27_3420_KevinSte..._1_unsigned_copy

... operating capability, which represents an entity’s ability, at any given time, to carry out its activities at the scale determined by its then-existing resources, both monetary and non-monetary. Using an operating capability concept of wealth, the entity’s recognised economic resources and present o ...

... operating capability, which represents an entity’s ability, at any given time, to carry out its activities at the scale determined by its then-existing resources, both monetary and non-monetary. Using an operating capability concept of wealth, the entity’s recognised economic resources and present o ...

Basic Cost Management Concepts

... costs are actively managed. At the most basic level, a cost may be defined as the sacrifice made, usually measured by the resources given up, to achieve a particular purpose. If we look more carefully, though, we find that the word cost can have different meanings depending on the context in which i ...

... costs are actively managed. At the most basic level, a cost may be defined as the sacrifice made, usually measured by the resources given up, to achieve a particular purpose. If we look more carefully, though, we find that the word cost can have different meanings depending on the context in which i ...

chapter 10—statement of cash flows

... 4. operating cash flow/current maturities of long-term debt and current notes payable 5. operating cash flow/total debt 6. operating cash flow per share b. 1. Review the statement of cash flows and comment on significant items. 2. Comment on cash dividends in relation to net income and net cash prov ...

... 4. operating cash flow/current maturities of long-term debt and current notes payable 5. operating cash flow/total debt 6. operating cash flow per share b. 1. Review the statement of cash flows and comment on significant items. 2. Comment on cash dividends in relation to net income and net cash prov ...

Chp 4 Slides 04_Ch_4_Slides

... Adjusting Entries for “Unearned Revenues” Illustration: Sierra Corporation received $1,200 on October 2 from R. Knox for guide services for multi-day trips expected to be completed by December 31. Unearned Service Revenue shows a balance of $1,200 in the October 31 trial balance. From an evaluation ...

... Adjusting Entries for “Unearned Revenues” Illustration: Sierra Corporation received $1,200 on October 2 from R. Knox for guide services for multi-day trips expected to be completed by December 31. Unearned Service Revenue shows a balance of $1,200 in the October 31 trial balance. From an evaluation ...

Accounting for Receivables

... Some receivables will never be collected and must be written off as uncollectible. ...

... Some receivables will never be collected and must be written off as uncollectible. ...

(PPT, 269KB)

... were financially stable, but Exxon was in a better situation than Mobil. The Exxon’s current and quick ratios (0.57 and 0.91 correspondingly) were higher than the Mobil’s (0.48 and 0.67 correspondingly) and merged company had significantly improved these results. Ratio of net current assets as a per ...

... were financially stable, but Exxon was in a better situation than Mobil. The Exxon’s current and quick ratios (0.57 and 0.91 correspondingly) were higher than the Mobil’s (0.48 and 0.67 correspondingly) and merged company had significantly improved these results. Ratio of net current assets as a per ...

RTF - Review of Business Taxation

... When an asset owned by the entity before the change in ownership (‘pre-entry asset’) is subsequently disposed of for a capital loss after a relevant change in ownership, the loss realised by the entity would be apportioned between, and allocated to, the pre- and post-ownership change period. This co ...

... When an asset owned by the entity before the change in ownership (‘pre-entry asset’) is subsequently disposed of for a capital loss after a relevant change in ownership, the loss realised by the entity would be apportioned between, and allocated to, the pre- and post-ownership change period. This co ...

Financial Accounting and Accounting Standards - FMT-HANU

... The Basics of Adjusting Entries Illustration: Pioneer Advertising Agency purchased supplies costing $2,500 on October 5. Pioneer recorded the payment by increasing (debiting) the asset Supplies. This account shows a balance of $2,500 in the October 31 trial balance. An inventory count at the close ...

... The Basics of Adjusting Entries Illustration: Pioneer Advertising Agency purchased supplies costing $2,500 on October 5. Pioneer recorded the payment by increasing (debiting) the asset Supplies. This account shows a balance of $2,500 in the October 31 trial balance. An inventory count at the close ...

Cash inflows - NYU Stern School of Business

... • The statement of cash flows, along with the income statement, explains why balance sheet items have changed during the period. – The balance sheet shows the status of a company at a point in time. – The statement of cash flows and the income statement show the performance of a company over a perio ...

... • The statement of cash flows, along with the income statement, explains why balance sheet items have changed during the period. – The balance sheet shows the status of a company at a point in time. – The statement of cash flows and the income statement show the performance of a company over a perio ...

CH 23 STATEMENT OF CASH FLOWS SELF

... the accumulated depreciation at date of sale was $1,400,000. The proceeds from the sale of the plant assets were $210,000. The information concerning the sale of the plant assets should be shown on Collier's statement of cash flows (indirect method) for the year ended December 31, 2012, as a (n) A. ...

... the accumulated depreciation at date of sale was $1,400,000. The proceeds from the sale of the plant assets were $210,000. The information concerning the sale of the plant assets should be shown on Collier's statement of cash flows (indirect method) for the year ended December 31, 2012, as a (n) A. ...

Balance Sheet

... IFRS requires a classified statement of financial position except in very limited situations. IFRS follows the same guidelines as this textbook for distinguishing between current and noncurrent assets and liabilities. However under GAAP, public companies must follow SEC regulations, which require sp ...

... IFRS requires a classified statement of financial position except in very limited situations. IFRS follows the same guidelines as this textbook for distinguishing between current and noncurrent assets and liabilities. However under GAAP, public companies must follow SEC regulations, which require sp ...

Ind AS 106 – Exploration for and Evaluation of Mineral Resources

... An entity shall disclose information that identifies and explains the amounts recognised in its financial statements arising from the exploration for and evaluation of mineral resources. ...

... An entity shall disclose information that identifies and explains the amounts recognised in its financial statements arising from the exploration for and evaluation of mineral resources. ...

Balance Sheet

... Usefulness of the Statement of Cash Flows Without cash, a company will not survive. Cash flow from Operations: High amount - company able to generate sufficient cash to pay its bills. Low amount - company may have to borrow or issue equity securities to pay bills. ...

... Usefulness of the Statement of Cash Flows Without cash, a company will not survive. Cash flow from Operations: High amount - company able to generate sufficient cash to pay its bills. Low amount - company may have to borrow or issue equity securities to pay bills. ...

Idle Capacity Costs: It Isn`t Just the Expense

... of the cost of idle capacity (i.e., no recognition). We compare this to our recommended treatment, where the cost of idle capacity is recognized as a separate line item in the income statement for financial reporting. Our goal is to demonstrate that the normal costs of idle capacity are quite large ...

... of the cost of idle capacity (i.e., no recognition). We compare this to our recommended treatment, where the cost of idle capacity is recognized as a separate line item in the income statement for financial reporting. Our goal is to demonstrate that the normal costs of idle capacity are quite large ...

Advanced Accountancy Paper - I

... harmonise the diverse accounting policies and practices, constituted an ASB on 1st April, 1977. This board has been formulating the Accounting Standards applicable to Indian enterprises. Initially, the Accounting Standards were recommendatory in nature and gradually the Accounting Standards were mad ...

... harmonise the diverse accounting policies and practices, constituted an ASB on 1st April, 1977. This board has been formulating the Accounting Standards applicable to Indian enterprises. Initially, the Accounting Standards were recommendatory in nature and gradually the Accounting Standards were mad ...

Financial statements of limited companies – profit and loss account

... In Chapter 2 we looked at how to prepare simple financial statements from transactions carried out by a business during an accounting period. We then looked in a little more detail at the first of these financial statements, namely the balance sheet. This chapter will be concerned with the second of ...

... In Chapter 2 we looked at how to prepare simple financial statements from transactions carried out by a business during an accounting period. We then looked in a little more detail at the first of these financial statements, namely the balance sheet. This chapter will be concerned with the second of ...

25.263

... The commission may initiate a generic proceeding to determine true-up issues that are common to multiple TDUs, APGCs, and AREPs. This proceeding may include updates to the ECOM model required by subsection (f)(2)(B) of this section, in the event a notification of intent is filed pursuant to paragrap ...

... The commission may initiate a generic proceeding to determine true-up issues that are common to multiple TDUs, APGCs, and AREPs. This proceeding may include updates to the ECOM model required by subsection (f)(2)(B) of this section, in the event a notification of intent is filed pursuant to paragrap ...

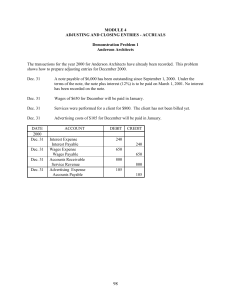

Practice Problem 2

... Billing of $25,000 has been issued for the month. Services of $5,000 to Construction Experts were completed on December 30, 2001, but billing will not be rendered until January 3, 2002. If Rental Services takes no action on any of the above items: a. Assets for 2001 will be overstated by $1,200. ...

... Billing of $25,000 has been issued for the month. Services of $5,000 to Construction Experts were completed on December 30, 2001, but billing will not be rendered until January 3, 2002. If Rental Services takes no action on any of the above items: a. Assets for 2001 will be overstated by $1,200. ...

chapter 3 the reporting entity and consolidation of less-than

... picture of the financial position and operating results of the overall operations under his or her control by preparing combined financial statements. Q3-20 Under the proprietary theory the parent company includes only a proportionate share of the assets and liabilities and income statement items of ...

... picture of the financial position and operating results of the overall operations under his or her control by preparing combined financial statements. Q3-20 Under the proprietary theory the parent company includes only a proportionate share of the assets and liabilities and income statement items of ...

FA2 Module 3. Cash Flow Statement

... Gains and losses are generally not included in operating activities; the related cash flow is presented in the appropriate SCF section. Indirect method Gains are deducted from, and losses added back to, net income in the operating activities section. The related cash flow is presented in the appropr ...

... Gains and losses are generally not included in operating activities; the related cash flow is presented in the appropriate SCF section. Indirect method Gains are deducted from, and losses added back to, net income in the operating activities section. The related cash flow is presented in the appropr ...

alternative leasing arrangements

... period (say next year), you could return it to the lessor but you will owe a large termination fee (perhaps equal to all remaining lease rental payments). This means that, with lease, the cost of the asset per year could be extraordinarily high if your need for it ends soon after signing the lease. ...

... period (say next year), you could return it to the lessor but you will owe a large termination fee (perhaps equal to all remaining lease rental payments). This means that, with lease, the cost of the asset per year could be extraordinarily high if your need for it ends soon after signing the lease. ...

EASTMAN CHEMICAL CO (Form: 8-K/A, Received

... Acquisition as if it had been completed on September 30, 2014. The accompanying Unaudited Pro Forma Condensed Combined Statements of Earnings (the "Pro Forma Income Statements") for the nine months ended September 30, 2014 and the year ended December 31, 2013 combine the historical consolidated stat ...

... Acquisition as if it had been completed on September 30, 2014. The accompanying Unaudited Pro Forma Condensed Combined Statements of Earnings (the "Pro Forma Income Statements") for the nine months ended September 30, 2014 and the year ended December 31, 2013 combine the historical consolidated stat ...

Accounting WFR 19e

... • In a perpetual inventory system, each purchase and the cost of each sale are recorded in Merchandise Inventory. • Most companies using the perpetual inventory system. ...

... • In a perpetual inventory system, each purchase and the cost of each sale are recorded in Merchandise Inventory. • Most companies using the perpetual inventory system. ...

CHANGES IN FASB 13 RULES TO CHANGE COMMERCIAL REAL

... record nearly all leases on their balance sheets as a “right to use” asset, and a corresponding “future lease payment – liability.” What does this change mean to owners and tenants of commercial real estate in simple terms? This proposal does away with operating leases; all leases would be capitaliz ...

... record nearly all leases on their balance sheets as a “right to use” asset, and a corresponding “future lease payment – liability.” What does this change mean to owners and tenants of commercial real estate in simple terms? This proposal does away with operating leases; all leases would be capitaliz ...

EdR Provides Update on Investments, Funding and

... communities we owned at both January 1, 2016, and 2017 whose operations are comparable on a same-community basis and not impacted by redevelopment or other significant nonoperational changes. A total of 3,124 of the 2017 same-community beds were classified as new communities in 2016. A total of 1,22 ...

... communities we owned at both January 1, 2016, and 2017 whose operations are comparable on a same-community basis and not impacted by redevelopment or other significant nonoperational changes. A total of 3,124 of the 2017 same-community beds were classified as new communities in 2016. A total of 1,22 ...

Depreciation

In accountancy, depreciation refers to two aspects of the same concept: the decrease in value of assets (fair value depreciation), and the allocation of the cost of assets to periods in which the assets are used (depreciation with the matching principle).A method of reallocating the cost of a tangible asset over its useful life span of it being in motion. Businesses depreciate long-term assets for both tax and accounting purposes.The former affects the balance sheet of a business or entity, and the latter affects the net income that they report. Generally the cost is allocated, as depreciation expense, among the periods in which the asset is expected to be used. This expense is recognized by businesses for financial reporting and tax purposes. Methods of computing depreciation, and the periods over which assets are depreciated, may vary between asset types within the same business and may vary for tax purposes. These may be specified by law or accounting standards, which may vary by country. There are several standard methods of computing depreciation expense, including fixed percentage, straight line, and declining balance methods. Depreciation expense generally begins when the asset is placed in service. For example, a depreciation expense of 100 per year for 5 years may be recognized for an asset costing 500.