Survey

* Your assessment is very important for improving the workof artificial intelligence, which forms the content of this project

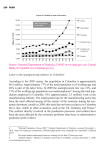

www.thedeal.com vol. 9 no. 15 october 3 — october 16, 2011 Feature Investing Colombia emerges After years of narco-trafficking and terrorism, the third-largest nation in South America is growing fast, driven by commodities, a booming financial economy and monetary discipline. Now it’s looking abroad By Matt Miller Feature Investing C olombia’ s largest conglomerate , Grupo de Inversiones Suramericana SA, turned heads toward the end of July when it won the auction for ING Groep NV’s Latin American life insurance, investment management and pension fund operations. With its ¤2.615 billion ($3.73 billion) bid, Grupo Sura beat out U.S. insurance behemoths such as Prudential Financial Inc., Principal Financial Group Inc. and Metropolitan Life Insurance Co. ¶ The purchase is the priciest ever for a Colombian company. It makes Grupo Sura a major player in global pension fund management, more than doubling assets under management, to $130 billion, and giving the company significant financial beachheads in Mexico, Uruguay and Chile. “We weren’t looking for such a large acquisition,” says Andrés Bernal Correa, the group’s chief finance and investment officer, as he explains his company’s recent moves to expand regionally through M&A. “But we were happy to find it.” Others in Colombia share in this sense of exuberance and pride. The Grupo Sura deal is another high-profile indication that the country’s business community is coming of age globally. “Until recently, Colombian companies weren’t big international players or expanding across frontiers. That has changed a lot,” says Álvaro Hernán Mejía. An investment veteran in Colombia, Hernán is co-founder of the Bogotábased stock brokerage Correval SA, where he heads investment bank operations. “Strategic investments are starting to take off.” Grupo Sura’s M&A activity is only one sign that Colombia-related investment is in the midst of dramatic change. In August, Colombian paper products company Carvajal SA acquired Grupo Convermex SA de CV, a Mexican plastic goods maker, for $180 million, while Sam Zell’s Equity International announced a $75 million stake in Colombian real estate company Terranum Development. An enviable mix of economic drive and monetary discipline characterize the country today. Booming exports, inbound investment and consumer demand all propel the economy these days, while inflation remains low, com- mercial banks strong and sovereign debt manageable. “We have a dynamic economy. We are a commodity producer with high commodity prices. We are attractive to foreign investors,” says soft-spoken Central Bank of Colombia Gov. José Darío Uribe. “We now have the highest terms of trade in Colombian history.” That kind of confidence resonates among Colombians and Colombia watchers. “In macro terms, it’s in the best shape I’ve seen in decades,” says Richard Frank, the president and CEO of Darby Overseas Investment Ltd., the Washington-based emerging-markets private equity firm that first invested in Colombia 16 years ago and has made four investments in Colombian companies. “I used to be really on the defensive for investing in Colombia,” he continues. Now, “it’s one of the most successful Latin American destinations we have.” In late June, Fitch Ratings upgraded Colombia’s foreign debt to investment grade. Fitch was the last of the three ratings agencies this year to boost Colombia’s debt profile after 12 years categorized as junk. All this may come as a surprise to Americans who still know Colombia for its notoriety as an illegal drug center. “Prudent and consistent macroeconomic management has resulted in low inflation and higher growth compared with peers,” Fitch wrote in its upgrade. “Colombia has been among the most actively reforming sovereigns. The [President Juan Manuel] Santos administration has moved forward with an impressive legislative and executive agenda designed to increase growth prospects, and improve fiscal credibility and predictability.” Brazil may hold center stage when it comes to economic performance in Latin America, although some are beginning to wonder whether the hype is outpacing the reality. Colombia, by contrast, remains underappreciated and a bit of a sleeper. “Colombia is the next upcoming emerging market,” argues Juan Carlos González, foreign investment vice president with Proexport Colombia, the government’s investment and tourism authority, which sponsored this reporter’s trip to the country. Whether Colombia will blossom into Latin America’s newest star is far from certain. Impediments remain, and even the country’s most avid boosters agree its infrastructure is woeful. At the very least, however, Colombia is becoming a country that has outgrown the caricature. “I don’t see many clouds on the horizon,” says Juan Muñoz, Bogotá-based executive director for J.P. Morgan Chase & Co. There aren’t many places where that’s the case these days. In a sign of Colombia’s growing financial confidence, the Santos government is laying the groundwork for fiscal sustainability through both mandated Feature Investing photographs by Matt Miller Feature Investing limits to spending and reforms in the use of oil and mining royalties. The government proposed four separate development funds in July, which are now subject to mandated review by the courts to ensure they are constitutional. Germán Arce Zapata, the Ministry of Finance’s director general of public credit and the national treasury, says the funds would be independently supervised and administered; he likened the board to that of the central bank. The system has been designed to ensure that the government won’t expropriate funds earmarked for local projects. Arce describes a pool of some $20 billion over the next decade for a development fund targeted at the country’s various regions—a sizable amount for a country of Colombia’s size. According to Arce, the central government will first focus its royaltiesrelated dividends on reducing budget deficits and levels of debt. Optimism isn’t limited to the government; it pervades boardrooms, banks and balance sheets; it’s carried slowly along the traffic-snarled streets of Colombia’s largest city and capital, Bogotá, a city of 8 million, some 8,612 feet above sea level in the Andes. New construction punctuates Bogotá’s urban expanse, which spills down from the Eastern Cordillera of the Andes and onto a high plateau, known locally as the Sabana de Bogotá. Well-dressed workers rush to their offices while residents stroll parks and sidewalks, pack giant shopping malls and crowd restaurants and bars. In August Colombia hosted the FIFA U-20 World Cup, the international soccer tournament for players under 20. That kind of an event would have been unimaginable just a few years back, says Santiago Gutiérrez-Borda, a partner with the Bogotá-based law firm José Lloreda Camacho & Co. All this represents a kind of societal exhale after long years of anxiety and uncertainty from all the violence. “There’s a real sense of national pride in the culture and the current economy,” says Frank. Colombia’s global image is slowly improving, though it continues to lag behind what’s happening on the ground. Quick. Hear the words Cali and Medellín, and what comes to mind? Economically vibrant cities or drug cartels? With American aid, the Colombian military shut down the country’s major drug cartels; violent drug wars by and large then moved north to Mexico. Colombia’s government also successfully disarmed paramilitary gangs, and the army effectively beat back left-wing guerrillas. Gone are the days when narco-trafficking, rightist death squads and kidnappings distinguished the country—though those forces continue to haunt this nation of 47 million, Latin America’s third-largest country. When it comes to righting a perception, “Colombia has a long way to go,” says Muñoz. “It’s always easier to remember the bad news rather than the good news.” Colombia has not magically erased all traces of its past. Cocaine still courses through the country. Some 8,000 rebels remain holed up in the mountains and lord over isolated communities. The Santos government is only now moving to return farms to thousands of displaced peasants, victims of paramilitary land grabs; that task could take several years. Unemployment tops 11%, high compared with the rest of booming Latin America. And even now, wealthy Colombians tend to keep low profiles as fears linger of once-widespread extortion and kidnapping. “People are very humble. They don’t show off,” says Muñoz. Security isn’t the only hangover. Bogotá suffers monumental traffic jams, while transportation links between major cites and the rest of the country remain sketchy. Millions lack adequate housing; the Santos government is targeting construction of 1 million new housing units over the next three years. And corruption, by all reports, remains endemic. In its latest annual corruption perception index, Transparency International ranks Colombia 78th out of 178 countries, the same as China. In a sign of both an independent judiciary and a crooked polity, some 50 politicians, including governors, mayors and members of the Congress of Colombia have been jailed for links to right-wing paramilitary groups, according to Ricardo Ávila Pinto, the publisher of the daily business newspaper Portafolio. Despite all this, Colombia’s change has been dramatic. That is reflected in investment, individual and institutional, domestic and international. “There’s been a huge transformation in market sentiment, in investment perception,” says Juan Pablo Córdoba Garcés, who heads the Bolsa de Valores de Colombia SA, or BVC, the country’s stock exchange. “It’s very exciting.” Colombia’s recent history has been exciting as well, just not in a good way. The ’90s was pretty much a lost decade. Heavily armed narcotics traffickers, paramilitary gangs and two left-wing organizations—the Fuerzas Armadas Revolucionarias de Colombia, or FARC, and the Ejército de Liberación Nacional, or ELN—battled each other and the government, terrorized large swaths of Colombia and tore apart the country. The economic results were predictably bad. Investment dried up and inflation soared. The best and the brightest fled for the United States and elsewhere. A banking and credit crisis hit Colombia in 1999. It marked an economic nadir, the only time since the Great Depression that Colombia’s economy contracted. This mortgage-related meltdown was eerily similar to that in the United States almost a decade later. Most Colombian banks—80% by some estimates—either failed or were bailed out by the government. “We spent quite a significant amount of money paying off the debt from the banking crisis,” Arce says. That time weighs heavily on Colombians. “We learned our lessons in the ’90s,” says Uribe. Colombia slowly pulled itself out of its economic tailspin in the first half of the past decade, then accelerated. While the rest of the world battled the global financial free fall in 2008, Co- Feature Investing lombia remained above the fray. Uribe describes a meeting with other regional central bank governors and how their tales of woe contrasted with Colombia’s still-humming economy. “From the beginning [of the 2008 crisis] we did very well,” he says. Commercial banks weathered the storm. Monetary authorities refused to intervene in the market and allowed the peso to float freely as it had since September 1999. (The Colombian peso has appreciated about 14% over the past three years against the dollar, even as the central bank regularly buys dollars.) Uribe says one critical decision the Finance Ministry made in 2004 was to tackle the currency mismatch of the public debt. That year, 70% of public debt was dollar-denominated, with only 30% denominated in Colombian pesos. By the time the international financial crisis hit four years later, that ratio was reversed. “That was very useful during the financial crisis,” he says. “During the crisis, our FX intervention was negligible.” Part of this focus was a policy that prohibited foreign exchange borrowing to hedge peso debt. “A fixed exchange rate provides an incentive to get external debt. It encourages people and firms to think that the exchange rate will always be stable and that they can get foreign financing at a lower interest rate and with a fixed exchange rate,” Uribe says. In Colombia, he continues, “We don’t allow the financial sector to have currency mismatches, and term mismatches in foreign currency. A bank goes out and gets a $1 million loan. It has to lend internally in dollars. If it’s a three-year loan, the bank can lend in dollars, but with a maturity of three years or less.” Colombia’s commercial banking sector has been transformed from liability to asset. Frank, for one, commends banking capital adequacy requirements in which Tier 1 capital reaches 15% of total assets, the highest in Latin America and far higher than Europe and the United States. “Banks are very well managed,” adds Ávila, who says the country’s major financial institutions are beginning to flex muscles regionally. He cites Grupo Aval, Colombia’s largest bank, which last year paid $1.9 billion to General Electric Co.’s GE Capital Corp. for BAC Credomatic GECF Inc., which has operations in Costa Rica, El Salvador, Guatemala, Honduras, Nicaragua, Panama and Mexico. Uribe and others cite 2004 as a kind of base year for the economic turnaround. The government finally turned the corner in its fight against the drug cartels and leftist guerrillas. Higher commodity prices and the beginning of renewed investment also marked that time. After 4.3% growth in 2010, forecasters expect Colombia’s economy to grow some 5% this year, with inflation of 3% to 4%. The research arm of Spanish bank Banco Bilbao Vizcaya Argentaria SA projects gross domestic product growth next year of 5.4%. (What effect the recent global market volatility will have on growth remains a question.) The 5% growth rate trails that of Peru and Chile this year. However, Banco Bilbao Vizcaya warns that, if anything, an overheated economy in Colombia remains the main concern. Colombian officials say they’re satisfied with “6+% by end of 2014,” Arce says. “Critics say, ‘Why not grow 9%?’ ” Arce continues. “We say because we have to grow 6% for the next 100 years, not 9% for the next couple [years], and then get hit by the next crisis and spend “A fixed exchange rate provides an incentive to get external debt. It encourages people and firms to think that the exchange rate will always be stable and that they can get foreign financing at a lower interest rate and with a fixed exchange rate.” —Uribe Feature Investing the next decade solving the crisis so we can get back to 6. We’re trying to get the economy to cruise speed.” To a major degree, Colombia is flourishing because it produces some of the world’s most strategic commodities. Oil, gold and coffee alone compose half the country’s exports. Coal-related revenue is also surging. The government forecasts oil production will double over the next decade. In an interview, Javier Gutiérrez Pemberthy, the CEO of Colombia’s oil giant Ecopetrol SA, agrees with this goal, but says that will require the discovery of new fields and enhanced production, primarily in Colombia, as well as “opportunistic” acquisitions. (Last year, Ecopetrol teamed up with Talisman Energy Inc. to buy BP Exploration Co. Colombia. Ecopetrol holds a 51% stake in the joint venture that paid $1.9 billion for BP’s Colombian subsidiary.) Ecopetrol projects capex for the decade ending 2020 will be a staggering $80 billion, 25% of which is earmarked for exploration. The ability to explore and enhance production is in part because security is no longer as big an issue. Gone are the days when Bloomberg terminals offered a running tally of oil pipeline attacks (and kidnappings, for that matter). Increased production, says Ávila, should get a filip as well because of the diminished activity of its oil-producing neighbor, Venezuela, under the unpredictably autocratic Hugo Chávez. “Thanks to Chávez, 1,000 [petroleum] engineers have moved to Colombia,” he says. (Uribe, the central bank governor, says the downside of Venezuela’s deteriorating economy is that it buys fewer Colombian-made goods, including motor vehicles and other manufactured products. “We exported to Venezuela more than $6 billion in 2007. Now we’re exporting about $1.5 billion,” he says, adding that many of those Colombian exporters have been waiting to get paid “a long time.”) Oil and mining have traditionally accounted for the bulk of private investment, some 70% of foreign direct investment in the years 2009, 2010 and the first quarter of 2011, according to government figures. But investment is diversifying. According to government officials, FDI this year should top $10 billion, which could match the 2008 record of $10.58 billion. In the late ’90s and early 2000s, FDI averaged only $1.5 billion to $2 billion a year. Domestic and foreign investors alike are signing checks as never before. “There’s confidence of investors here in Colombia and confidence of investors abroad,” says Lloreda Camacho’s Gutiérrez, whose clients include CocaCola Co., Unilever NV/plc and Spirit Airlines Inc. Gutiérrez, for example, advised the Colombian supermarket chain Grupo Éxito SA on the ¤700 million purchase in June of two Uruguay supermarket chains, Grupo Disco del Uruguay and Devoto SA. France’s Groupe Casino owns a 54% stake in Éxito. Éxito says it will issue up to $1.4 billion worth of new shares on Colombia’s stock exchange to underwrite this expansion. Colombia’s capital markets are undergoing notable change. “Equity markets were stagnant two, three years ago, [but] they will progress very rapidly,” says Dario Duran, a director of Altra Investments, a Bogotá-based private equity shop. Perceptions of the country’s capital markets vary, and the discussion is sometimes half-empty versus half-full. The Bolsa de Valores de Colombia has only 90 listed companies. This year, three initial public offerings have taken place, with four or five more issues in the pipeline. Large, old-guard institutions dominate the exchange. With 2010 revenue of $21 billion and net income of $4 billion, Ecopetrol alone composes more than 39% of the exchange’s total market cap, even though the float represents only about 12% of the company’s total shares. Ecopetrol was owned 89.9% by the state, after the government divested shares in a $3.3 billion IPO in 2007. This August, Ecopetrol executed a follow-on offering, which was a victim of bad timing and fell slightly short of expectations. Investors subscribed to 2.4 trillion Colombian pesos [$1.34 billion] of the Col$2.5 trillion shares being sold, an offer that represented 1.67% of total shares. The company’s Gutiérrez says that under the circumstances, with global markets tumbling and twisting, “for us, it was a success.” Hernán, the investment banker, bemoans a lack of choice in the stock market. “Colombia doesn’t have a lot of players,” he says. “There’s one listed company in foods, three in oil, one in cement.” Gutiérrez says that limited marketplace affects his company as well. He points to the daily float, which is pretty much split down the middle between Colombian investors and ADRs, even though by numbers of shareholders, Colombia represents 99% of the total. “The real test for us is being part of a market like this,” he says, on the floor of the New York Stock Exchange, where he journeyed in September to celebrate Ecopetrol’s 60th anniversary of incorporation and ring the closing bell. He Feature Investing talks of the need in both the bond and equity markets to be recognized internationally by investors as a global energy player. That is beginning to happen, Gutiérrez believes. “I expect in the future, the number of shares traded in this market will increase, the number of ADRs will increase.” The Colombia exchange’s Córdoba, by contrast, emphasizes not the limited issues, but the dramatic growth: $2 billion in trading and a $25 billion market cap in 2004 versus $28 billion in trading and $217 billion market cap last year. Five years ago, five companies were trading more than $1 million a day, he says. Today, there are 23. The percentage of foreign exposure is increasing even more rapidly, having doubled from 4% last year to 8% today. “If you look at Colombia today versus five years ago, the transformation has been tremendous,” he says. In late May, the Colombian stock exchange inked a marketing and trading agreement with exchanges in Peru and Chile. Termed MILA, the Mercado Integrado Latinoamericano— not a full merger, Córdoba stresses—allows investors in one exchange to trade in the equities of the other two. An IPO on one becomes, in practical terms, an IPO in all three. “There will be more investments, more trades being done, more alternatives to issuers,” Córdoba insists. The integration expands not only the markets in these three countries, but, potentially, Central America as well, he says. Others believe it’s just a matter of time until the public equities market expands. J.P. Morgan Chase’s Muñoz, for one, sees smaller and midcap issues as “probably the next stage” in markets development. Duran agrees. “Sooner or later, we’ll experience smaller IPOs being successful,” he says. Colombia’s pension funds provide the potential for a huge driver in both private and public equities. “Colombian pension funds have huge portfolios. They want to diversify, and are eager for diversification opportunities,” Duran says, since “most have high concentrations in fixed income, both in the equivalent of treasuries and private debt.” Pension funds account for only 25% of equities trading on the Colombian bourse, according to Córdoba. That could well rise as changes in legislation aid a shift from fixed income. For example, Colombian pension funds can now co-invest directly in private equity through special-purpose vehicles. The composition of investments in pension funds is shifting too. According to Santiago Montenegro Trujillo, the president of the private pension fund association Asofondos, the degree of pension fund risk allowed by law is linked to age. A younger contributor can opt for up to 70% equities. Investments in alternative assets such as private equity, normally limited to 5% of total portfolio, can reach 7% in riskier funds. At the same time, individual investors are flexing their muscles. “Colombia is going through a process where individuals are getting richer,” says Hernán, citing per capita income that has doubled in six years. “That has caused people here to look for alternative investments.” The composition of those investors is changing as well. “For a bunch of years, the equities market was thought to be only for rich people, an exclusive club,” says Muñoz. “Now, ordinary people are starting to feel they are part of it.” Private equity is rapidly gaining ground and local acceptance (see sidebar). However, while Colombia has two angel investor networks, it has no organized venture capital, or at least not one that would be recognizable in the U.S. or Europe. “Entrepreneurs are looking for venture capital,” says Camilo Villaveces Atuesta, who heads Ashmore Management Co. (Colombia) SA. That’s the next step, says María Cristina Albarracín, the director of the private equity division at Banco de Comercio Exterior de Colombia SA, or Bancóldex, the government’s development bank. One possible catalyst is a $100 million fund-of-funds that will invest in technology and innovation venture funds. Terms of reference should be out in the next few months, Albarracín says, and would be linked to the slice of resources royalties allocated to what the government calls science, technology and innovation. Colombia’s legislature would decide specific allocations. The government has already committed to create a biotech venture fund. Bancóldex will hire consultants shortly to help work out details, Albarracín says. Juan Sebastián Pardo is president of Credifamilia Cia. de Financiamiento SA, and he illustrates the need for startup capital. Pardo completed his M.B.A. at Stanford University in 2007. Like an increasing number of his generation who have been educated abroad, Pardo decided to return to Colombia and start his own business. He hit on mortgage finance. Adjustable-rate mortgages disappeared after the crisis of 1999, and banks turned cautious. A long, pent-up demand for housing finance has bedeviled Colombia. “Mortgage penetration is just 3, 4%, the lowest Feature Investing in Latin America,” says Pardo. Pardo needed just $10 million in capital for a banking license, but that took two years, thanks in part to the financial crisis. Credifamilia finally gained a banking license in February and now has private equity chasing it for further investments. It targets affordable housing, in which the government subsidizes interest rates. “We are hoping to make Col$150 billion in loans in the first two years,” he says. Pardo is critical not only of the lack of startup capital, but also of those seeking it. “You can always get $100,000 to start a restaurant,” but “there’s a lack of entrepreneurial culture that thinks big.” As more Colombians return home, that could change. “People are coming back. Multinationals are coming back, and they’re looking for local talent. I have several friends and relatives who are coming back,” says Muñoz. Cross-border acquisitions are more commonplace as Colombia develops its equities markets and the companies themselves bulk up and expand. “We’re in the process of becoming regional players,” says Duran, whose firm is trying to follow this doctrine, with investments primarily in Colombia and Peru, but also in Central America, Chile and Argentina. One example: his firm’s acquisition, along with Dutch development fund Nederlandse Financierings-Maatschappij voor Ontwikkelingslanden NV, of Colombian specialized-packaging company Proenfar SA for an undisclosed amount. Proenfar has an Argentine subsidiary, markets throughout Central America and the Caribbean and is in the final stages of a transaction in Mexico. “In the Andean region, there’s a lot of convergence—geographical, political, economic,” Duran says. “We see today a lot of capital flow into this region. A lot of Colombian companies are going to Chile and Peru; a lot of Chilean and Peruvian companies are coming to Colombia.” Nowhere is that expanded reach more apparent than with Grupo Sura, AS FEATURED IN The Deal (ISSN 1545-9878) is published biweekly except in August and December by The Deal, LLC. © Copyright 2011 The Deal, LLC. The Copyright Act of 1976 prohibits the reproduction by photocopy machine or any other means of any portion of this publication except with the permission of the publisher. The Daily Deal is a trademark of The Deal, LLC. www.Thedeal.com whose domestic empire extends from cement to chocolate, life insurance to leasing. The conglomerate accounts for a staggering 6.5% of Colombia’s GDP. Finance director Bernal says Sura ran up against limits of domestic expansion in the past decade. “We control more than 50% of Colombia’s cement market, more than 60% of processed foods,” he says. “It’s almost impossible to do more acquisitions in Colombia.” Over the past six or seven years, Bernal says, Grupo Sura has made some 25 international acquisitions. The pace began to quicken three years ago when Grupo Sura “decided our next step was internationalization,” he says. Strategically and financially, Bernal says, “we have the capacity to grow through acquisitions.” The ING acquisition, which Grupo Sura anticipates will close late this year or early next year, ratchets up the stakes considerably. “We are confident we have the resources to digest this,” Bernal says. “Then, in a couple years, who knows?” n