Survey

* Your assessment is very important for improving the work of artificial intelligence, which forms the content of this project

Securitization wikipedia , lookup

Troubled Asset Relief Program wikipedia , lookup

2010 Flash Crash wikipedia , lookup

Investment fund wikipedia , lookup

Market sentiment wikipedia , lookup

Currency intervention wikipedia , lookup

Efficient-market hypothesis wikipedia , lookup

Hedge (finance) wikipedia , lookup

Systemically important financial institution wikipedia , lookup

Financial crisis of 2007–2008 wikipedia , lookup

Systemic risk wikipedia , lookup

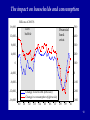

Understanding the Great Recession Economics 122: Fall 2010 1 Using macro to understand the current recession Let’s analyze the history of the recession to illustrate some of the major macro issues/tools Underlying forces: 1. Increasing leverage with lower perceived risks 2. The housing bubble 3. A “run on the banks” and the Lehman bankruptcy 4. The crash in asset prices 5. Decline in wealth leading to declining I and C. 6. International transmissions 7. IS-TR curve interpretation 8. Liquidity trap! 9. Governmental response in monetary and fiscal policies 10. The trough in late 2009 11. The long stagnation to reach full employment (?) 2 The bubble economy 3 Trends in volatility of US stock prices Historical lows Note: Implied volatility is a measure of the equity price variability implied by the market prices of call options on equity futures. Historical volatility is calculated as a rolling 100-day annualized standard deviation of equity price changes. Volatilities are expressed in percent rate of change. VIX is CBOE index. 4 Leveraging the US economy 5 Rising leverage of US economy 4 10 8 3 6 2 4 1 2 Total financial assets/K Total financial assets/GDP 0 1930 1940 1950 1960 1970 Source: Federal Reserve flow of funds data. 1980 1990 2000 0 2010 5 The result on housing prices Real housing prices [1987-1995 = 100] 200 1. Rising perceived wealth of households 19952006. 2. Then catastrophic loss of wealth 20062009 160 120 80 40 0 1985 1990 1995 2000 2005 2010 6 Then people wake up from the dream to the nightmare of falling wealth … 7 Mortgage delinquencies for subprime mortgages 8 Source: IMF, Global Financial Stability Report, Oct 2008 at imf.org The loss of paper wealth Household net worth/disposable income 6.5 Wealth loss of $12 trillion ($100,000 per household) 6.0 5.5 5.0 4.5 4.0 60 65 70 75 80 85 90 95 00 05 10 9 The impact on households and consumption Billions of 2005 $ 16,000 12,000 500 Financial bank crisis Tech bubble 400 8,000 300 4,000 200 0 100 -4,000 0 -8,000 -100 -12,000 -200 Change in net worth (left scale) Change in consumption (right scale) -16,000 00 01 02 03 04 05 06 07 -300 08 09 10 10 Predictions of consumption theory Consumption function: p Ct = β1 Y t + β2 Wt Savings rate: p s = 1 – β1 - β2 Wt /Y t .26 12 .24 10 .22 8 .20 6 .18 4 .16 2 Wealth-income ratio (inverted, left scale) Personal savings rate (right scale) .14 60 65 70 75 80 85 90 95 00 0 05 10 11 Bank runs Series of bank runs. Different from earlier (Depression era) because was the run by large depositors (run on the repo). Bear Stearns and Lehman were wiped out in a week. 12 Bank losses* * Note that US bank equity was around $1000 billion in 2010. 13 Chicken little 14 The Lehman Bankruptcy A central event in the crisis. Market fundamantalists worried that continued bailouts would lead to “moral hazard” and worse future problems. So on September 15, 2008, government decided to let Lehman go bankrupt. Catastrophic results: - markets froze up (people could not make transactions) - stock market went down 30 % in a month and US dollar ROSE almost 20 %. - market fundamentalism lasted just 36 hours (!) - then bailout of AIG, Citibank, BofA, TARP, GM, etc. - Fed opened up several new facilities to steady markets “An economy in free fall” in the fall of 2008. 15 Risk on Mature Govt Debt (US, etc.) CDS = risk that security will default. These are US and similar Treasury bonds! 16 A risk measure on commercial paper Source: Federal Reserve page on commercial paper. These are short-term promissory note or unsecured money market obligation, issued by prime rated commercial firms and financial companies. This shows medium-grade (A2/P2) minus top grade (AA). 17 Risk premiums on top-rated securities IMF 18 Impact of Credit Crunch on Investment .18 9.5 Credit crisis .17 9.0 .16 8.5 .15 8.0 .14 7.5 .13 7.0 .12 6.5 .11 6.0 .10 5.5 2005 2006 2007 2008 2009 2010 Investment/Potential GDP Baa bond rate 19 Macroeconomic impacts 20 Macroeconomic impacts Rewrite augmented IS and TR curves as follows: IS: Y = C(Y,W) +I(rr) + G + NX Y = C(Y,W) +I(i - π + δ) + G + (X – M) TR: i = f(Y, π) rr = risky real rate = i - π + δ, where δ is the risk premium Have adverse IS shifts to W, δ, and NX Fed lowers i in standard manner, but real interest rate for businesses goes up! TR = Taylor rule (or LM in old-fashioned theory) 21 Before crisis Taylor Rule (TR) iff IS(i ff - π + risk premium) i* 2006 Y After financial crisis TR iff IS(i ff - π + low risk premium) i* IS’(i ff - π + high risk premium) 2008 Y World output trends 24 Policy Responses (thanks to Keynes’s theories) Gwendolen Darwin Raverat 25 Financial Market Support Measures 2007-2010 26 Unconventional Fed Measures: the Fed Balance Sheet Treasuries = normal stuff!; CPLF = commercial paper funding facility; MBS = mortgage-backed securities 27 Fed balance sheet before and after the crisis 28 Before Fed expansion LM iff IS(i ff - π + risk premium) IS’ i* 2008 Y After Fed expansion LM iff LM’ IS(i ff - π + risk premium) IS’ i* 2009 Y After Fed and Treasury recapitalization (TARP) and other measures which lowered the spread iff LM’ IS’’ IS’ i* 2010 Y 31 Fiscal Policy in the Liquidity Trap: Components of US stimulus legislation Source: CBO, presentation of Elmendorf, June 2009 32 Without stimulus TR iff IS(2008) i* Y With stimulus TR iff IS(2008) IS(2010) i* Y CBO’s estimate of impact of stimulus on economy My forecast 35 Source: CBO, presentation of Elmendorf, June 2009,; Nordhaus, Nov 2010. When will it ever end? 36