Survey

* Your assessment is very important for improving the work of artificial intelligence, which forms the content of this project

Business valuation wikipedia , lookup

Stock selection criterion wikipedia , lookup

Conditional budgeting wikipedia , lookup

Present value wikipedia , lookup

Individual Savings Account wikipedia , lookup

Securitization wikipedia , lookup

Internal rate of return wikipedia , lookup

Public finance wikipedia , lookup

Modified Dietz method wikipedia , lookup

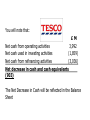

The Cash Flow Statement by Binam Ghimire 1 Learning Objective 1. 2. 3. 4. 5. Cash Flow from Operations Cash Flow from Investing Cash Flow from Financing IAS7 Presentation of the Cash Flow Statement Analysis of Cash Flow Cash Flow Statement IAS 7 Fundamental Principle in IAS 7 All enterprises that prepare financial statements in conformity with IFRSs are required to present a statement of cash flows. Objective of IAS 7 to require the presentation of information about the historical changes in cash and cash equivalents of an enterprise by means of a statement of cash flows, which classifies cash flows during the period according to operating, investing, and financing activities. What are cash and cash equivalents ? Cash & Cash Equivalents cash on hand demand deposits short-term, highly liquid investments that are readily convertible to a known amount of cash, and that are subject to an insignificant risk of changes in value. Guidance notes indicate that an investment normally meets the definition of a cash equivalent when it has: a maturity of three months or less from the date of acquisition. overdrawn bank balances where these readily fluctuate from positive to negative Presentation of the Statement of Cash Flows Cash flows must be analysed between Operating, Investing Financing Activities. Operating activities Are the main revenue-producing activities of the enterprise that are not investing or financing activities, So operating cash flows include cash received from customers and cash paid to suppliers and employees Investing activities Are the acquisition and disposal of long-term assets and other investments that are not considered to be cash equivalents Financing activities Are activities that alter the equity capital and borrowing structure of the enterprise Note: Interest and Dividends received and paid may be classified as operating, investing, or financing cash flows, provided that they are classified consistently from period to period Taxation Cash Flows Cash flows arising from taxes on income are normally classified as operating, unless they can be specifically identified with financing or investing activities Extraordinary Items Should be classified as operating, investing or financing as appropriate and should be separately disclosed Cash Flows and Life Cycle 10 Summary so far…. A Cash Flow Statement is: a statement of the cash that flowed into and out of the business over the last year. To aid understanding it is normally presented under 3 headings: Net Cashflow (in – out) from Operating Activities (i.e. from your core trading activity – clearly this should produce a positive cash inflow) Net Cashflow from Investing Activities (e.g. buying/selling Non Current Assets. Growing companies will therefore have a negative cashflow). Net Cashflow from Financing (e.g. cash received/repaid re share issues and debt – as a result it may well be negative) The addition of these 3 will then balance to the Increase/Decrease in the Bank/Cash balances over the year Cisco Systems You will note that: Net cash from operating activities Net cash used in investing activities Net cash from refinancing activities Net increase in cash and cash equivalents 527 $ 9,897 (9,959) 589 The Net Decrease in Cash will be reflected in the Balance Sheet You will note that: £M Net cash from operating activities 3,992 Net cash used in investing activities (1,859) Net cash from refinancing activities (3,036) Net decrease in cash and cash equivalents (903) The Net Decrease in Cash will be reflected in the Balance Sheet The Relationship between the Balance Sheet and the Cash Flow Statement The relationship between the Balance Sheet and the Cash Flow Statement, usually reveals: the Investment Cycle representing the purchase of Non Current Assets the Operating Cashflow, financing Working Capital (purchase of Current Assets and payment of Current Liabilities) Cashflow from Financing (Equity and/or Debt) to finance the investment in Non Current Assets BALANCE SHEET Cash Flow Investment Cycle (i.e. cash used to buy assets or received from the sale of assets) ASSETS Non Current Assets LIABILITIES Equity Non Current Liabilities (Debt) Operating Cycle (i.e. from core trading activities) Current Assets Current Liabilities Cash Flow From Financing (i.e. cash from shares issued and loans taken) Evaluation What does the Cash Flow Statement of Tesco tell you about them, after all the Net Decrease in cash and cash equivalents is £ 903 M for the year ? Summary Fundamental Principle in IAS 7 All enterprises that prepare financial statements in conformity with IFRSs are required to present a statement of cash flows. Objective of IAS 7 to require the presentation of information about the historical changes in cash and cash equivalents of an enterprise by means of a statement of cash flows, which classifies cash flows during the period according to operating, investing, and financing activities. Cash flows must be analysed between Operating, Investing Financing Activities.