LF and FEM

... together to determine equilibrium, and then the effects of shifts in demand and supply are analyzed. • The two markets are linked together and r, NCO, EP/P*, and NX are jointly determined. • Different policies and situations are then analyzed and their affect on r, NCO, EP/P*, and NX identified. ...

... together to determine equilibrium, and then the effects of shifts in demand and supply are analyzed. • The two markets are linked together and r, NCO, EP/P*, and NX are jointly determined. • Different policies and situations are then analyzed and their affect on r, NCO, EP/P*, and NX identified. ...

Screen Information, Trader Activity, and Bid-Ask

... electronic limit order book systems for equities, derivatives, and bonds. This development has generated a growing literature on order flow and its contribution to market activity and price formation.1 We analyze the links between information observed through the system by traders, order placement b ...

... electronic limit order book systems for equities, derivatives, and bonds. This development has generated a growing literature on order flow and its contribution to market activity and price formation.1 We analyze the links between information observed through the system by traders, order placement b ...

NBER WORKING PAPER SERIES HOUSING DYNAMICS Edward L. Glaeser Joseph Gyourko

... Enterprise Oversight (OFHEO) constant quality house price series, a $1 increase in real house prices in one year is associated with a 71 cent increase the next year. A $1 increase in local market prices over the past five years is associated with a 32 cent decrease over the next five year period. Th ...

... Enterprise Oversight (OFHEO) constant quality house price series, a $1 increase in real house prices in one year is associated with a 71 cent increase the next year. A $1 increase in local market prices over the past five years is associated with a 32 cent decrease over the next five year period. Th ...

FTR Auction Design for the California ISO

... case the auction will take a long time, because for example if demand exceeds supply by 20 percent it will take about a half dozen rounds before all the bidders will have had to bid once. The other is that we require not only losing bidders but those within the next bid increment to raise their bids ...

... case the auction will take a long time, because for example if demand exceeds supply by 20 percent it will take about a half dozen rounds before all the bidders will have had to bid once. The other is that we require not only losing bidders but those within the next bid increment to raise their bids ...

Trading and Electronic Markets

... They keep perfect audit trails. Electronic exchange systems that support hidden orders keep those orders perfectly hidden—unlike floor brokers, who may inadvertently or fraudulently reveal their clients’ hidden orders to friends or confederates. Electronic order-matching systems do not get tired, ca ...

... They keep perfect audit trails. Electronic exchange systems that support hidden orders keep those orders perfectly hidden—unlike floor brokers, who may inadvertently or fraudulently reveal their clients’ hidden orders to friends or confederates. Electronic order-matching systems do not get tired, ca ...

PDF

... seasonality. Chen et al. (2010) found that exchange rates are very useful in forecasting future commodity prices but not vice versa. They also found positive relationship between exchange rate and international commodity prices. More recent studies consider a time period when China had already devel ...

... seasonality. Chen et al. (2010) found that exchange rates are very useful in forecasting future commodity prices but not vice versa. They also found positive relationship between exchange rate and international commodity prices. More recent studies consider a time period when China had already devel ...

Chapter 10

... • By doing so, investors could earn an additional premium without taking on additional risk. This opportunity to earn something for nothing would quickly be exploited and eliminated. Because investors can eliminate firm-specific risk “for free” by diversifying their portfolios, they will not require ...

... • By doing so, investors could earn an additional premium without taking on additional risk. This opportunity to earn something for nothing would quickly be exploited and eliminated. Because investors can eliminate firm-specific risk “for free” by diversifying their portfolios, they will not require ...

Market Makers

... 614D. A Market Maker wishing to conduct Options Hedging Short Selling shall notify the Exchange of its intention. A Market Maker may also apply to the Exchange to register one or more Exchange Participants as its Options Hedging Participants which will conduct on its behalf Options Hedging Transact ...

... 614D. A Market Maker wishing to conduct Options Hedging Short Selling shall notify the Exchange of its intention. A Market Maker may also apply to the Exchange to register one or more Exchange Participants as its Options Hedging Participants which will conduct on its behalf Options Hedging Transact ...

Intraday Returns and the Day-end Effect: Evidence from

... Güray Küçükkocaoğlu∗ Abstract In this paper, we examine the behavior of the intra-daily stock returns and close-end stock price manipulation in the Istanbul Stock Exchange (ISE). Understanding the price behavior in a given trading day could help investors when they are making their buy and sell deci ...

... Güray Küçükkocaoğlu∗ Abstract In this paper, we examine the behavior of the intra-daily stock returns and close-end stock price manipulation in the Istanbul Stock Exchange (ISE). Understanding the price behavior in a given trading day could help investors when they are making their buy and sell deci ...

A Single Protocol for Clearing and Settlement?

... “Define EU wide protocol to eliminate national differences in IT & interfaces used by Clearing & Settlement providers” ...

... “Define EU wide protocol to eliminate national differences in IT & interfaces used by Clearing & Settlement providers” ...

A Single Protocol for Clearing and Settlement?

... “Define EU wide protocol to eliminate national differences in IT & interfaces used by Clearing & Settlement providers” ...

... “Define EU wide protocol to eliminate national differences in IT & interfaces used by Clearing & Settlement providers” ...

Article 81(1)

... MVBER - Outline • Follows a similar pattern to VABER • Applies to agreements at all levels of vehicle distribution in respect of: – Sale of new motor cars and commercial vehicles – After-sale servicing – Spare part supply ...

... MVBER - Outline • Follows a similar pattern to VABER • Applies to agreements at all levels of vehicle distribution in respect of: – Sale of new motor cars and commercial vehicles – After-sale servicing – Spare part supply ...

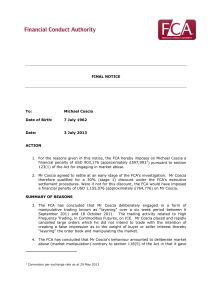

FINAL NOTICE: Michael Coscia

... 23. The orders placed by Mr Coscia were resting on the order book for typically less than one second. The FCA has concluded that placing the large orders for such a short period of time and automatically cancelling the remainder of a large order in the event of a partial execution made it very unlik ...

... 23. The orders placed by Mr Coscia were resting on the order book for typically less than one second. The FCA has concluded that placing the large orders for such a short period of time and automatically cancelling the remainder of a large order in the event of a partial execution made it very unlik ...

ASX Clear Section 11 - Derivatives Market Contracts – Allocation

... Participant may allocate Derivatives Market Contracts If a Derivatives Market Contract is reported to ASX Clear for registration in the name of a Participant (the “First Participant”), the First Participant may, before the Derivatives Market Contract is registered, allocate the contract to another P ...

... Participant may allocate Derivatives Market Contracts If a Derivatives Market Contract is reported to ASX Clear for registration in the name of a Participant (the “First Participant”), the First Participant may, before the Derivatives Market Contract is registered, allocate the contract to another P ...

The IOSCO Transparency Principle and Modelling the Bid

... one year of trade-level data obtained from the JSE. These two sources facilitated the assessment of transparency and liquidity in the market. In the current market regime there is fairly accurate provision of historical trade activity and pre-trade transparency is available through quotes provided b ...

... one year of trade-level data obtained from the JSE. These two sources facilitated the assessment of transparency and liquidity in the market. In the current market regime there is fairly accurate provision of historical trade activity and pre-trade transparency is available through quotes provided b ...

a survey of strategic market games

... A trivial strategy is a strategy where a trader’s bids and offers are zero. A trivial strategy in SMGs leads to no-trade equilibrium. If the trivial equilibrium is the only equilibrium in the game, then the initial allocation of endowments is already Pareto efficient and the game does not have any t ...

... A trivial strategy is a strategy where a trader’s bids and offers are zero. A trivial strategy in SMGs leads to no-trade equilibrium. If the trivial equilibrium is the only equilibrium in the game, then the initial allocation of endowments is already Pareto efficient and the game does not have any t ...

Derivatives and Volatility on Indian Stock Markets

... cash markets has remained an active topic of analytic and empirical interest. Questions pertaining to the impact of derivative trading on cash market volatility have been empirically addressed in two ways: by comparing cash market volatilities during the pre-and post-futures/ options trading eras an ...

... cash markets has remained an active topic of analytic and empirical interest. Questions pertaining to the impact of derivative trading on cash market volatility have been empirically addressed in two ways: by comparing cash market volatilities during the pre-and post-futures/ options trading eras an ...

Estimating a Structural Model of Herd Behavior in Financial Markets

... by the data, which implies both that herd behavior arises in equilibrium and that there is information content in the sequence of trades. Note that in each day of trading there is always high heterogeneity in trading decisions (i.e., even in days when the fundamental value has increased, we observe ...

... by the data, which implies both that herd behavior arises in equilibrium and that there is information content in the sequence of trades. Note that in each day of trading there is always high heterogeneity in trading decisions (i.e., even in days when the fundamental value has increased, we observe ...

New Issue of Securities (Chapter 6 of Listing Requirements): Fund

... 22,243,000 new ordinary shares of RM0.10 each in Cuscapi to be issued pursuant to the Proposed Private Placement, on the ACE Market of Bursa Securities, subject to the following conditions:(i) Cuscapi and KIBB must fully comply with the relevant provisions under Bursa Securities ACE Market Listing R ...

... 22,243,000 new ordinary shares of RM0.10 each in Cuscapi to be issued pursuant to the Proposed Private Placement, on the ACE Market of Bursa Securities, subject to the following conditions:(i) Cuscapi and KIBB must fully comply with the relevant provisions under Bursa Securities ACE Market Listing R ...

Testing for imperfect competition at the Fulton fish market - U

... quoted law enforcement officers as saying the market has been a Mafia stronghold for 60 years (Raab, 1991). According to investigations, Mafia activity is primarily present in the unloading activities and the parking arrangements of the customers:. The whiting market. I chose whiting for this study ...

... quoted law enforcement officers as saying the market has been a Mafia stronghold for 60 years (Raab, 1991). According to investigations, Mafia activity is primarily present in the unloading activities and the parking arrangements of the customers:. The whiting market. I chose whiting for this study ...

Chapter 15 PPP

... • Buyer/holder has legally binding obligation to take delivery on specified date • Futures may be held until delivery date or traded on futures market • All trading is done on a margin basis ...

... • Buyer/holder has legally binding obligation to take delivery on specified date • Futures may be held until delivery date or traded on futures market • All trading is done on a margin basis ...

Abstract Edward Chamberlin, who initiated classroom

... Experimental economics began in the 1940’s in Edward Chamberlin’s Harvard classroom. Chamberlin devised a classroom trading pit that served two purposes— instructing the participating economics students and testing scientific propositions. Chamberlin “induced” market demand and supply by distributi ...

... Experimental economics began in the 1940’s in Edward Chamberlin’s Harvard classroom. Chamberlin devised a classroom trading pit that served two purposes— instructing the participating economics students and testing scientific propositions. Chamberlin “induced” market demand and supply by distributi ...

Annuities Market in Kenya - Retirement Benefits Authority

... they may receive worse terms on an annuity that is available to the open market. Also there is a need for more general competition regulation to ensure that prices are not artificially boosted by monopoly. But as discussed in this paper, stringent prudential regulation may also be required to preven ...

... they may receive worse terms on an annuity that is available to the open market. Also there is a need for more general competition regulation to ensure that prices are not artificially boosted by monopoly. But as discussed in this paper, stringent prudential regulation may also be required to preven ...

FTRs: Necessary or Burdensome?

... • Provides hedging against congestion costs • Partially “completes” the “Arrow-Debreu” markets with respect to congestion costs • Provides signals for new generation and transmission (especially with long-term FTRs) • FTRs cannot be withheld to raise energy prices (as opposed to physical transmissio ...

... • Provides hedging against congestion costs • Partially “completes” the “Arrow-Debreu” markets with respect to congestion costs • Provides signals for new generation and transmission (especially with long-term FTRs) • FTRs cannot be withheld to raise energy prices (as opposed to physical transmissio ...