery through exports Disadvantages: Bank system collapse Oligarchs/big exporters would have gained wealth and power Less reforms Conclusion Ultimate problem: Loose monetary policy of US Fed and ECB No exchange rate regime could salvage these open and attractive economies No country changed exchange rate regime as no evident advantage Poor Macroeconomics Paul Krugman: “Latvia is the new Argentina.” ! Devaluation was neither necessary nor inevitable in the Baltics... Outcome (1) Unit labor costs fell sharply Flat income tax and low corporate taxes survived Current account turned around to big surplus in 2009 No deflationary cycle Return to growth sooner than expected Outcome (2) Minimal bank collapses All foreign-owned banks survived changes over the corresponding period of the previous year, % Inflation and Gross Wages: up and down, 2004-2010 40 35 30 25 20 15 10 5 0 2004 2005 2006 2007 2008 -5 -10 -15 Consumer Prices Source: Central Statistical Bureau of Latvia, www.csb.gov.lv. Gross Wages 2009 2010 Crisis bred budget deficits 2009-11 2 (percent of GDP) 0 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011E -2 -4 -6 -8 -10 Estonia, Latvia, Lithuania, and Bulgaria Poland, Czech Republic, Hungary, and Romania Slovenia and Slovakia Public debt remains limited 60 (percent of GDP) 50 40 30 20 10 0 2000 2001 2002 2003 Estonia, Latvia, Lithuania, and Bulgaria 2004 2005 2006 2007 2008 2009 Poland, Czech Republic, Hungary, and Romania 2010 2011E Slovenia and Slovakia Apart from in Hungary & Poland, end 2010 90 80 (percent of GDP) 70 60 50 40 30 20 10 0 Latvia Lithuania Estonia Slovenia Hungary Slovakia Czech Poland Romania Bulgaria Republic Political Economy People have demanded realistic, radical crisis resolution Minimal social unrest Cuts of 10% of GDP (Baltics) politically easier than 2% of GDP Strange myth that democracies cannot cut public expenditures: Political Economy 2 Radical, early adjustment preferable Better to cut expenditures than raise taxes Equity is important Political Economy 3 8 of 10 countries have changed government during the crisis 9 of 10 countries have centerright governments – center right stronger than ever Multi-party coalitions most effective in crisis International Assistance 1. International liquidity crucial: missing first because ECB was passive 2. Large early international assistance vital 3. New cooperation IMF-EU worked well 4. EU grants important: 4-7% of GDP Outlook Main concerns: reversed pension reforms and rising inflation Trimmed public sectors: Expenditure cuts rather than higher taxes Eastern Europe has gained efficiency and self-confidence: European convergence continues The Last Shall Be the First 20 Inflation: Threat again (percent change) 18 16 14 12 10 8 6 4 2 0 2000 2001 2002 2003 Estonia, Latvia, Lithuania, and Bulgaria 2004 2005 2006 2007 2008 Poland, Czech Republic, Hungary, and Romania 2009 2010 2011E Slovenia and Slovakia Total GDP Growth, 2000-2010 70 (percent change) 60 50 40 30 20 10 0 Slovakia Romania Lithuania Bulgaria Poland Estonia Latvia Czech Republic Slovenia Hungary European Convergence GDP in PPP as % of EU Average