Survey

* Your assessment is very important for improving the workof artificial intelligence, which forms the content of this project

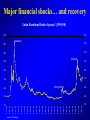

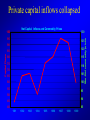

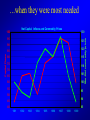

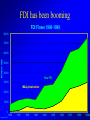

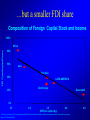

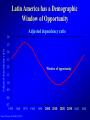

LATIN AMERICA: IS IT MOVING FORWARD? Ricardo Hausmann Kennedy School of Government Harvard University Outline • • • • • • • Structural reform and growth Demographic window of opportunity Financial Turmoil and contagion ‘Original sin’: an interpretation of the problem The boom in FDI: what does it mean? The recovery in Latin America Prospects for long-run growth Latin America recovered in the 1990s GDP Growth 6 5 porcentaje 4 3 2 1 0 1965-70 Fuente: IDB 1971-80 1981-90 1991-98 Based on significant structural reform Avance de las políticas estructurales 80% Variación relativo al máximo Trade 60% Financial 40% 20% 0% Fuente: Lora, 1997 …that is still incomplete by area Avance de las políticas estructurales 80% Variación relativo al máximo Trade 60% Financial 40% Tax Privatization 20% Labor 0% Fuente: Lora, 1997 More reforms, more growth Cambios en Tasas de Crecimiento Cambios en Crecimiento y en Políticas Estructurales (1993-95 vs. 1987-89) 15% Perú 10% Nicaragua El Salvador 5% Argentina Trinidad and Tobago Brazil Bolivia Ecuador Guatemala Colombia 0% Costa RicaUruguay Venezuela -5% 0% República Dominicana Paraguay Honduras Mexico Chile Jamaica 5% 10% 15% 20% 25% 30% Cambios en Indices de Política Fuente: Lora y Barrera, 1997 35% 40% 1997 was a very good year Real GDP Growth (Average 8 Largest Economies) 6.0 6.0 5.0 5.0 4.0 4.0 3.0 3.0 2.0 2.0 1.0 1.0 0.0 90 91 92 93 94 95 96 97 0.0 …but then came a bad streak • • • • • • Asian Financial crisis Collapse in the terms of trade El Niño Russian crisis and contagion Hurricanes Georges and Mitch Brazilian crisis 35 Index 01/02/97 = 100 1/2/99 12/2/98 11/2/98 10/2/98 Hong Kong 9/2/98 8/2/98 7/2/98 6/2/98 5/2/98 4/2/98 3/2/98 2/2/98 1/2/98 12/2/97 Thailand 11/2/97 10/2/97 9/2/97 8/2/97 7/2/97 6/2/97 5/2/97 4/2/97 3/2/97 2/2/97 1/2/97 The collapse in the terms of trade Commodity Prices 125 115 Copper 105 95 Wheat 85 75 65 Oil 55 45 Russia 100 Source: JP Morgan. 3-Dec-98 3-Oct-98 3-Aug-98 3-Jun-98 3-Apr-98 3-Feb-98 3-Dec-97 3-Oct-97 3-Aug-97 500 3-Jun-97 3-Apr-97 3-Feb-97 3-Dec-96 3-Oct-96 3-Aug-96 3-Jun-96 3-Apr-96 3-Feb-96 3-Dec-95 3-Oct-95 3-Aug-95 3-Jun-95 3-Apr-95 3-Feb-95 3-Dec-94 3-Oct-94 Major financial shocks… and recovery Latin Eurobond Index Spread (1994-98) 1,700 1,700 1,500 (Mexico) 1,500 1,300 1,300 1,100 (Russia) 1,100 900 900 700 700 (Hong Kong) 500 300 300 100 Private capital inflows collapsed Net Capital Inflows and Commodity Prices 130 95 125 90 120 Capital Flows 85 80 115 75 110 70 105 65 60 100 55 95 50 90 45 40 85 1991 1992 1993 1994 1995 1996 1997 1998 1999 Non-fuel commodity prices 100 …when they were most needed Net Capital Inflows and Commodity Prices 130 95 125 90 120 Capital Flows 85 80 115 75 110 70 105 65 60 100 55 95 50 90 45 40 85 1991 1992 1993 1994 1995 1996 1997 1998 1999 Non-fuel commodity prices 100 …only marginally offset by official financing ... 90 80 70 60 50 40 30 20 10 0 -10 -20 1997 Private Net Flows 1998 Official Inflows 1999 Acum of Reserves CAD …causing a collapse in imports Trade and Current Account (excl. Mexico) 160 140 120 100 80 60 40 20 0. 1991 1992 1993 1994 1995 1996 1997 1998 1999 -20 -40 -60 -80 Exports(-Mex) Imports(-Mex) Trade Balance(-Mex) CA(-Mex) …that exceeded the fall in exports Comparing Recessions (absolute change between periods) 35 Imports 25 Exports 15 Trade Balance 5 -5 -15 -25 -35 Source: WEO 1994-1995 1997-1999 …and caused a collapse in growth Real Growth in Latin America 6 5 4 3 2 1 0 1991 Source: WEO 1992 1993 1994 1995 1996 1997 1998 1999 …that affected most countries Fall in Growth (Average 1999-98 vs 1997) Venezuela Argentina Ecuador Chile Guyana Peru Western Hemisphere Uruguay Mexico Brazil Colombia Suriname El Salvador Dominican Rep. Belize Bahamas Panama Grenada Honduras Paraguay Trinidad&Tob Guatemala Dominica Nicaragua Bolivia Barbados Haiti Jamaica Costa Rica -2 0 2 4 6 8 10 Latin America: no Fireworks Since the East Asian crisis • No systemic banking crises • No widespread currency crises • No inflationary crises • No debt crisis • No reversal of reforms Exceptions • Ecuador is a real exception • Brazil: not really an exception, just a currency realignment that has not generated any other symptom • Colombia? Venezuela? Capital flows have been recovering 4.0 Figure 12a: Net Private Capital Inflows, Portfolio, FDI and Loans in Latin America, 1996-2000 3.5 Private Capital Inflows 3.0 2.5 2.0 FDI 1.5 Portfolio 1.0 0.5 Loans 0.0 1996 -0.5 -1.0 Note: As percentage of GDP. Source: Balance of Payments, IMF. 1997 1998 1999 2000 30 Source: Goldman Sahcs Commodity Indexes 05/17/00 04/17/00 03/16/00 02/15/00 01/14/00 12/15/99 11/15/99 10/14/99 09/14/99 08/13/99 07/14/99 06/14/99 05/13/99 40 04/13/99 03/12/99 02/10/99 90 01/11/99 12/10/98 11/10/98 10/09/98 09/09/98 08/10/98 07/09/98 06/09/98 05/08/98 04/08/98 03/09/98 02/05/98 01/06/98 12/05/97 11/05/97 10/06/97 09/04/97 08/05/97 07/04/97 06/04/97 05/05/97 04/03/97 03/04/97 01/31/97 01/01/97 Commodity prices have stopped falling Commodity Indexes (Index Jan 97=100) 120 110 100 Agricultural 80 70 60 50 Energy World outlook looks good • • • • Continued recovery in Europe …and in East Asia …mild recovery in Japan …and a roaring US economy …and the region is expected to recover Real Growth in Latin America Annual percent change 6 5 4 % 3 2 1 0 1991 Source: WEO 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 What will the future bring? • Are we facing another boom? • Will it be followed by another crisis? • …or will it be sustained? Four scenarios ahead Dangerous Safe Deep Boom - Crisis High, sustained flows Shalow Mild boomcrisis No boomno crisis The origin of crises: the mainstream approach • Booms and crises were caused by moral hazard • and an inadequate perception of risks Mainstream View #1 Shallow and safe • Large recent losses • …and changes to international financial architecture: – lower bail-outs, more bail-ins – more flexible exchange rates • …will reduce moral hazard, giving rise to a more moderate but sustainable scenario. Mainstream View # 2 Deep and dangerous • Booms and crises are caused by moral hazard • ...but nothing substantial has changed • …so we will get another boom, followed by another crisis The origin of crises: the mismatch approach • Crises are not caused by moral hazard. • They are caused by mismatches which leave countries vulnerable to self-fulfilling attacks. – ORIGINAL SIN: unable to borrow internationally in own currency • Changes in architecture have made things worse • The mismatches are in the stocks, not in the flows. Original sin: World Comparison Debt in Currency X Over Debt in Country X, 1998 (Money Market Instruments and Bonds) United States Luxembourg Switzerland Japan Italy South Africa New Zealand United Kingdom Germany France Portugal Hong Kong Netherlands Australia Denmark Poland Spain Canada Greece Taiwan Belgium Ireland Sweden Finland Cyprus Norway Austria Singapore Argentina Indonesia Thailand Mexico Malaysia Source: BIS 0 0.5 1 1.5 2 2.5 View # 3 Shallow and dangerous • • • • • Countries do not deal with the mismatches Risks are perceived as high, Flows will be low ...but still a crisis. Deep and dangerous also a possibility if the market focuses on the good equilibrium View #4 Deep and Safe • Countries deal with the mismatches: – developing the ability to borrow internationally in their own currency – adopting common currency that does not have original sin. • The market can support large, sustainable flows FDI has been booming FDI Flows 1990-1999 80000 70000 Millions US$ 60000 50000 40000 New FDI 30000 M&A,privatization 20000 10000 0 Source: ECLAC 1990 1991 1992 1993 1994 1995 1996 1997 1998 1999a …but in the context of declining total flows Net Commercial Capital Flows and Its Composition for Latin America 120 1.2 FDI / Total Flows (%) 100 1 80 0.8 60 0.6 FDI 40 0.4 20 0.2 0 0 1996 Source: IIF 1997 1998 1999 Percentage US$ Billions Net Commercial Flows Is FDI like good cholesterol? Conventional wisdom • Capital is like cholesterol • Good cholesterol FDI – Brings technology, market access, managerial skills – It is “bolted down” – It is attracted by long-term prospects and good institutions Conventional wisdom • Bad cholesterol “Hot” portfolio money – Driven by short-term speculative considerations – Affected by moral hazard – First to flee More development, more foreign capital Foreign Capital Stock and Income Developed Foreign Capital Stock / GDP 60% 50% 40% 30% LATIN AMERICA 20% East Asia 10% Africa East Europe Asia 0% -10% 2.5 3.0 3.5 GDP per capita (log) 4.0 *Data refers to stocks of 1997 in current dollars and GDP in PPP current dollars. The GDP per capita is a weighted average of countries for the same year. Source: IFS, WB and RES-IDB. 4.5 …but a smaller FDI share Composition of Foreign Capital Stock and Income 100% FDI / Total Capital Flows Africa 80% 60% Asia East Asia 40% LATIN AMERICA East Europe 20% 0% 2.5 3.0 3.5 GDP per capita (log) Developed 4.0 *Data refers to stocks of 1997 in current dollars and GDP in PPP current dollars. The GDP per capita is a weighted average of countries for the same year. Source: IFS, WB and RES-IDB. 4.5 FDI/GDP: Outcome of opposite forces FDI Stock and Income 8% LATIN AMERICA 7% East Asia 6% FDI/GDP Developed 5% East Europe 4% Africa 3% Asia 2% 2.5 3.0 3.5 GDP per capita (log) *Data refers to stocks of 1997 in current dollars and GDP in PPP current dollars. The GDP per capita is a weighted average of countries for the same year. Source: IFS, WB and RES-IDB. 4.0 4.5 Richer, larger, more open economies don’t have higher FDI-shares Correlations with Volume and Composition of Capital Flows 0.8 Volume 0.6 0.4 FDI/GDP 0.2 0.0 -0.2 -0.4 Composition -0.6 Income Size Openness Riskier countries get less capital, but a larger share of FDI Correlations with Volume and Composition of Capital Flows 0.6 Composition 0.4 0.2 FDI/GDP 0.0 -0.2 Volume -0.4 -0.6 Country Risk Resource rich, distant countries don’t get more capital, but higher FDI-share Correlations with Volume and Composition of Capital Flows 0.6 Composition 0.4 0.2 FDI/GDP 0.0 -0.2 Volume -0.4 -0.6 Subsoil Resources Distance Better finance, better institutions don’t beget more FDI-share Correlations with Volume and Composition of Capital Flows 0.8 0.6 0.4 Volume FDI/GDP 0.2 0.0 -0.2 -0.4 Composition -0.6 Financial Development Quality of Institutions Original sin increases FDI-share Correlations with Volume and Composition of Capital Flows Composition 0.4 0.2 FDI/GDP Volume 0.0 -0.2 -0.4 Original Sin “Good things” are associated with more foreign capital inflows but a lower share of FDI Controlling for income, size and openness, lower risk and better institutions do not increase the share of FDI Hypothesis • FDI is booming because firms are redefining their shape so as to circumvent lousy debt markets • FDI is a solution to the mismatch problem caused by original sin – Long term and no currency denomination • FDI may also limit liquidity problems • Implications for optimal financial structures – IPOs to domestic market or M&A to a strategic investor? Looking into the more distant future Structural reforms are continuing Bank Supervision Pensions Funds Capital Market Privatiz. & Regulations Comercial(X,M) Foreign Investment Education Tax Sistem Justice Labor Property Rights Health 0 0.2 0.4 0.6 0.8 Source: Survey. Note: Difference with respect to 3 years ago (based on scale 0-5) 1 1.2 Latin America has a Demographic Window of Opportunity Adjusted dependency ratio 1.6 Adjusted dependency ratio 1.5 1.4 1.3 1.2 Window of opportunity 1.1 1.0 0.9 0.8 0.7 1950 1960 Source: Duryea and Székely (1998) 1970 1980 1990 2000 2010 2020 2030 2040 2050 ¿What does demographic opportunity imply? • More work • More savings • More education THE OPPORTUNITY TO BE THE FASTEST GROWING REGION IN THE WORLD