The Payments System and the Market for Interbank Funds

... agent-based model in the spirit of models applied to understanding self-organized criticality.8 Physicists have used these models to study cascading phenomena in a variety of systems (for instance, Jensen [1998]), where models made of very simple agents, interacting with neighboring agents, can yiel ...

... agent-based model in the spirit of models applied to understanding self-organized criticality.8 Physicists have used these models to study cascading phenomena in a variety of systems (for instance, Jensen [1998]), where models made of very simple agents, interacting with neighboring agents, can yiel ...

Regulation and the National Regulatory Authority in

... Flexibility in price regulation Current situation Distortions Rigidity • Cost oriented prices for each service • Is it reasonable? ...

... Flexibility in price regulation Current situation Distortions Rigidity • Cost oriented prices for each service • Is it reasonable? ...

Table 1: Granger Causality Testing between Prices and Volumes

... temporal asymmetry is evident if trading volume responds significantly differently to positive lagged price changes than to negative lagged price changes. Testing for temporal asymmetry is important due to the implications of its existence on the trading actions and investment strategies of market p ...

... temporal asymmetry is evident if trading volume responds significantly differently to positive lagged price changes than to negative lagged price changes. Testing for temporal asymmetry is important due to the implications of its existence on the trading actions and investment strategies of market p ...

Market coupling - Houmoller Consulting ApS

... Unfortunately, instead the Nord Pool Spot recalculation still takes place Now with some information on the German and Dutch bids feed to the Nord Pool Spot software. This is the so-called Iceberg solution • ”Iceberg” as the German/Dutch market situation is only partly visible for the Nord Pool ...

... Unfortunately, instead the Nord Pool Spot recalculation still takes place Now with some information on the German and Dutch bids feed to the Nord Pool Spot software. This is the so-called Iceberg solution • ”Iceberg” as the German/Dutch market situation is only partly visible for the Nord Pool ...

The synchronized and long-lasting structural change on

... break, characterized by correlations that have significantly departed from zero to positive territories since late September 2008 and have also remained exceptionally high as of December 2011. Our results support the presence of high frequency trading and algorithmic strategies on commodity markets ...

... break, characterized by correlations that have significantly departed from zero to positive territories since late September 2008 and have also remained exceptionally high as of December 2011. Our results support the presence of high frequency trading and algorithmic strategies on commodity markets ...

Derivatives Trading and Its Impact on the Volatility of NSE, India

... some pre-existing risk by taking positions in derivatives markets that offset potential losses in the underlying or spot market. In India, most derivatives users describe themselves as hedgers and Indian laws generally require that derivatives be used for hedging purposes only. Another motive for de ...

... some pre-existing risk by taking positions in derivatives markets that offset potential losses in the underlying or spot market. In India, most derivatives users describe themselves as hedgers and Indian laws generally require that derivatives be used for hedging purposes only. Another motive for de ...

Maker-Taker Pricing Effects on Market Quotations

... Holding constant the quoted bid and ask prices, the 0.3¢/share access fee effectively increases net bid-ask spreads paid by makers by 0.6¢/share over the quoted market spreads. Buyers who initiate trades pay the quoted ask price plus the 0.3¢ access fee while taking sellers receive the quoted bid pr ...

... Holding constant the quoted bid and ask prices, the 0.3¢/share access fee effectively increases net bid-ask spreads paid by makers by 0.6¢/share over the quoted market spreads. Buyers who initiate trades pay the quoted ask price plus the 0.3¢ access fee while taking sellers receive the quoted bid pr ...

decentralized trade mitigates the lemons problem

... Wolinsky (1985, 1990). Except for introducing adverse selection, our model of decentralized trade is standard—in Rubinstein and Wolinsky (1985) traders engage in an alternating offer bargaining game, while in Gale (1987) one agent in a match is randomly selected to make a take-it-or-leave-it price o ...

... Wolinsky (1985, 1990). Except for introducing adverse selection, our model of decentralized trade is standard—in Rubinstein and Wolinsky (1985) traders engage in an alternating offer bargaining game, while in Gale (1987) one agent in a match is randomly selected to make a take-it-or-leave-it price o ...

Webtrader Business Terms For Securities Trading

... Client in case of extraordinary circumstances, which shall include without limitation the circumstances set out in clause 13. A Client cannot enter an order into the Trading Platform on conditions fully or partially identical to another unexecuted trade entered into the Trading Platform system by th ...

... Client in case of extraordinary circumstances, which shall include without limitation the circumstances set out in clause 13. A Client cannot enter an order into the Trading Platform on conditions fully or partially identical to another unexecuted trade entered into the Trading Platform system by th ...

Momentum Effect: Empirical Evidence from Karachi Stock Exchange

... strongly believe that the markets are efficient in pricing the financial instruments. This view became popular after Fama’s work on the Efficient Market Hypothesis. But before 1990’s, wide-ranging financial literature documented that stock prices, to some extent, are predictable. Many psychologists, ...

... strongly believe that the markets are efficient in pricing the financial instruments. This view became popular after Fama’s work on the Efficient Market Hypothesis. But before 1990’s, wide-ranging financial literature documented that stock prices, to some extent, are predictable. Many psychologists, ...

Forecasting Prices in the Presence of Hidden Liquidity

... rerouted to those venues. Thus, one needs to consider the possibility that once the best ask on an exchange is depleted, the price will not necessarily go up, since an ask order at that price may still be available on another market and a new bid cannot arrive until that price is cleared on all mark ...

... rerouted to those venues. Thus, one needs to consider the possibility that once the best ask on an exchange is depleted, the price will not necessarily go up, since an ask order at that price may still be available on another market and a new bid cannot arrive until that price is cleared on all mark ...

Chp 10 Slides File

... information about the firm, including financial statements and a discussion of risks. The prospectus is filed with the Securities and Exchange Commission (SEC). b. The lead underwriter must determine the offer price at which the shares will be offered at the time of the IPO. c. Allocation of IPO Sha ...

... information about the firm, including financial statements and a discussion of risks. The prospectus is filed with the Securities and Exchange Commission (SEC). b. The lead underwriter must determine the offer price at which the shares will be offered at the time of the IPO. c. Allocation of IPO Sha ...

NBER WORKING PAPER SERIES Kristin J. Forbes Working Paper 13908

... external debt ratios, and part of this adjustment will involve a large dollar depreciation (Obstfeld and Rogoff (2007) and Blanchard, Giavazzi and Sa (2005)). A more recent series of papers argues that this system of imbalances could continue for an extended period due to factors such as: difference ...

... external debt ratios, and part of this adjustment will involve a large dollar depreciation (Obstfeld and Rogoff (2007) and Blanchard, Giavazzi and Sa (2005)). A more recent series of papers argues that this system of imbalances could continue for an extended period due to factors such as: difference ...

OPEC Policy and Oil Prices - Oxford Institute for Energy Studies

... • New discoveries in non-OPEC countries responding to higher oil prices taking advantage of new technologies • Diversity of Consumers • Main Impact on Market • Collapse of OPEC administered system in 1986 • Saudi Arabia‟s attempts to defend marker price would only result in a dramatic reduction in i ...

... • New discoveries in non-OPEC countries responding to higher oil prices taking advantage of new technologies • Diversity of Consumers • Main Impact on Market • Collapse of OPEC administered system in 1986 • Saudi Arabia‟s attempts to defend marker price would only result in a dramatic reduction in i ...

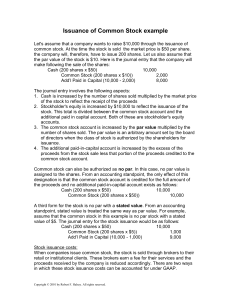

Issuance of Common Stock example

... A third form for the stock is no par with a stated value. From an accounting standpoint, stated value is treated the same way as par value. For example, assume that the common stock in this example is no par stock with a stated value of $5. The journal entry for the stock issuance would be as follow ...

... A third form for the stock is no par with a stated value. From an accounting standpoint, stated value is treated the same way as par value. For example, assume that the common stock in this example is no par stock with a stated value of $5. The journal entry for the stock issuance would be as follow ...

Shareholder Wealth and Volatility Effects of Stock Splits Some

... ments, earnings per share (annual results) and dividends is thus ignored in this study. My justification for this is the following. Firstly, a large part of the data would have been lost in controlling for the simultaneous information releases since the split / stock dividend is often announced in c ...

... ments, earnings per share (annual results) and dividends is thus ignored in this study. My justification for this is the following. Firstly, a large part of the data would have been lost in controlling for the simultaneous information releases since the split / stock dividend is often announced in c ...

High frequency trading: assessing the impact on market

... market making firms to quantitative hedge funds and their practices include a range of activities such as pseudo market-making and statistical arbitrage (“stat-arb”) trading. Though many of these trading approaches derive from strategies that have always existed in markets, the speed with which they ...

... market making firms to quantitative hedge funds and their practices include a range of activities such as pseudo market-making and statistical arbitrage (“stat-arb”) trading. Though many of these trading approaches derive from strategies that have always existed in markets, the speed with which they ...

Beck and Levine "Stock markets, banks, and growth: Panel evidence"

... used by Levine and Zervos (1998) and Rousseau and Wachtel (2000). Value traded equals the value of the trades of domestic shares on domestic exchanges divided by GDP. Value traded has two potential pitfalls. First, it does not measure the liquidity of the market. It measures trading relative to the ...

... used by Levine and Zervos (1998) and Rousseau and Wachtel (2000). Value traded equals the value of the trades of domestic shares on domestic exchanges divided by GDP. Value traded has two potential pitfalls. First, it does not measure the liquidity of the market. It measures trading relative to the ...

Paying for Market Quality

... we also add to this stream of literature by explicitly analysing the terms of the contracts between firms and the market-makers responsible for providing liquidity. We can thus study the economic rationale of these arrangements as well as the interaction between contractual minimum market quality st ...

... we also add to this stream of literature by explicitly analysing the terms of the contracts between firms and the market-makers responsible for providing liquidity. We can thus study the economic rationale of these arrangements as well as the interaction between contractual minimum market quality st ...

Chapter 4: Using Futures Markets

... A hedger is an individual who enters the futures market in order to reduce a preexisting risk. A preexisting position might include: 1. A commodity that you own: you have a silver mining company and have silver stored. You own the commodity. 2. An anticipatory hedge: a commodity that you will acquir ...

... A hedger is an individual who enters the futures market in order to reduce a preexisting risk. A preexisting position might include: 1. A commodity that you own: you have a silver mining company and have silver stored. You own the commodity. 2. An anticipatory hedge: a commodity that you will acquir ...

Electronic Market-Makers: Empirical Comparison

... around the world. Electronic market-makers use technology to create efficiencies and reduce trading costs for investors. Electronic market-makers are also responsible for maintaining the liquidity and orderly price transitions [17]. A market is called a liquid market if traders can buy or sell large ...

... around the world. Electronic market-makers use technology to create efficiencies and reduce trading costs for investors. Electronic market-makers are also responsible for maintaining the liquidity and orderly price transitions [17]. A market is called a liquid market if traders can buy or sell large ...

Prestigious Stock Exchanges - Federal Reserve Bank of New York

... understanding of global equity activity and allows for a superior assessment of the relative importance of the population of stock exchanges. Now, it is clear that in circumstances where most of the cross-listing flows are directed to just one stock exchange location, the statistics contained in th ...

... understanding of global equity activity and allows for a superior assessment of the relative importance of the population of stock exchanges. Now, it is clear that in circumstances where most of the cross-listing flows are directed to just one stock exchange location, the statistics contained in th ...

Chapter 1 DIFFERENCES OF OPINION AND THE VOLUME OF

... for differences in beliefs across agents; see Jarrow (1980), Lintner (1969), Mayshar (1983), and Williams (1977). Differences in beliefs in contingent commodities models have received much less attention. The major references are Rubinstein (1975), (1976), Breeden-Litzenberger (1978), Hakansson-Kunk ...

... for differences in beliefs across agents; see Jarrow (1980), Lintner (1969), Mayshar (1983), and Williams (1977). Differences in beliefs in contingent commodities models have received much less attention. The major references are Rubinstein (1975), (1976), Breeden-Litzenberger (1978), Hakansson-Kunk ...

CHAPTER 11

... Arbitrage, Risk Arbitrage, and Equilibrium The critical property of a risk-free arbitrage portfolio is that any investor, regardless of risk aversion or wealth, will want to take an infinite position in it. Because those large positions will quickly force prices up or down until the opportunity v ...

... Arbitrage, Risk Arbitrage, and Equilibrium The critical property of a risk-free arbitrage portfolio is that any investor, regardless of risk aversion or wealth, will want to take an infinite position in it. Because those large positions will quickly force prices up or down until the opportunity v ...

The Effects of Capital Structure Change on Security Prices

... borne by the firm in the process of redistributing wealth among classes of securityholders, Technological limitations on the number of profitable investment projects also offer some measure of natural protection. ...

... borne by the firm in the process of redistributing wealth among classes of securityholders, Technological limitations on the number of profitable investment projects also offer some measure of natural protection. ...