Survey

* Your assessment is very important for improving the workof artificial intelligence, which forms the content of this project

History of the Federal Reserve System wikipedia , lookup

Financial economics wikipedia , lookup

Credit rationing wikipedia , lookup

Interbank lending market wikipedia , lookup

Quantitative easing wikipedia , lookup

Financialization wikipedia , lookup

United States housing bubble wikipedia , lookup

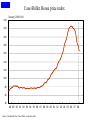

The crisis, global imbalances and the role of emerging markets Shanghai conference Gilles Saint-Paul A. The Context: Global Imbalances An unsustainable boom • Very large trade deficits of the US • These deficits were due to a very low savings rate (= high consumption) • They were financed by excess savings in China, Japan, and producers of primary materials • This was further fueled by – BofC exchange rate policy – Low FED interest rates What should the adjustment look like? • A large, permanent fall in US private consumption expenditure (by 5 % of US GDP) • A reallocation of economic activity to the export sector (by 5 % of US GDP) • A depreciation of the US real exchange rate (by 20 % to 40 %) A crisis difficult to avoid • US consumption has to fall by 2 % of World GDP • US export increase has to be sustained by a rise in demand outside the US, i.e. in China • But this conflicts with the Chinese mercantilist policies as well as their inadequate internal market • Furthermore, US fall in aggregate demand as well as depreciation will have massive effects on the Eurozone B. The Housing Bubble Fig. 2.2 Case-Shiller House price index January 2000=100 240 220 200 180 160 140 120 100 80 60 40 88 89 90 91 92 93 94 95 96 97 98 99 00 01 02 03 04 05 06 07 08 Source: Standard & Poor Case-Shiller, composite index. What is a bubble? • Loosely, « prices are too high » • However, too high prices can be rational • Price deviates from the fundamental because prices high in the future • Asset held even though bubble may rationally be expected to burst • In this case, it rises even more quickly Are bubbles sustainable in general equilibrium? • In the long-run, the bubble cannot grow faster than the economy • A bubble is more likely, – The higher the growth prospects – The lower the interest rate • These conditions were satisfied during the relevant period Fig. 1.1 9.0 Economic growth and Ifo economic climate for the world % 1995=100 Real GDP growth 8.0 7.0 140 (left-hand scale) 130 Ifo World Economic Climate a) 120 (right-hand scale) 110 6.0 100 5.0 90 4.0 80 3.0 2.0 3.4 3.3 2.9 1.0 1.5 2.0 2.0 4.9 4.7 3.7 4.0 3.6 3.5 2.5 4.5 2.2 70 5.1 5.2 2.8 60 3.4 2.3 1.4 0.0 50 40 90 91 92 93 94 95 96 97 98 99 00 01 02 03 04 05 06 07 08 09 10 a) Arithmetic mean of judgements of the present and expected economic situation. Sources: IMF, World Economic Outlook Database October 2008, Update January 2009 (GDP 2008, 2009 and 2010, EEAG forecast); Ifo World Economic Survey (WES) I/2009. Fig. 1.15 Central bank interest rates 7.0 % Federal funds rate (US) 6.0 5.0 Bank rate (UK) 4.0 3.0 2.0 % 2.0 Main refinancing bid rate (ECB) 1.0 1.5 % 0.25 % 0.1 % Average target rate (BoJ) 0.0 1999 2000 2001 2002 2003 2004 2005 2006 Sources: European Central Bank; Federal Reserve Bank of St. Louis; Bank of England; Bank of Japan. 2007 2008 2009 The consequences of bubbles • A wealth effect consumption goes up – Ex: consumption loan taken out of a loan against appreciation in the value of the house • Most houses owned by US residents US trade deficit goes up • Foreigners may want to join the bubble rise in demand for US assets US trade deficit goes up The consequences of bubbles (II) • Corporations and entrepreneurs make capital gains • They can use their assets as collateral • Borrowing easier • The cost of capital falls • Investment goes up • This is called the financial accelerator Fig. 1.12 Credit growtha) in the euro area % 16 14 Lending for house purchases 12 10 8 6 4 2 Corporate credit Consumer credit 0 2001 2002 2003 2004 2005 2006 2007 2008 a) Annual percentage chnage; corporate credit = credit to non-financial corporations; lending to house purchases = credit to private households and Non Profit Institutions Serving Households. Sources: European Central Bank; Ifo Institute calculations. Fig. 1.18 Spread between corporate and government bonds 6.0 % % 1.6 1.4 5.0 1.2 4.0 1.0 3.0 0.8 0.6 2.0 0.4 1.0 0.2 0.0 0.0 1986 1988 1990 1992 1994 1996 1998 USA Baa long term (left-hand scale) Bank bonds Germany 9-10 years (right-hand scale) Sources: Deutsche Bundesbank; EcoWin; Ifo Institute calculations. 2000 2002 2004 2006 2008 Euro area BBB 10 years (left-hand scale) Euro area AAA 10 years (right-hand scale) Fig. 2.5 1200 Commercial paper outstanding in the United States Billions of dollars 1100 1000 Asset-backed CP 900 800 Non-asset backed CP 700 600 2004 Source: Federal Reserve Bank. 2005 2006 2007 2008 The consequences of bubbles (III) • If asset is accumulable, greater incentives to produce it • Excess investment in the bubbble-ridden sector • Ex: construction boom in US, Spain C. The crisis A 3-dimensional crisis: • A solvency problem • A liquidity problem • A demand problem The solvency problem • Lenders assumed house prices would not fall – Bank made whole by seizing the house – Everybody can get a loan – Add deregulation and the loan can be 100% of the purchase price • But prices did fall – Giving back the house cheaper than reimbursing – This would have happened anyway as repossessions would have taken place and depressed the price The spreading of insolvency • Securitization diluted ownership of mortgages throughout the financial system • In principle, this is good, BUT – Systemic price risk ignored – Institutions highly leveraged all ended vulnerable – Moral hazard problem in monitoring the loans How to deal with insolvency? • • • • Insolvency is taken care of by bankruptcy What is bankruptcy? Shareholders lose their shares Creditors take over and the losses are allocated between them • The firm starts again Why not? • It is a lengthy process • Some assets may be inefficiently liquidated • But it could have been doable with coordination by the government • One simple way of doing it is – Computing the true value of the assets – Do a debt/equity swap A debt-equity swap: Assets Debt Equity Before the crisis 120 100 20 During the crisis 60 100 -40 Conversion 1 $ of Debt 0.45 $ of Debt + 0.15 $ of equity After the crisis 60 45 15 Why a bailout instead? • Policymakers feared a run on the financial system • Runs exist because assets are less liquid than liabilities • Example: – 100 $ of deposits == 100 $ of a house – If all withdraw their deposits, all houses have to be sold – But the equilibrium price will fall, not all can be paid – It is then rational for me to withdraw before the others Bank run is one equilibrium Two aspects of liquidity • A (real) asset is worth less if liquidated now than allowed to continue to run – Deposit insurance will eliminate the « run » equilibrium, since everybody will be served • A (financial) market may be too thin for absorbing a large supply shock – Government purchases may render the market liquid The transmission mechanism • The bursting bubble reduces aggregate demand through two mechanisms: – Wealth effect on consumers – Financial accelerator on firm • Furthermore, this is exacerbated by debtdeflation: – Which increases the default rate – And reduces the (net) collateral of borrowers The policy response • Replace the bubble by the same nominal amount of public debt (Bail out) • Replace private consumption by public consumption (Stimulus) • Print money D. The response to the crisis Bail out • Bailout prevents technical bankruptcy of bailed out institutions • Bail-out can be win-win if value of assets < true value because of liquidity (ex. Sweden) • Unlikely in the present situation: cost to tax payer is real • Furthermore: – Opacity on the withdrawal of toxic assets – Sets the stage for another round of excessive risktaking (Moral hazard) “The TARP was originally conceived to purchase troubled assets directly from banks. However, as quickly became apparent, properly valuing these assets was extremely difficult as a result of ongoing home mortgage foreclosures, defaults, and falling house prices. The financial turmoil intensified in the weeks following the bill’s passage, and to move quickly, the U.S. Treasury established the Capital Purchase Program (CPP), which became the centerpiece of TARP. The goal of the CPP was to recapitalize healthy banks by purchasing preferred shares of stock in banks instead of purchasing their troubled assets” Stimulus • Governments apply standard Keynesian analysis • But the required US fall in consumption is permanent, not temporary • Stimulus postpones the adjustment by preventing real exchange rate depreciation and price falls – G instead of X replaces C Perverse effects of stimulus • If future taxes highly distortionary, adverse response of consumption and stimulus contractionary (Cf japanese experience) • Furthermore, expectations of stimulus make recession worse in the short run by maintaining high prices • Finally, one may exit in a worse situation, with impoverished consumers and deteriorated public accounts Money • The liquidity injected replaces internal money with external one • This may prove highly inflationary when the internal money creation process resumes • Furthermore, a chunk of the money is backed by poor assets • Withdrawing the money when exiting the crisis may prove a delicate task Fig. 2.7 2400 Central bank balance sheets Billions of dollars Billions of euros 2400 2200 2200 2000 2000 1800 1800 a) ECB 1600 1600 1400 1400 1200 FED 1200 b) 1000 1000 800 800 600 600 J F M A M J J A S O N D J F M A M 2007 a) Total assets/liabilities. b) Total factors supplying reserve funds. Source: European Central Bank; Federal Reserve Bank. J J 2008 A S O N D J 2009 E. The near future and the role of China and emerging markets Implications for China: consumption • Consumption must rise in China – Because US aggregate demand cannot continue at that rate – Because Chinese growth rates are high and consumption should be smoothed – Because China has accumulated a large – stock of foreign assets Implications for China: real exchange rate • To sustain higher consumption, the Chinese real exchange rate must appreciate • Pegging the renmibi to the US dollar does not prevent it • It postpones it and makes it happen through inflation • Dangerous because of inflation inertia • Better to let the renmibi float, albeit in a managed way Where should the money go? • US assets have low return – Recession – Uncertainty about the dollar – Uncertainty about inflation – Potential high future taxes, including on capital • In similar circumstances, many countries have experienced massive depreciation and BoP crisis • This is not happening (yet). Why? The investors lack alternatives • Eurozone suffer from similar problems • Other zones suffer from insecure property rights and/or undeveloped markets • Consequently US assets remain paradoxically a good deal The Euro option: • Inherited stock of public debt typically higher than in the US • Monetary policy more conservative lower LT inflation risk • Euro may be over-valued • Some countries with fiscal/competitiveness problems may jeopardize the Euro The emerging market options • No country among B,R,I,C has an established reputation of securing property rights (I ?) • Return on investment also depends on development of internal markets: – Access to customers – Existence of a mass consumption sector – Financial development – Lack of financial repression Conclusion • It is illusory to stimulate by perpetuating the diseases of the boom, i.e. – Overconsumption – Overindebtedness and bad loans – Misallocation of activity • Aggregate demand must move where the money is (China, etc.) • The US Real exchange rate must depreciate (this process has started) • The US is lucky to have avoided sharp capital flight so far.