Survey

* Your assessment is very important for improving the work of artificial intelligence, which forms the content of this project

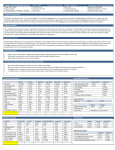

Module 4.3 Stock Valuation – estimating growth and discount rates, plus a look at comparables McGraw-Hill/Irwin Copyright © 2013 by The McGraw-Hill Companies, Inc. All rights reserved. 9.2 Estimates of Parameters The value of a firm depends upon its growth rate, g, and its discount rate, R. Where does g come from? g = Retention ratio × ROE (eq 9.8) Payout Ratio = dividend per share / earnings per share Retention Ratio = 1 – dividend payout ratio 9-1 Digging into ROE Please read this wikipedia link: https://en.wikipedia.org/wiki/Return_on_equity ROE is typically described as the product of three other ratios: net margin, asset turnover, and leverage. Net margin and asset turnover are typically deemed decent measures of managerial skill. æ NetIncome öæ Sales öæ Assets ö NetIncome ROE = ç ÷ç ÷ç ÷= è Sales øè Assets øè Equity ø Equity So, not ROEs are created equally. Warren Buffet likes firms that improve ROE by improving net margin and asset turnover (the first two ratios). 9-2 Where Does R Come From? Asset pricing models like the CAPM (coming soon) or from our dividend growth model The discount rate can be broken into two parts. The dividend yield The growth rate (in dividends) In practice, there is a great deal of estimation error involved in estimating R AND g. If g is estimated from ROE, and ROE is based on accounting numbers, then you know there is a lot room for error! 9-3 Using dividend growth model (DGM) to Find R Start with the DGM: D0 (1+ g) D1 P0 = = R-g R-g Rearrange and solve for R, shows R as sum of dividend yield and growth rate : D0 (1+ g) D1 R = +g = +g P0 P0 Dividend yield growth rate 9-4 9.3 Growth Opportunities Growth opportunities are opportunities to invest in positive NPV projects. The value of a firm can be conceptualized as the sum of the value of a firm that pays out 100% of its earnings as dividends plus the net present value of the growth opportunities. EPS P= + NPVGO R 9-5 NPVGO Model: Example Consider a firm that has forecasted EPS of $5, a discount rate of 16%, and is currently priced at $75 per share. We can calculate the value of the firm as a cash cow. EPS $5 P0 = = = $31.25 R .16 So, NPVGO must be: $75 - $31.25 = $43.75 9-6 9.4 Comparables Comparables are used to value companies based primarily on multiples. Common multiples include: Price-to-Earnings Enterprise Value Ratios 9-7 Price-Earnings Ratio The price-earnings ratio is calculated as the current stock price divided by annual EPS. The Wall Street Journal uses last 4 quarter’s earnings Price per share P/E ratio = EPS 9-8 PE and NPVGO EPS P= + NPVGO R Recall, Dividing every term by EPS provides the following description of the PE ratio: 1 NPVGO PE = + R EPS So, a firm’s PE ratio is positively related to growth opportunities and negatively related to risk (R) 9-9 Enterprise Value Ratios The PE ratio focuses on equity, but what if we want the value of the firm? Use Enterprise Value: Like PE, we compare the value to a measure of earnings. From a firm level, this is EBITDA, or earnings before interest, taxes, depreciation, and amortization. EV = market value of equity + market value of debt - cash EBITDA represents a measure of total firm cash flow The Enterprise Value Ratio = EV / EBITDA 9-10 Common Stock Market Reporting 52 WEEKS YLD VOL NET HI LO STOCK SYM DIV % PE 100s CLOSE CHG 21.89 9.41 Gap Inc GPS 0.34 3.1 8 88298 11.06 0.45 Gap has been as high as $21.89 in the last year. Gap pays a dividend of 34 cents/share. Gap ended trading at $11.06, which is up 45 cents from yesterday. Given the current price, the dividend yield is 3.1%. Gap has been as low as $9.41 in the last year. Given the current price, the PE ratio is 8 times earnings. 8,829,800 shares traded hands in the last day’s trading. 9-11