Survey

* Your assessment is very important for improving the workof artificial intelligence, which forms the content of this project

Federal takeover of Fannie Mae and Freddie Mac wikipedia , lookup

Payday loan wikipedia , lookup

Moral hazard wikipedia , lookup

United States housing bubble wikipedia , lookup

Financialization wikipedia , lookup

Securitization wikipedia , lookup

Fractional-reserve banking wikipedia , lookup

Interest rate ceiling wikipedia , lookup

Syndicated loan wikipedia , lookup

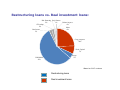

Bank Lending During the Financial Crisis of 2008 Victoria Ivashina David Scharfstein Harvard Business School Goal To understand the spill over of the crisis from financial sector to real sector through the lending channel – Did bank lending fall? – If so, was it a contraction in demand or supply? • How did different types of banks respond to the crisis? Prior: C&I Loans by Domestically Chartered Commercial Banks Source: Federal Reserve Board, Assets and Liabilities of Commercial Banks in the United States, (http://www.federalreserve.gov/releases/h8). Not seasonally adjusted, adjusted for mergers. Data • Reuters DealScan: Origination of large loans (primarily syndicated loans) Self reported data: -advertise -reflect market conditions -most importantly, receive league tables credit (published quarterly) • Data through December 31, 2008 • US companies • Primarily US banks but also includes domestic affiliates of foreign banks • From Aug ’08 to Oct ’08, top three US banks Citi, JPM, BAC originated 62% of the loans to the US companies, followed by Morgan Stanley with 4% of the loan origination Basic Facts: Bank Lending Falls Total Loan Issuance, US Corporate Loans (Amount and Number of Loans) • • New lending in 2008 was significantly below new lending in 2007, even before the peak period of the financial crisis The decline in new loans accelerated during the financial crisis, falling by 47% in dollar volume and 33% in number of issues in 4th quarter of 2008 relative to the previous quarter (79% and 61% with respect to the peak) QI '00 QII '00 QIII '00 QIV '00 QI '01 QII '01 QIII '01 QIV '01 QI '02 QII '02 QIII '02 QIV '02 QI '03 QII '03 QIII '03 QIV '03 QI '04 QII '04 QIII '04 QIV '04 QI '05 QII '05 QIII '05 QIV '05 QI '06 QII '06 QIII '06 QIV '06 QI '07 QII '07 QIII '07 QIV '07 QI '08 QII '08 QIII '08 QIV '08 Basic Facts: Bank Lending Falls Total Loan Issuance, US Corporate Loans (Billion USD) 800 700 600 500 400 300 200 100 0 Æ Look at the loan issuance across three categories: • Restructuring loans (M&A, LBOs, and stock repurchases) vs. Real investment loans (working capital or general corporate purposes) • Non-investment grade vs. investment grade loans • Term loans vs. revolving lines Restructuring loans vs. Real investment loans: Exit financing Proj. finance 2% 1% CP backup 2% Real estate 3% Debtor-in-poss. 0% Other 0% Corp. purposes 24% Work. Capital 7% Recap. 5% LBO/M&A 56% *Based on 2007 numbers Restructuring loans Real investment loans Restructuring loans vs. Real investment loans: 450 400 350 300 250 200 150 100 50 0 QI '07 QII '07 QIII '07 QIV '07 Restructuring Loans • QI '08 QII '08 QIII '08 QIV '08 Real Investment Loans There is a drop in both real investment loans (working capital or general corporate purposes) and restructuring loans (those for M&A, LBOs, and stock repurchases) Non-investment grade vs. investment grade loans: 400 350 300 250 200 150 100 50 0 QI '07 QII '07 QIII '07 QIV '07 Non-Investment Grade • QI '08 QII '08 QIII '08 QIV '08 Investment Grade In the last quarter of 2008, non-investment grade loans fell by 82% relative to the prior quarter, while investment grade loans fell by 77% Term loans vs. revolving lines: 400 350 300 250 200 150 100 50 0 QI '07 QII '07 QIII '07 QIV '07 Term Loans • QI '08 QII '08 QIII '08 QIV '08 Revolving Lines Sep–Nov 2008, revolving credit facilities and term loans both declined, but the decline in term loans (67%) was larger than the decline in revolving facilities (27%) Is drop in lending a supply shock or demand shock? Supply effect if bank characteristics affect lending • Effect of deposit base on lending – – Banks that are more reliant on short-term debt have difficulty rolling over debt and will have to cut lending more Thus, banks with strong deposit base will cut lending less Caveat: insured deposits C&I Loans by Domestically Chartered Commercial Banks Source: Federal Reserve Board, Assets and Liabilities of Commercial Banks in the United States, (http://www.federalreserve.gov/releases/h8). Not seasonally adjusted, adjusted for mergers. Reconciling the facts: • Borrowers draw down their credit facilities: OutstandingLoanst = OutstandingLoanst-1 + NewLoanst + Drawdownst – LoanRetirementst Borrowers draw down their credit facilities 34 firms, nearly $27 billion just in this sample (i.e., 26% of the jump) Borrowers draw down their credit facilities for precautionary reasons “ Drawing down these funds is a prudent liquidity measure. Ensuring access to our liquidity to the fullest extent possible at a time of ambiguity in the capital markets is in the best interest of our customers, suppliers, shareholders, and employees.” Dana Corp. explaining $200 mm drawdown. “ In light of the uncertain market environment, we have made this proactive financial decision to increase our liquidity and cash position and to bridge our access to the debt capital markets.” Duke Energy explaining $1 bn drawdown. “ The Company believes that these actions were necessary to preserve its availability to capital due to Lehman Brothers’ level of participation in the Company’s debt facilities and the uncertainty surrounding both that firm and the financial markets in general.” FairPoint Communications explaining $200 mm drawdown. Source: SEC filings Is drop in lending a supply shock or demand shock? Supply effect if bank characteristics affect lending • Effect of deposit base on lending – – Banks that are more reliant on short-term debt have difficulty rolling over debt and will have to cut lending more Thus, banks with strong deposit base will cut lending less Caveat: insured deposits • Effect of revolving line exposure on lending – Banks with large exposure to revolving lines will cut new lending more But, note that banks with large exposure to revolving lines also tend to have a strong deposit base (Kashyap, Rajan, and Stein, 2002) Revolvers and Deposits 1 Revolvers/Total Loans 0.8 0.6 y = 0.34+ 0.45x R² = 0.47 0.4 0.2 0 0 0.1 0.2 0.3 0.4 0.5 0.6 Deposits/Assets 0.7 0.8 0.9 1 Lehman exposure Example: Tribune Co. 750 $MM revolving line Tribune needs/draws 300 $MM JPM 150 $MM Lehman 150 $MM (375 $MM) (375 $MM) With Lehman out of the picture: JPM (375 $MM) Tribune needs/draws 300 $MM Lehman 300 $MM Empirical Approach Define three windows: Pre-Crisis: August 2006 – July 2007 Crisis I: August 2007 – July 2008 Crisis II: August 2008 –December 2008 Dependent variable: %Δ Total number of loans = [Mean(#loans per month)Crisis II / Mean(#loans per month)Base – 1] where base = Pre-Crisis or Crisis I (Median is -55% relative to Pre-crisis, and -39% relative to Crisis I) %Δ Total volume of loans per month (defined analogously) Regression: %Δ Total number of loans on lagged Deposits/Assets Results Results Economic magnitude: banks with revolving line exposure to Lehman one standard deviation above the mean (12%) cut lending by 44%, while banks with Lehman exposure one standard deviation below the mean (0%) cut lending by only 25% Robustness: Revolving lines vs. term loans Results Robustness: CDS Implications • Measurement issues • Financial crisis had an adverse effect on supply of credit at the bank level • However, it is possible that there was a drop in loan demand, which was satisfied by the banking sector as a whole though a shift in supply from low deposit banks to high deposit banks – Raises an important question: Can firms easily switch from one bank to another? If not, there will be real effects of the financial crisis even if there has been a drop in demand