Survey

* Your assessment is very important for improving the workof artificial intelligence, which forms the content of this project

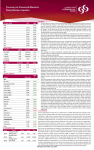

Qatar Financial Centre Authority PO Box 23245 Doha, Qatar T +974 496 7777 F +974 496 7676 [email protected] www.qfc.com.qa Banking V1 / 500 / 11.2008 Qatar lies at the heart of the Gulf, and is playing an increasingly influential role on both the regional and world stages. It has one of the highest per capita incomes in the world and is the most rapidly developing economy in the Middle East 03 06 10 14 Introducing Qatar The economy The Banking opportunity Qatar Financial Centre Qatar’s government is using its vast oil and gas wealth to create a society that provides opportunities for all 02 03 Introducing Qatar Qatar is emerging as one of the most dynamic economies in the Middle East, with a clear vision for its future and the means and determination to achieve it. It offers both significant business and investment opportunities to new players in the financial sector. Under the leadership of Qatar’s Emir, Sheikh Hamad bin Khalifa Al Thani, the country has taken steps towards the creation of a modern, knowledge-based economy in order to establish a stable and sustainable future. The government is using its vast oil and gas wealth to create a society that provides opportunities for all. Reliance on crude oil exports has been replaced by an ambitious and progressive approach to the management of the nation’s economy, which focuses on developing Qatar’s huge natural gas reserves and its expansion of liquefied natural gas, petrochemicals and condensates production. This is supported by a far reaching programme of economic liberalisation and diversification into a more broadly based economy. Investment in education is a central focus of Qatar’s development goals. To support its vision of a modern, industrialised and knowledge-based economy the government has recognised that education is key to business success and long-term prosperity and has funded social development and technological projects at all levels. One such project is The Qatar Foundation for Education, Science and Community Development, which was set up in 1995 to provide world class educational opportunities, to support Qatar’s diversification programme and to attract world class research and development to Qatar. The most visible elements of this investment are Education City, which comprises a 2,500 acre campus hosting six world-renowned US universities, and the Qatar Science and Technology Park (QSTP), which supports the country’s desire to attract technology transfer and value added research. By bringing research and business together, QSTP is also spearheading the development of Qatar’s knowledge-based economy. 04 05 “Qatar is on the rise… US$140 billion investment is turning this small country into a leading center in the Middle East” Forbes Qatar’s economy is rapidly expanding in practically every sector and industry. A combination of government investment and the participation of multi-national companies is creating a culture of opportunity. The government has committed over US$140 billion for investment, infrastructure and expansion in a wide range of sectors, including energy, health, education, transport, infrastructure and tourism. Qatar enjoys one of the world’s fastest growing GDPs, reaching 11.8% year on year, with a nominal value of US$92 billion in 2008 (Economist Intelligence Unit), making Qatar one of the wealthiest nations in the world. Finance The finance sector in Qatar is growing both within and outside the QFC and is attracting international investment. The Doha Securities Market (DSM) was opened to investors in May 1997 and in June 2008 had 43 companies listed on its exchange with new listings occurring on a regular basis. In June 2008 it was announced that NYSE Euronext would be taking a 25% shareholding in the DSM and would play a significant role in the future development and management of the exchange. Major international finance companies have already established a presence in Qatar, including HSBC, Standard Chartered Bank, Zurich, AXA, Barclays, EFG Hermes, Credit Suisse, ICBC, ICICI, Citi and Morgan Stanley. The economy is characterised by low private consumption and a high national savings rate, making Qatar a very attractive financial market within the GCC and with a high asset growth rate. In its June 2008 report on the MENA Banking Sector, EFG Hermes identified Qatar as the banking destination of choice in the region thanks to its strong momentum in investments and strong economic growth. The QFC also sees a strong potential for Qatar to become the regional hub for insurance and reinsurance. 06 Energy Qatar is quickly becoming the world’s single largest producer of LNG, and by 2010 will have a production capacity of 77 million tons per year. Qatar’s LNG industry is expanding fast, while new oil capacity continues to come on stream, thus boosting export volumes. Output of associated condensates — light oil extracted during gas production — is also growing and other gas-based industrial projects, such as the Oryx Gas to Liquid facility, are reaching completion. Qatar’s role as a major supplier of energy to the world has been recognised with the decision for Doha to host the 24th World Petroleum Congress in 2010. Transport The transport sector is key in supporting the rapid growth of Qatar, and with significant investment in fleet and infrastructure projects, Qatar is establishing itself as a hub for global travel. Its flagship airline, Qatar Airways, now flies to over 80 destinations, and has ambitious plans to treble its fleet of airliners by 2015. The New Doha International Airport, which is currently under construction, will offer an initial capacity of 12 million passengers per year in 2010 and the ability to handle 50 million passengers per year upon its completion in 2015, making it the largest airport in the Middle East. The scale of Qatar’s oil and gas industry, and the associated opportunities it provides, are truly remarkable. The latter half of 2008 will see Qatar take delivery of the world’s largest LNG carrier. The 265,000 cubic metres vessel is currently being built by a Korean shipyard and, with a total of 58 new LNG tankers under construction in Korea, Qatar is the biggest client for Korean shipbuilders. To supply gas to its global customer base, Qatar will expand its fleet of 20 vessels by another 60, at a cost of some US$15 billion, by 2009. A massive public works renewal programme is now in full swing with projects ranging from new and improved roads to power supplies and enhancements to other utilities, with projects ranging from the US$1.8 billion ‘Friendship Bridge’ between Qatar and Bahrain and the regeneration and development of the Ras Laffan port now underway. The government is continuing to invest billions of dollars as part of its commitment to the transport sector with plans to build a 140km light rail system, to add a number of multi-lane motorways, to extend current road networks and to expand and improve the bus and taxi system. Infrastructure To meet the expected demand from business travellers, more than 80,000 hotel rooms will be available in Qatar by 2016, with several multi-national hotel corporations already in the final stages of building properties in the capital including Hilton, Rotana Hotels, Shangri-La Hotels and Resorts, W Hotels and the Global Hyatt Corporation. Long-term residents are also being served with several ambitious residential projects underway including The Pearl Qatar. The Pearl is a US$2.5 billion man made island covering 985 acres of reclaimed land offshore. Once opened, it will be the first real estate venture in Qatar to offer international investors freehold and residential rights to 7,600 units of high quality accommodation of varying styles. Lusail is a mixed use development which will house Energy City and will accommodate some 200,000 residents. Demand for electricity and water in these major developments will be met thanks to planned new power plants, with a projected doubling of the country’s water and electricity distribution capacity by the end of 2009. Healthcare and science Qatar is building capacity across the healthcare and research sectors. It has set aside US$8 billion — the largest cash endowment of its kind anywhere in the world — to create the Sidra Medical and Research Centre. At its heart will be a US$900 million fully digitalised academic medical centre that will help to build Qatar’s scientific expertise and resources. It is scheduled to open in 2011. A further 2.8% of Qatar’s GDP has been committed to fund biomedical research. The Qatar Science and Technology Park has been set up to encourage research and innovation in science. The Park, which officially opens in 2009, already boasts tenants such as Shell, Microsoft, Cisco, EADS, Rolls Royce, Total and GE, with research underway into upstream environments, carbonate reservoirs and solar energy. 07 The economy This nation, with an indigenous population of some 250,000 is transforming itself into one of the fastest growing economies in the world The increasing demand for banking services has created a market with immense potential for experienced players 08 09 The Banking opportunity 10 11 Qatar’s burgeoning economy and the scale of new projects coming onstream offer a compelling case for banks. The lion’s share of investment in the GCC region is expected to be in the construction sector, with a likely value of US$663 billion between 2008 and 2011 There is therefore considerable wealth being generated in the market, and a growing appetite for investment and innovative financial products, both at the personal and the business level. While the A programme of investment across the gross savings rate in the GCC is one of the entire economy, supported by Qatar’s highest in the world, the ratio of private increasing energy revenues, has created consumption to GDP is significantly lower new avenues for a wide range of banking than the global average. According to the services including commercial and investment banking, project finance, Islamic EIU, Qatar records one of the highest savings rates in the GCC, with 61%, and the finance, as well as asset management, private banking and wealth management. lowest private spending rate of 22% in the The increasing demand for banking services region. This clearly indicates an opportunity for additional investment and retail has created a market with immense banking products. potential for companies able to provide new capacity to the financial sector. Wealthy individuals and government funds are increasingly looking outside The opportunities are not only in Qatar. The traditional markets to diversify their portfolios, GCC region as a whole is benefiting from with 80% of Middle East private wealth large hydrocarbon revenues, which have been channelled into over US$2 trillion worth invested outside the region in 2006 (Cap Gemini World Wealth Report). While this of infrastructural and other major projects. represents a significant opportunity for Qatar has consistently enjoyed the fastest banks from outside the region, in support growth in the region, and this is projected of the domestic banks in the region, it also to continue with GPD in Qatar forecast to represents the potential for investment increase at 10.5% in the period 2006-2010 vehicles to be established inside the region. (source: EIU). Real Economic growth in Qatar is expected to continue, estimated to be 13.4% in 2009 from 2008, and 6.7% in 2011 from 2010 (source: EIU). Real economic growth in Qatar is expected to continue, averaging 14% annually from 2008-9 and 11.0% in 2010-11 (Standard & Poor’s). The lion’s share of investment in the GCC region is expected to be in the construction sector, with MEED Projects estimating its likely value at US$663 billion between 2008 and 2011. This is being invested across almost 1,000 construction and real-estate projects, with over 140 of them having estimated values of US$1 billion. The majority of these projects will take place in UAE, Saudi Arabia, and Qatar. Qatar is leading the way in oil and gas investment with around US$40 billion allocated to its LNG program to extract, store and transport gas from the vast North Field reservoir, and a further US$30 billion in other energy projects, while its neighbour Saudi Arabia is committing over US$80 billion into petrochemical and industries projects. According to the EIU, Qatar records one of the highest savings rates in the GCC, with 61%, and the lowest private spending rate of 22% in the region 12 13 The GCC is the world’s largest project finance market, with the Ras Abu Fontas/ Nakhilat deal in 2006 achieving tenors of more than 25 years for the first time for any project financing in the region. With continued development in the energy sector, and a surge in non-traditional industry projects, the prospects for further project finance in the region look strong. Estimates put the total project finance needs for the GCC region at US$ 420 billion in the period 2006-2009 (Zawya). This is being serviced by an increase in the number of international banks entering the GCC market, along with a focus on newer sources of funding such as Islamic tranches and bonds. Inevitably there has been a commensurate rise in project finance advisory opportunities across the region. Heightened investment activity has also led to an increase in corporate borrowing and long-tenor funds from debt capital markets, with GCC companies expected to look further towards the long-term international bond markets as an alternative source to meet their financing needs. In 2006 three of the largest GCC bond issues came from Qatar (Rasgas at US$1.55 billion, Nakilat at US$1.15 billion and Qatar Petroleum at US$650 million). Furthermore corporate borrowing is increasing and diversifying. The total corporate debt for the GCC region nearly doubled in 2006 to US$93 billion, with a 45% increase in the total number of loans, and growth in loans in newer sectors such as telecoms, real estate and shipping. Multinational banks were the main beneficiaries of this growth. GCC Sukuks are becoming increasingly popular among international investors resulting in high levels of oversubscription. The appetite for Shari’a compliant finance as a means of diversifying investments is clear, and, as Islamic finance matures as an industry, the region is likely to see the emergence of a liquid secondary market for trading Sukuks. Islamic finance continues to grow in demand, popularity and diversity, and its expansion has been considerably faster than conventional banking within the GCC region in recent years (though from a much lower base). However, the regional Islamic banks are small by international standards and they are likely to have capacity constraints in catering to the large domestic financing needs. New Islamic banks are being formed and there is evidence of established regional banks adding Islamic finance to their portfolios. Sukuks (Islamic bonds) are increasingly attractive sources of funding with nearly US$2 billion believed to have been raised in the GCC region through Sukuk issues in 2007 (IFIS). Even taking into account recent equity market corrections, stock exchanges in the region are developing with an increase in M&A and IPO activity. In every GCC country M&A and Equity Capital Markets advisory is dominated by the foreign investment banks. Over US$20 billion is expected to be raised across 100 IPOs in the GCC over the next two years. Such transactions will undoubtedly become more efficient and sophisticated with the increased involvement of such leading exchanges as Nasdaq and NYSE Euronext. Given the wealth of the region, it comes as no surprise that there is great potential for private banking services. HNWIs are increasingly seeking innovative financial solutions that capitalise and diversify their current holdings. 80% of HMWIs in the region claim residences in non-GCC countries, with 45% having children living abroad. This group is characterised by an international mindset and desire for new products that compare with those available in more developed exchanges, as well as catering to local market needs and providing value-added services. Qatar and the QFC offer banks the opportunity to tap into this significant potential. The business environment created by the QFC enables banks to quickly establish a meaningful presence in Qatar and the region. With the ability to handle both onshore and offshore business, banks licensed by the QFC have the chance to directly engage with some of the most economically dynamic economies in the world today. Council of Ministers THE BOARD: Chairman Chief Executive Officer and Director General Non-Executive Director • Oversight & strategy • Business Development • Policy, plans procedures • Provide infrastructure/ HR/administration • Budgeting & reporting • Develop location • Corporate Communications and Marketing • Propose & submit regulation • Approve licensed companies and persons • Collect fees and taxes • Issue visas and permits Companies Registration Office Executive Team Business Development Promote the Qatar Financial Centre and shape offering to businesses • Help, advise and support businesses to make their commercial decisions Operations Provide facilities and infrastructure for the efficient operation of the Qatar Financial Centre • Support services to all other departments (HR, IT, finance etc) 14 Corporate Communications and Marketing Promote the reputation and profile of the QFC Authority through media relations, sponsorship and other activities • Provide information, communications and knowledge support to the QFC and its partners External Liaison Serve as link with government and locating companies, provide support to businesses • Macroeconomic monitoring • Visas, taxation, health and education etc Qatar Financial Centre Qatar Financial Centre (QFC) is a financial and business centre established to attract international financial services and multinational corporations in order to grow and develop the market for financial services in Qatar and the region. QFC provides access to over US$140 billion of investment in Qatar over the next 5 years as well as to over US$1 trillion planned investment across the GCC. QFC consists primarily of a commercial arm, the QFC Authority (QFC) and an independent financial regulator, the QFC Regulatory Authority. QFC operates to international and transparent laws based on standards found in the UK, the USA and other leading financial jurisdictions around the world. It also has an independent judiciary which comprises a civil and commercial court and a regulatory tribunal. A combination of revenue potential, low operating cost and low risk for financial services firms provide a compelling reason for establishing operations in Qatar. Many of the top global financial institutions are already enjoying the benefits that QFC has to offer. This number is growing at a rapid rate and is made up of both financial services firms, and those offering professional services to and in support of the financial sector including legal, insurance, accounting and consulting organisations. QFC provides access to local and regional investment opportunities, providing an abundance of expertise. Business can be transacted inside or outside Qatar, in local or foreign currency. Uniquely, this allows businesses to operate both locally and internationally. Furthermore, QFC allows 100% ownership by foreign companies, and all profits can be remitted outside of Qatar. QFC has a low, highly transparent, flat rate tax regime, applying 10% tax on profits generated by QFC licensed firms. Qatar Financial Centre (QFC) Authority The QFC Authority is responsible for commercial strategy and for developing relationships with the global financial community and other key institutions both within and outside Qatar. QFC Authority aims to help all QFC licensed firms generate new, and sustainable, revenue streams, and in doing so contribute to the further development and deepening of the financial services sector in Qatar. One of the most important roles of QFC Authority is to approve and issue licences to individuals, businesses and other entities that wish to incorporate or establish themselves in Qatar with the Centre. In practical terms, QFC helps licensees concentrate on their core business by offering fast and efficient on-call support and commercial counsel. It provides a direct link with government institutions in Qatar and a wide reaching international political and business network. The QFC Authority provides licensees with a principal point of contact via its Operations Department for infrastructure, office space and IT, as well as communications support for its licensee community. Licensed firms are able to choose their own location provided that it has been confirmed as an approved site. Qatar Financial Centre (QFC) Regulatory Authority The QFC Regulatory Authority is an independent statutory body and authorises and supervises businesses that conduct financial services activities in, or from, the QFC. It has developed principle-based legislation of international standard, modelled closely on those standards employed by London and other major financial centres. The QFC Regulatory Authority has powers to authorise, supervise and, where necessary, discipline regulated firms and individuals. In 2007 the government announced a decision to create a single unified financial regulatory platform in which the QFC Regulatory Authority, the banking supervisory arms of the Central Bank and of the Qatar Financial Markets Authority, which oversees the Doha Securities Market, would be combined into one body, and the laws and rulebooks of the country’s financial sector would be revised and rewritten to meet international standards. This move will set Qatar apart from its regional neighbours and will provide a high level of regulation and efficiency for all participants in Qatar’s financial sector. The Independent Judiciary The Centre also comprises a Civil and Commercial Court and a Regulatory Tribunal. The judiciary exists to uphold the rule of law and ensure the transparency of QFC business transactions. These two bodies provide the legal infrastructure for the QFC to resolve disputes between QFC firms or financial institutions and their counter-parties, and for arbitration or the formal resolution of civil disputes. The Court is modelled on the internationally respected Commercial Court in London. It is responsible for hearing and delivering judgements on cases that come before it, and is the final arbiter in the event of disputes in matters of law. The Regulatory Tribunal has been established to hear and decide upon appeals from decisions of the QFC Regulatory Authority and other QFC agencies. 15 “We believe that we have helped raise the standards of regulation and market development in the region, established a place for Qatar among the elite of the global financial services industry and improved the quantity and quality of financial services provided to our citizens” HE Yousef Hussein Kamal, Chairman, QFC Authority Printed on Revive 50:50 Gloss, which is produced using 50% de-inked post-consumer recovered fibre at a mill that has been awarded the ISO14001 certificate for environmental management. The pulp is bleached using an elemental chlorine free (ECF) process. Designed by Bisqit. www.bisqit.co.uk