Bonus Assignment solution

... “if”) – then this would be a $2.4 billion cost savings per year, or an additional $2.4 billion of pretax income. Income tax is currently about 30% of its income, so that would leave $1.7 billion of additional net income. This amount would increase TWX earnings per share by 44%. Therefore cost saving ...

... “if”) – then this would be a $2.4 billion cost savings per year, or an additional $2.4 billion of pretax income. Income tax is currently about 30% of its income, so that would leave $1.7 billion of additional net income. This amount would increase TWX earnings per share by 44%. Therefore cost saving ...

chapter 2 - CSUN.edu

... Study Objective 3 - Identify the Two Constraints in Accounting Constraints allow a company to modify generally accepted accounting principles without reducing the usefulness of the information content. These constraints are: Materiality - an item is material if it can influence the decision of an ...

... Study Objective 3 - Identify the Two Constraints in Accounting Constraints allow a company to modify generally accepted accounting principles without reducing the usefulness of the information content. These constraints are: Materiality - an item is material if it can influence the decision of an ...

Here

... • Hide the “Beginning” column and any other monthly balance sheet columns prior to the actual beginning balance sheet. Using the example above, you would hide “Beginning” and “January.” Financial Ratios are calculated based on the data entered. Industry numbers can be entered for comparison purposes ...

... • Hide the “Beginning” column and any other monthly balance sheet columns prior to the actual beginning balance sheet. Using the example above, you would hide “Beginning” and “January.” Financial Ratios are calculated based on the data entered. Industry numbers can be entered for comparison purposes ...

Intangible Capital and the “Market to Book Value”

... First, suppose that PHARMA were to purchase $10 million in tangible capital from another company, for example, a technologically advanced piece of laboratory equipment. The standard economic assumption underlying this purchase is that PHARMA invests up to the point that the $10 million cost of the n ...

... First, suppose that PHARMA were to purchase $10 million in tangible capital from another company, for example, a technologically advanced piece of laboratory equipment. The standard economic assumption underlying this purchase is that PHARMA invests up to the point that the $10 million cost of the n ...

Chapter 11

... administrative reasons that have little or nothing to do with value maximization. The important thing about soft rationing is that the corporation as a whole isn't short of capital; more can be raised on ordinary terms if management so desires. Ongoing soft rationing means we are constantly bypassin ...

... administrative reasons that have little or nothing to do with value maximization. The important thing about soft rationing is that the corporation as a whole isn't short of capital; more can be raised on ordinary terms if management so desires. Ongoing soft rationing means we are constantly bypassin ...

Chapter 3

... • Measuring transactions requires that certain expenses and revenues be allocated over several accounting periods. • The accountant assumes the business is a going concern (the business will continue to operate indefinitely, unless there is evidence to the contrary). • This allows the cost of certai ...

... • Measuring transactions requires that certain expenses and revenues be allocated over several accounting periods. • The accountant assumes the business is a going concern (the business will continue to operate indefinitely, unless there is evidence to the contrary). • This allows the cost of certai ...

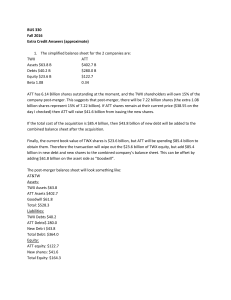

Condensed Income Statement

... combined the Comprehensive cost of goods and cost of services. (2) Minority interest expense is normally reported as a pre-tax nonoperating item, but it is sometimes reported as an operating item. If so, we include it as a part of costs of goods sold. (3) We want to report any depreciation as a sepa ...

... combined the Comprehensive cost of goods and cost of services. (2) Minority interest expense is normally reported as a pre-tax nonoperating item, but it is sometimes reported as an operating item. If so, we include it as a part of costs of goods sold. (3) We want to report any depreciation as a sepa ...

BUS103: Subunit 1.3.7.2 “Principles of Accounting Transactions

... of and understand the financial health of the company. An accounting transaction is defined as a part of an accounting system that is a record of money either spent to pay bills, buy inventory, and so forth, or money received from customers, loans, debt collection, and so forth. Transactions are rec ...

... of and understand the financial health of the company. An accounting transaction is defined as a part of an accounting system that is a record of money either spent to pay bills, buy inventory, and so forth, or money received from customers, loans, debt collection, and so forth. Transactions are rec ...

Viewpoints: Impairment of Exploration and Evaluation Assets (Mining)

... suggest that the carrying amount of an E&E asset may exceed its recoverable amount. According to IFRS 6, one or more of the following facts and circumstances indicate that an entity should test E&E assets for impairment: a. the period for which the entity has the right to explore in the specific ar ...

... suggest that the carrying amount of an E&E asset may exceed its recoverable amount. According to IFRS 6, one or more of the following facts and circumstances indicate that an entity should test E&E assets for impairment: a. the period for which the entity has the right to explore in the specific ar ...

FY 2004-2005 - FSM National Public Auditor

... There was no restricted net assets at September 30, 2004 or 2005. Unrestricted, in which case assets may be designated for purposes designated by the Committee, or Management. F. Use of Estimates. The preparation of financial statements in conformity with generally accepted accounting principles req ...

... There was no restricted net assets at September 30, 2004 or 2005. Unrestricted, in which case assets may be designated for purposes designated by the Committee, or Management. F. Use of Estimates. The preparation of financial statements in conformity with generally accepted accounting principles req ...

GLOSSARY OF COLLEGE STORE OPERATIONS TERMS

... sold during (gross profit) a stated time frame, excluding the selling and other operating expenses. ...

... sold during (gross profit) a stated time frame, excluding the selling and other operating expenses. ...

Adjusting Entry

... LO1 Revenue and Expense Reporting o Accounting information – necessary for decision making. o To be useful in decision making – accountants must report revenues and expenses in a way that reflects the ability of the company to create value for its owners. o Accrual-basis accounting records revenues ...

... LO1 Revenue and Expense Reporting o Accounting information – necessary for decision making. o To be useful in decision making – accountants must report revenues and expenses in a way that reflects the ability of the company to create value for its owners. o Accrual-basis accounting records revenues ...

Non-Bank Finance Companies Criteria

... and predictability of earnings over a period rather than a position at a particular point in time. Ind-Ra also looks at operating expenses relative to loans or leases, including the mix of variable and fixed costs. Ind-Ra recognizes that NBFCs may have very different cost structures. For example, an ...

... and predictability of earnings over a period rather than a position at a particular point in time. Ind-Ra also looks at operating expenses relative to loans or leases, including the mix of variable and fixed costs. Ind-Ra recognizes that NBFCs may have very different cost structures. For example, an ...

ALTERNATE MARKETING NETWORKS INC

... The following unaudited pro forma consolidated financial statements give effect to the purchase by Alternate Marketing Networks, Inc. (the "Company") of Total Logistics, Inc. ("TLI"). Pro forma adjustments related to the pro forma consolidated balance sheet have been determined assuming the combinat ...

... The following unaudited pro forma consolidated financial statements give effect to the purchase by Alternate Marketing Networks, Inc. (the "Company") of Total Logistics, Inc. ("TLI"). Pro forma adjustments related to the pro forma consolidated balance sheet have been determined assuming the combinat ...

Working Capital Finance

... Traders, Merchants, exporters etc. who do not have fixed operating cycle. ...

... Traders, Merchants, exporters etc. who do not have fixed operating cycle. ...

WIS ACCOUNTING BASICS

... External users are parties outside the reporting entity (company) who are interested in the accounting information. Investors (owners) use accounting information to make buy, sell or keep decisions related to shares, bonds, etc. Creditors (suppliers, banks) utilize accounting information to make len ...

... External users are parties outside the reporting entity (company) who are interested in the accounting information. Investors (owners) use accounting information to make buy, sell or keep decisions related to shares, bonds, etc. Creditors (suppliers, banks) utilize accounting information to make len ...

Managerial Discretion, Matching and the Market

... way accounting information is used by markets (market objective). The literature on empirical research on accounting choice is surveyed by Fields et al. (2001). 3 For a related method, but looking at R&D expenditures, see Lev and Sougiannis (1996). ...

... way accounting information is used by markets (market objective). The literature on empirical research on accounting choice is surveyed by Fields et al. (2001). 3 For a related method, but looking at R&D expenditures, see Lev and Sougiannis (1996). ...

NBER WORKING PAPER SERIES INEFFICIENCY OF CORPORATE INVESTMENT AND DISTORTION OF SAVINGS

... resources. At the other extreme, for families who do not own any land and aspire to acquire it, an increase in the price of land is a significant increase in the cost of living without a compensating increase in their income. Although there are thus significant allocative consequences within the hou ...

... resources. At the other extreme, for families who do not own any land and aspire to acquire it, an increase in the price of land is a significant increase in the cost of living without a compensating increase in their income. Although there are thus significant allocative consequences within the hou ...

The Balance Sheet: Assets, Debts and Equity

... which details a firm’s earnings and expenses over a period of time, the balance sheet lists all of a company’s assets and liabilities at a single point in time. The balance sheet provides a snapshot of a firm at the end of a fiscal quarter or year. The income, expenses and cash flow that come into a ...

... which details a firm’s earnings and expenses over a period of time, the balance sheet lists all of a company’s assets and liabilities at a single point in time. The balance sheet provides a snapshot of a firm at the end of a fiscal quarter or year. The income, expenses and cash flow that come into a ...

HelpWithAssignment.com

... company’s revenues and expenses over a period of time. The last or the bottom line of the income statement shows the company’s net income, which is a measure of its profitability during the period. The income statement is sometimes called a profit and loss statement and the net income is referred to ...

... company’s revenues and expenses over a period of time. The last or the bottom line of the income statement shows the company’s net income, which is a measure of its profitability during the period. The income statement is sometimes called a profit and loss statement and the net income is referred to ...

Current Liabilities

... Understand the role and limitations of the Balance Sheet as a summary of the financial position of a business. Be able to work with a Balance Sheet in different formats Be able to work out the effect of business transactions on a Balance Sheet. Be able to discuss some of the Accounting Conventions a ...

... Understand the role and limitations of the Balance Sheet as a summary of the financial position of a business. Be able to work with a Balance Sheet in different formats Be able to work out the effect of business transactions on a Balance Sheet. Be able to discuss some of the Accounting Conventions a ...

Financial Statement Analysis

... answer this, ask yourself whether you would prefer to buy a house using a one-year note that would have to be refinanced in twelve months, or a 30-year mortgage.) ...

... answer this, ask yourself whether you would prefer to buy a house using a one-year note that would have to be refinanced in twelve months, or a 30-year mortgage.) ...

Depreciation

In accountancy, depreciation refers to two aspects of the same concept: the decrease in value of assets (fair value depreciation), and the allocation of the cost of assets to periods in which the assets are used (depreciation with the matching principle).A method of reallocating the cost of a tangible asset over its useful life span of it being in motion. Businesses depreciate long-term assets for both tax and accounting purposes.The former affects the balance sheet of a business or entity, and the latter affects the net income that they report. Generally the cost is allocated, as depreciation expense, among the periods in which the asset is expected to be used. This expense is recognized by businesses for financial reporting and tax purposes. Methods of computing depreciation, and the periods over which assets are depreciated, may vary between asset types within the same business and may vary for tax purposes. These may be specified by law or accounting standards, which may vary by country. There are several standard methods of computing depreciation expense, including fixed percentage, straight line, and declining balance methods. Depreciation expense generally begins when the asset is placed in service. For example, a depreciation expense of 100 per year for 5 years may be recognized for an asset costing 500.