Survey

* Your assessment is very important for improving the work of artificial intelligence, which forms the content of this project

* Your assessment is very important for improving the work of artificial intelligence, which forms the content of this project

Fei–Ranis model of economic growth wikipedia , lookup

Ragnar Nurkse's balanced growth theory wikipedia , lookup

Economic democracy wikipedia , lookup

Chinese economic reform wikipedia , lookup

Economic calculation problem wikipedia , lookup

Productivity wikipedia , lookup

Uneven and combined development wikipedia , lookup

Production for use wikipedia , lookup

Rostow's stages of growth wikipedia , lookup

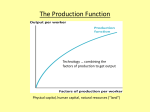

3.1 Introduction • In this chapter, we learn: – Some facts related to economic growth that later chapters will seek to explain. – How economic growth has dramatically improved welfare around the world. • this growth is actually a relatively recent phenomenon 3.1 Introduction • In this chapter, we learn: – Some tools used to study economic growth, including how to calculate growth rates. – Why a “ratio scale” makes plots of per capita GDP easier to understand. • The United States of a century ago could be mistaken for Kenya or Bangladesh today. • Some countries have seen rapid economic growth and improvements to health quality, but many others have not. 3.2 Growth over the Very Long Run • Sustained increases in standards of living are a recent phenomenon. • Sustained economic growth emerges in different places at different times. – Thus, per capita GDP differs remarkably around the world. • The Great Divergence – The recent era of increased difference in standards of living across countries. • Before 1700 – Per capita GPD in nations differed only by a factor of two or three. • Today – Per capita GPD differs by a factor of 50 for several countries. 3.3 Modern Economic Growth • Timeline: from 1870 to 2000, United States per capita GDP . . . – . . . rose by nearly 15-fold. • Implications for you? – A typical college student today will earn a lifetime income about twice his or her parents. 3.4 Modern Growth around the World • After World War II, growth in Germany and Japan accelerated. • Convergence – Poorer countries will grow faster to “catch up” to the level of income in richer countries. • Brazil had accelerated growth until 1980 and then stagnated. – China and India have had the reverse pattern. A Broad Sample of Countries • Over the period 1960–2007 – Some countries have exhibited a negative growth rate. – Other countries have sustained nearly 6 percent growth. – Most countries have sustained about 2 percent growth. • Small differences in growth rates result in large differences in standards of living. Case Study: People versus Countries • Since 1960: – The bulk of the world’s population is substantially richer. – The fraction of people living in poverty has fallen. • A major reason for changes – Economic growth in China and India – These are 40 percent of the world population! Case Study: Growth Rules in a Famous Example, Yt = AtKt1/3Lt2/3 • Applying rules of growth rates • Original output equation: • Use multiplication rule to get • Use exponent rule to get 3.6 The Costs of Economic Growth • The benefits of economic growth – Improvements in health – Higher incomes – Increase in the variety of goods and services • Costs of economic growth include: – Environmental problems – Income inequality across and within countries – Loss of certain types of jobs • Economists generally have a consensus that the benefits of economic growth outweigh the costs. 3.7 A Long-Run Roadmap • Are there certain policies that will allow a country to grow faster? • If not, what about a country’s “nature” makes it grow at a slower rate? Summary • Sustained growth in standards of living is a very recent phenomenon. • If the 130,000 years of human history were warped and collapsed into a single year, modern economic growth would have begun only at sunrise on the last day of the year. Summary • Modern economic growth has taken hold in different places at different times. • Since several hundred years ago, when standards of living across countries varied by no more than a factor of 2 or 3, there has been a “Great Divergence.” • Standards of living across countries today vary by more than a factor of 60. • Since 1870 – Growth in per capita GDP has averaged about 2 percent per year in the United States. – Per capita GDP has risen from about $2,500 to more than $37,000. • Growth rates throughout the world since 1960 show substantial variation – Negative growth in many poor countries – Rates as high as 6 percent per year in several newly industrializing countries, most of which are in Asia • Growth rates typically change over time • In Germany and Japan – Growth picked up considerably after World War II. – Incomes converged to levels in the United Kingdom. – Growth rates have slowed down as this convergence occurred. • Brazil exhibited rapid growth in the 1950s and 1960s and slow growth in the 1980s and 1990s. • China showed the opposite pattern. • Economic growth, especially in India and China, has dramatically reduced poverty in the world. • In 1960 – Two out of three people in the world lived on less than $5 per day (in today’s prices). • By 2000 – This number had fallen to only 1 in 10. 4.1 Introduction • In this chapter, we learn: – How to set up and solve a macroeconomic model. – How a production function can help us understand differences in per capita GDP across countries. – The relative importance of capital per person versus total factor productivity in accounting for these differences. – The relevance of “returns to scale” and “diminishing marginal products.” – How to look at economic data through the lens of a macroeconomic model. • A model: – Is a mathematical representation of a hypothetical world that we use to study economic phenomena. – Consists of equations and unknowns with real world interpretations. • Macroeconomists: – Document facts. – Build a model to understand the facts. – Examine the model to see how effective it is. 4.2 A Model of Production • Vast oversimplifications of the real world in a model can still allow it to provide important insights. • Consider the following model – Single, closed economy – One consumption good Setting Up the Model • A certain number of inputs are used in the production of the good • Inputs – Labor (L) – Capital (K) • Production function – Shows how much output (Y) can be produced given any number of inputs • Others variables with a bar are parameters. • Production function: Output Productivity parameter Inputs • The Cobb-Douglas production function is the particular production function that takes the form of Assumed to be 1/3. Explained later. • A production function exhibits constant returns to scale if doubling each input exactly doubles output. Returns to Scale Comparison Find the sum of exponents on the inputs Result • sum to 1 • the function has constant returns to scale • sum to more than 1 • the function has increasing returns to scale • sum to less than 1 • the function has decreasing returns to scale • Standard replication argument – A firm can build an identical factory, hire identical workers, double production stocks, and can exactly double production. – Implies constant returns to scale. Allocating Resources Firm chooses inputs to maximize profit Rental rate of capital Wage rate • The rental rate and wage rate are taken as given under perfect competition. • For simplicity, the price of the output is normalized to one. • The marginal product of labor (MPL) – The additional output that is produced when one unit of labor is added, holding all other inputs constant. • The marginal product of capital (MPK) – The additional output that is produced when one unit of capital is added, holding all other inputs constant. • The solution is to use the following hiring rules: – Hire capital until the MPK = r – Hire labor until MPL = w • If the production function has constant returns to scale in capital and labor, it will exhibit decreasing returns to scale in capital alone. Solving the Model: General Equilibrium • The model has five endogenous variables: – Output (Y) – the amount of capital (K) – the amount of labor (L) – the wage (w) – the rental price of capital (r) • The model has five equations: – The production function – The rule for hiring capital – The rule for hiring labor – Supply equals the demand for capital – Supply equals the demand for labor • The parameters in the model: – The productivity parameter – The exogenous supplies of capital and labor • A solution to the model – A new set of equations that express the five unknowns in terms of the parameters and exogenous variables – Called an equilibrium • General equilibrium – Solution to the model when more than a single market clears • In this model – The solution implies firms employ all the supplied capital and labor in the economy. – The production function is evaluated with the given supply of inputs. – The wage rate is the MPL evaluated at the equilibrium values of Y, K, and L. – The rental rate is the MPK evaluated at the equilibrium values of Y, K, and L. Interpreting the Solution • If an economy is endowed with more machines or people, it will produce more. • The equilibrium wage is proportional to output per worker. • Output per worker = (Y/L) • The equilibrium rental rate is proportional to output per capital. • Output per capital = (Y/K) • In the United States, empirical evidence shows: – Two-thirds of production is paid to labor. – One-third of production is paid to capital. – The factor shares of the payments are equal to the exponents on the inputs in the CobbDouglas function. • All income is paid to capital or labor. – Results in zero profit in the economy – This verifies the assumption of perfect competition. – Also verifies that production equals spending equals income. Case Study: What Is the Stock Market? • Economic profit – Total payments from total revenues • Accounting profit – Total revenues minus payments to all inputs other than capital. • The stock market value of a firm – Total value of its future and current accounting profits – The stock market as a whole is the value of the economy’s capital stock. 4.3 Analyzing the Production Model • Per capita = per person • Per worker = per member of the labor force. – In this model, the two are equal. • We can perform a change of variables to define output per capita (y) and capital per person (k). • Output per person equals the productivity parameter times capital per person raised to the one-third power. Output per person Productivity parameter Capital per person • What makes a country rich or poor? • Output per person is higher if the productivity parameter is higher or if the amount of capital per person is higher. – What can you infer about the value of the productivity parameter or the amount of capital in poor countries? Comparing Models with Data • The model is a simplification of reality, so we must verify whether it models the data correctly. • The best models: – Are insightful about how the world works – Predict accurately The Empirical Fit of the Production Model • Development accounting: – The use of a model to explain differences in incomes across countries. Set productivity parameter = 1 • Diminishing returns to capital implies that: – Countries with low K will have a high MPK – Countries with a lot of K will have a low MPK, and cannot raise GDP per capita by much through more capital accumulation • If the productivity parameter is 1, the model overpredicts GDP per capita. Case Study: Why Doesn’t Capital Flow from Rich to Poor Countries? • If MPK is higher in poor countries with low K, why doesn’t capital flow to those countries? – Short Answer: Simple production model with no difference in productivity across countries is misguided. – We must also consider the productivity parameter. Productivity Differences: Improving the Fit of the Model • The productivity parameter measures how efficiently countries are using their factor inputs. • Often called total factor productivity (TFP) • If TFP is no longer equal to 1, we can obtain a better fit of the model. • However, data on TFP is not collected. – It can be calculated because we have data on output and capital per person. – TFP is referred to as the “residual.” • A lower level of TFP – Implies that workers produce less output for any given level of capital per person 4.4 Understanding TFP Differences • Why are some countries more efficient at using capital and labor? Human Capital • Human capital – Stock of skills that individuals accumulate to make them more productive – Education, training, etc. • Returns to education – Value of the increase in wages from additional schooling • Accounting for human capital reduces the residual from a factor of 11 to a factor of 6. Technology • Richer countries may use more modern and efficient technologies than poor countries. – Increases productivity parameter Institutions • Even if human capital and technologies are better in rich countries, why do they have these advantages? • Institutions are in place to foster human capital and technological growth. – Property rights – The rule of law – Government systems – Contract enforcement Misallocation • Misallocation – Resources not being put to their best use • Examples – Inefficiency of state-run resources – Political interference Case Study: A “Big Bang” or Gradualism? Economic Reforms in Russia and China • When transitioning from a planned to a market economy, the change can be sudden or gradual. – A “big bang” approach is one where all old institutions are replaced quickly by democracy and markets. – A “gradual” approach is one where the transition to a market economy occurs slowly over time. • Russia followed a “big bang” approach, yet GDP per capita has declined since the transition. • China has seen accelerated economic growth using the “gradual” approach. 4.5 Evaluating the Production Model • Per capita GDP is higher if capital per person is higher and if factors are used more efficiently. • Constant returns to scale imply that output per person can be written as a function of capital per person. • Capital per person is subject to strong diminishing returns because the exponent is much less than one. • Weaknesses of the model: – In the absence of TFP, the production model incorrectly predicts differences in income. – The model does not provide an answer as to why countries have different TFP levels. Summary • Per capita GDP varies by a factor of 50 between the richest and poorest countries of the world. • The key equation in our production model is the Cobb-Douglas production function: Output Productivity parameter Inputs • The exponents in this production function: – One-third of GDP is paid out to capital. – Two-thirds is paid to labor. – Exponents sum to 1, implying constant returns to scale in capital and labor. • The complete production model consists of five equations and five unknowns: - Output Y Capital K Labor L Wage rate w Rental rate r • The solution to this model is called an equilibrium. • The prices w and r are determined by the clearing of labor and capital markets. • The quantities of K and L are determined by the exogenous factor supplies. • Y is determined by the production function. • The production model implies that output per person in equilibrium is the product of two key forces: – Total factor productivity (TFP) – Capital per person • Assuming the TFP is the same across countries, the model predicts that income differences should be substantially smaller than we observe. • Capital per person actually varies enormously across countries, but the sharp diminishing returns to capital per person in the production model overwhelm these differences. • Making the production model fit the data requires large differences in TFP across countries. • Economists also refer to TFP as the residual, or a measure of our ignorance. • Understanding why TFP differs so much across countries is an important question at the frontier of current economic research. • Differences in human capital (such as education) are one reason, as are differences in technologies. • These differences in turn can be partly explained by a lack of institutions and property rights in poorer countries. This concludes the Lecture Slide Set for Chapter 4 Macroeconomics Second Edition by Charles I. Jones W. W. Norton & Company Independent Publishers Since 1923