Survey

* Your assessment is very important for improving the workof artificial intelligence, which forms the content of this project

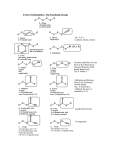

Jeffrey H. Nilsen Bonds A firm needs to borrow – why would it prefer to take a bank loan over issuing a bond (or vice versa) ? Do banks issue bonds ? Why ? We won’t use bond pricing in this class but we need to have intuition for how financial instruments’ values change when interest rates change Questions What is the fundamental value of house (as asset) ? What is a bond’s yield to maturity (YTM) ? How does YTM differ from holding period yield ? Given a bond P, coupon and face value, what does the YTM do? What is the YTM on a discount bond ? For a $100 face value with P of 95$ ? Valuing An Asset The fundamental value of an asset today is the present value of its future cash flows Your mortgage loan is asset to lender with PV(expected future interest & principle payments you make) Your house is an asset to you with value = PV(consumption services + expected sales price) Yield to Maturity Can measure YTM for all bonds, including zero coupon bonds For bond with a given P, Coupon and Face Value, YTM is the rate equating bond’s value today (its P) with PV(cash flows until maturity) if hold bond to maturity, then indeed YTM = return If sell prior to maturity, then (holding) return either greater or smaller than YTM (changing interest rates affect value of bond) Coupon Bond Questions What is the YTM on a coupon bond ? If the coupon rate = discount rate, what is Price of Bond ? If you sell a bond prior to maturity, under what conditions will you receive the YTM? Coupon Bonds (e.g. Treasuries, Corporate Bonds) Coupon bond (annuity): pays regular fixed coupons and repays F (face value) at maturity Coupon rate = C/F P0 C C F2 2 1 i 1 i 1 i 2 YTM equates P0 to PV(C) + PV(F) Fact: bond with coupon rate = discount rate has P0 = F E.g. 10%, 2-period bond with F = 1000, C = 100 & P0 = 1000 Bond Facts Coupon payments are fixed when you buy the bond While you hold the bond, market interest rates change (changing the discount rate) and the value of the bond If you sell the bond before it matures, you may NOT earn the “yield to maturity” Your “holding period return” is the return you receive for the time you have held bond Coupon Bond Sold prior to maturity questions You sell a 2 year, 10% $1000 face value bond after receiving the 1st coupon, with 1 year remaining to maturity. Interest rates have risen to 20%, what is the P you sell it for? Interest Rate vs. Holding (or Actual) Return Assume you must sell a 2-year bond you bought last year (year 0). It has 1 year remaining until maturity Holding Return = capital gain + CF earned holding bond = (P sold – P bought) + (bond coupon) rHold P1 P0 C P0 Earned 1 coupon, another remains But what is Pt+1 (the price you sell it at) ?? Holding Return Example (assume mkt rates rise to 20% in year 1) You buy 2Youryr bond 100at P0 100 = 1000 1000, C = 100 & F = 1000, so YTM 10% Bond At yr 0 0 1 2 Sell in YR 1: Your 1 year bond has only one $100 coupon left Your bond must compete with new 1 year bonds paying 20% coupon. P1NEW 200 1000 $1000 1.2 1.2 To find your bond’s P1, discount remaining CF at new market rate P1YOUR 100 1000 $916 1.2 1.2 The buyer pays lower P1 vs. new bond. Your bond will give her same return as new bond’s Holding Return Example If rates rise after you’ve bought a bond you’ll take a capital loss. ret P1 P0 C 916 1000 100 1.7% P0 Your holding return is less than the YTM 1000 Term Structure of Interest Rates (TS) Relation between interest rates of bonds differing only by term to maturity Bonds identical in default risk, liquidity, and tax payments FT term structure TODAY http://video.ft.com/4734867703001/US-recession-risk/editorschoice Why Is Term Structure (TS) Interesting? It’s crystal ball: rise in slope of TS predicts higher economic activity 4 quarters in future But how ? From C. Harvey (1995) Expectations Theory Explains how TS predicts future economic activity “pure” ET assumes short term and long term bonds are perfect substitutes (i.e. saver chooses short or long bond based only on return offered) Expectations Theory Interest rate on long bond equals avg. expected short rate over life of long bond Saver with $1 has 2-year horizon, selects between: Rollover short: Buy 1 yr bond, rollover at estimated t+1 1 year bond interest rate e e t t+1 it iet+1 Long: Buy 2-yr bond: t t+1 1 it 1 it 1 1 it it 1 it ite1 1 i 1 i 1 2 i 2 t 2 t 2 t it2 it2 i2t Saver will switch to whichever bond offers higher return => yields will be equal it ite1 2 it 2 ET => today’s long rate fixed by expected future short rates Assume current 1-yr bond rate 6% Assume saver expects next year’s 1-yr bond rate to be 8% So 2-yr bond rate must be it2 it ite1 2 (6% + 8%)/2 = 7% per annum in order for saver to buy it BUT: future short term rates can’t Be observed on today’s market !! Use ET to Infer Future Short Term Rates i2, 0 i0 E0 i1 2 For 2 periods, today is time 0 E0 i1 not observable If observe i2,0 > i0 pure ET predicts E0 i1 > i0 => market expects short rate to rise in future But TS usually up-sloping (how can it be ?? How can rates usually be expected to rise ??) Segmented Markets Theory Theory assumes short & long term instruments are not substitutes at all => separate markets so short and long rates set independently Can explain consistently higher LT rates But can’t explain why all rates move together Preferred Habitat (Liquidity Premium) Theory Savers lend long only if receive term premium => TS normally up-sloping 10 10, 0 i i0 E0 i1 ... E0 i10 10,0 10 (10 year bond) where θ is premium savers are paid for lending long If LT < ST rates => inverted TS indicates steep fall in expected short-term rates swamping θ But θ fluctuates over time; Shiller (1990): “...little agreement on how term premium is affected by M policy!" How ET predicts Future GDP (via M Policy): (assume TS initially up-sloping) Fed tightens M policy: current short rates rise. Y falls in short run M policy neutral in long run => future short rates unaffected ET => short rate rise > long rate rise (TS becomes more flat) Summarizing: contracting M (iLong – iShort) falls (slope falls) GDP slows => TS & GDP positively related maturity