Survey

* Your assessment is very important for improving the workof artificial intelligence, which forms the content of this project

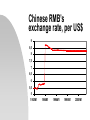

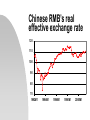

China’s Exchange Rate System after WTO Accession: Some Considerations Jian-Guang Shen, Bank of Finland Institute for Economies in Transition Chinese RMB’s exchange rate, per US$ 9 8,5 8 7,5 7 6,5 6 5,5 5 1992M1 1994M1 1996M1 1998M1 2000M1 Chinese RMB’s real effective exchange rate 120 110 100 90 80 70 1992M1 1994M1 1996M1 1998M1 2000M1 China’s exchange rate system Dual exchange rate regime prior to 1994 Single exchange rate since 1994 Nominally a system of managed floating exchange rate Practically a peg to the US dollar supported by comprehensive, direct capital account controls. China’s exchange rate market The nation-wide inter-bank foreign exchange market, the China Foreign Exchange Trading Centre (CFETC) All foreign exchange trading has been conducted in this market. The CFETC also provides settlement services Over 300 foreign exchange banks and non-banking financial institutions Problems with China’s exchange rate market Only financial institution headquarters hold CFETC memberships Dominated by the PBOC and BOC Capital control regulations suppress supply and demand Centralised trading system has high costs and restrictions Only three foreign currencies (USD, HKD, JPY), no futures and options China’s capital control measures I Capital brought in from abroad must be deposited in special accounts in designated banks. Any repayments and remittances from these accounts are also subject to SAFE approval. Foreign investment in the Chinese stock market is limited to B shares. Inbound foreign capital must get SAFE approval to convert to RMB. China’s capital control measures II All long-term foreign borrowing (over one year) must be mentioned in the state commercial loan plan. Commercial loans of longer than three months but less than or equal to one year have to be registered with SAFE, and the conditions for repayment of principal and interest rates must be approved by SAFE. China’s capital control measures III Only PBOC-approved state organisations can issue bonds abroad. Leasing and trust loans from abroad are subject to state plans for foreign capital utilisation. All foreign loan guarantees require SAFE approval. Outbound foreign investments must receive SAFE approval. Results of China’s capital control measures China’s foreign debt structure is dominated by medium- and longterm foreign debt Short-term foreign capital inflows usually are part of commercial deals State sovereignty debts are significant Four alternatives: benefits and disadvantages Fixed exchange rate regime Crawling peg Float within bands (target zone) Managed float with no preannounced exchange rate path Long term goal A flexible exchange rate mechanism with free crossborder capital mobility The role of RMB in the international financial market Manage the transition The exit strategy: No depreciation pressure join a net capital flow situation China satisfies both, but worries about: Appreciation pressure the pace of liberalization in accordance with other financial market development The fixed exchange rate system Benefits Stable currency As nominal anchor for monetary policy Prevent currency risks Disadvantages Inflexible in the face of shocks No monetary autonomy under capital liberalisation prone to currency crisis Floating regime Benefits Flexible in the face of shocks Monetary autonomy under capital liberalisation Not prone to currency crises Disadvantages Strong fundamentals needed Excessive currency risks Interest rates still fixed by PBOC More developed financial markets needed Floating within bands Benefits Some flexibility in the face of shocks Less strong fundamentals needed Avoid excessive currency risks Disadvantages Vulnerable to speculative currency attacks Difficult to decide the band Now RMB has revaluation pressure Crawling Peg Benefits Relatively stable currency Some flexibility in the face of shocks Disadvantages Vulnerable to speculative attacks Crawling rule difficult to design Low monetary autonomy and credibility Capital account liberalisation in China The effect of WTO accession Liberalisation of financial markets Money market Capital market Foreign exchange market Operational difficulties Commercial banks Domestic enterprises The central bank Capital account control still useful The second-best argument: compensation for imperfect markets in China Increased risks in the financial system: the lesson of the Latin American and Asian Crises Assistance for monetary and fiscal policies Conclusions WTO membership needs more flexible exchange rate system China as a large continental-type economy Capital account liberalisation inevitable More shocks require it