Survey

* Your assessment is very important for improving the work of artificial intelligence, which forms the content of this project

Coloured vote constitutional crisis wikipedia , lookup

Constitutional Court of Thailand wikipedia , lookup

Separation of powers under the United States Constitution wikipedia , lookup

United States Bill of Rights wikipedia , lookup

United States Constitution wikipedia , lookup

Constitutional amendment wikipedia , lookup

Seventeenth Amendment to the United States Constitution wikipedia , lookup

United States constitutional law wikipedia , lookup

Eighth Amendment to the United States Constitution wikipedia , lookup

Fifth Amendment to the United States Constitution wikipedia , lookup

Fourteenth Amendment to the United States Constitution wikipedia , lookup

Disenfranchisement after the Reconstruction Era wikipedia , lookup

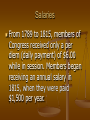

Terms and Cases Module 11 Chapters 11 and 12 Cases – Chapters 11 Pollock v. Farmers’ Loan & Trust Co. (1895): Invalidated the income tax as unconstitutional; the decision was overturned by ratification of the Sixteenth Amendment. The Sixteenth Amendment was designed to give constitutional authority for a national income tax. The original Constitution had provided in Article I, Section 9, that: No Capitation, or other direct, Tax shall be laid, unless in Proportion to the Census or Enumeration herein before directed to be taken. On the basis of this elusive language that did not specifically define a “direct tax,” the Supreme Court had, in Pollock v. Farmer’s Loan and Trust Company (1895), declared that a tax on income was a direct tax and that, as a tax on such income rather than on a state’s population, it was therefore void. The Sixteenth Amendment reversed this judgment, the third such amendment to overturn a Supreme Court decision Terms – Chapter 11 Blue Laws: Laws requiring the closure of certain businesses or forbidding the sale of certain items on Sundays. Direct Taxes: Unidentified taxes, prohibited from being laid by Article I, Section 9 except according to a state’s population. The prohibition against direct taxes has been superseded by the legalization of the income tax in the Sixteenth Amendment. Progressive Era: The time period early in the twentieth century during which there was a strong push for reform and democratization. Amendments 16 through 19 are associated with this period. Terms – Chapter 11 Ratification: Formal approval. The Constitution requires that treaties be ratified by two-thirds of the Senate and constitutional amendments by three-fourths of the state legislatures or conventions. Seneca Falls Convention: A convention that met in New York in 1848 and issued a call for women’s suffrage that eventually resulted in adoption of the Nineteenth Amendment (1920). Cases – Chapter 12 Coleman v. Miller (1939) The question of assessing contemporaneousness to amendments has been left in Coleman v. Miller (1939) to Congress, and it accepted the 27th amendment by an overwhelming vote on May 20, 1992. Dillon v. Gloss (1921) stated that an amendment should reflect a contemporary consensus to its limit. On the negative side for the 27th amendment, ratifications spread out over a two-hundred-year period stretch the idea. Harper v. Virginia Board of Elections (1966), the Supreme Court voided the use of such poll taxes in state elections on the authority of the equal protection clause of the Fourteenth Amendment. The right to vote can now be exercised regardless of one’s ability to pay for this privilege. Cases – Chapter 12 Marbury v. Madison (1803): In turning away a request by an individual who had been appointed as a justice of the peace but had never received his commission, the Court ruled that a section of the Judiciary Act of 1789 that seemed to grant the Court original jurisdiction was unconstitutional and therefore void, therefore asserting the Court’s power of judicial review. Lame-duck representatives, readers may recall, created the judicial seats that came to be contested in the case of Marbury v. Madison (1803), which established the principle of judicial review of national legislation. Similarly, in 1873, an outgoing Congress had approved the so-called Salary Grab Act, boosting salaries form $5,000 to $7,500 per year and applying the law retroactively to the beginning of the session, while in 1922 an outgoing Congress had adopted a ship subsidy bill, despite the fact that voters had rejected many of the bill’s sponsors. Cases – Chapter 12 Oregon v. Mitchell (1970) An attempt to extend the franchise to eighteen-year-olds by legislation was struck down by the Supreme Court, congressional power being recognized in the case of federal but not state elections. Fearing that different standards could lead to an election nightmare, Congress proposed and the states quickly ratified the Twenty-sixth Amendment to eliminate this disparity. United States v. Classic (1941) declared that primaries were so integral to the electoral process that they were limited by constitutional restrictions. Terms – Chapter 12 Emoluments: A constitutional term used to refer to salaries or other monetary rewards. Franchise: The right to vote Grandfather Clauses: Provisions, directed against racial minorities and eventually overturned by the courts, which restricted voting to those who could prove that their grandfathers had voted prior to 1867, that is, prior to the time that African Americans were given this right. Terms – Chapter 12 Lame Ducks: Elected officials who are finishing out their terms but already know that they will not be returning to office. The Twentieth Amendment shortened the period during which lame-duck presidents and members of Congress serve. Literacy Tests: Tests, now suspended by law, which were once a prerequisite for exercising the right to vote; such tests, combined with “understanding clauses,” were often administered in a racially discriminatory fashion. Poll Taxes: Taxes levied as a condition to voting. The Twenty-fourth Amendment prohibited the payment of such poll taxes as a condition for voting in federal elections. Suffrage: The right to vote. Ex-Felon Disenfranchisement The roots of felony disenfranchisement laws can be traced back to ancient Greek and Roman traditions. Disenfranchisement was commonly imposed on individuals convicted of "infamous" crimes as part of their "civil death," whereby these persons would lose all rights and claim to property. The practice of disenfranchisement was transplanted to American by English settlers. Ex-Felon Disenfranchisement Upon the passage of the Fifteenth Amendment, giving African-Americans the right to vote, Southern States began to use seemingly neutral voting qualifications e.g. literacy tests, property requirements, grandfather clauses, tests for good moral character and criminal disenfranchisement - to deny the vote to blacks. While disenfranchisement laws had existed long before these practices began, a number of Southern States tailored these laws to maximize their impacts on AfricanAmericans. Unlike most other laws that burden the right of citizens to vote based on some form of social status, felony disenfranchisement laws have been held to be constitutional. Ex-Felon Disenfranchisement In Richardson v. Ramirez, the United States Supreme Court upheld the constitutionality of felon disenfranchisement statutes, finding that the practice did not deny equal protection to disenfranchised voters. The Court looked to Section 2 of the Fourteenth Amendment to the United States Constitution, which proclaims that States which deny the vote to male citizens, except on the basis of "participation of rebellion, or other crime," will suffer a reduction in representation. Ex-Felon Disenfranchisement Based on this language, the Court found that this amounted to an "affirmative sanction" of the practice of felon disenfranchisement, and the 14th Amendment could not prohibit in one section that which is expressly authorized in another. However, many critics, argue that Section 2 of the 14th Amendment does not represent an endorsement of felon disenfranchisement statutes as constitutional in light of the equal protection clause; but is limited only to the issue of reduced representation. Ex-Felon Disenfranchisement The United States Supreme Court has generally upheld felony disenfranchisement laws, but has at the same time struck down those that were clearly intended to disenfranchise particular racial groups, or which allowed disenfranchisement based on the commission of acts so minor that they could not be classified as felonies. Ex-Felon Disenfranchisement Current Application Today, only four states continue to impose a life-long denial of the right to vote to all citizens with a felony record, absent some extraordinary intervention by the Governor or State legislature. These are Florida, Iowa, Kentucky, and Virginia. In July, 2005, Iowa Governor Vilsack issued an executive order restoring the right to vote for all persons who have completed supervision. However, the lifetime prohibition on voting remains Iowa law. Nine other states disenfranchise ex-felons for various lengths of time following the completion of their probation or parole. Almost every state prohibits felons from voting while incarcarated, on probation, or on parole. Salaries The current salary for rank-and-file members of the House and Senate is $158,100 per year. Senate Leadership Majority Leader - $175,600 Minority Leader - $175,600 House Leadership Speaker of the House - $203,000 Majority Leader - $175,600 Minority Leader - $175,600 Current salary for the Chief Justice is around $202,900 per year, while Associate Justices make about $194,200. President’s Salary is $400,000 Salaries From 1789 to 1815, members of Congress received only a per diem (daily payment) of $6.00 while in session. Members began receiving an annual salary in 1815, when they were paid $1,500 per year.