Lecture 17

... The first will allow us to change probability measure so that the discounted asset prices are martingales. Recall that in our discrete time world, once we had such a martingale measure, the pricing of options was reduced to calculating expectations under that measure. In the continuous world it will ...

... The first will allow us to change probability measure so that the discounted asset prices are martingales. Recall that in our discrete time world, once we had such a martingale measure, the pricing of options was reduced to calculating expectations under that measure. In the continuous world it will ...

FIN 377L – Portfolio Analysis and Management

... However, her revised view is that they also will not increase in value much, if at all. ...

... However, her revised view is that they also will not increase in value much, if at all. ...

Title A Note on Look-Back Options Based on Order - HERMES-IR

... value of the cr-Percentile. This may be obtained by some more effort. Now we outline the present paper. In Section II, the notations and the definitions are given. In Section 111, the unconditional and the conditional distribution of the i-th order statistic of the prices of the underlying asset are ...

... value of the cr-Percentile. This may be obtained by some more effort. Now we outline the present paper. In Section II, the notations and the definitions are given. In Section 111, the unconditional and the conditional distribution of the i-th order statistic of the prices of the underlying asset are ...

here

... 16. (6 points) Marilyn owns a European call option for TMIWD, Inc. The option has an exercise price of $130, with an expiration date one year from today. If Marilyn assumes that TMIWD stock’s value on the expiration date comes from a uniform distribution, with all prices between $100-$140 equally l ...

... 16. (6 points) Marilyn owns a European call option for TMIWD, Inc. The option has an exercise price of $130, with an expiration date one year from today. If Marilyn assumes that TMIWD stock’s value on the expiration date comes from a uniform distribution, with all prices between $100-$140 equally l ...

Absolute Dividends

... correlation, however the implied volatility depends on and therefore intuitively we need to strip off this ...

... correlation, however the implied volatility depends on and therefore intuitively we need to strip off this ...

Arbitrage Opportunities in Misspecified Stochastic volatility Models

... from a single trajectory of the underlying in an almost sure way, their misspecification leads, in principle, to an arbitrage opportunity. The questions are whether this opportunity can be realized with a feasible strategy, and how to construct a strategy maximizing the arbitrage gain under suitable ...

... from a single trajectory of the underlying in an almost sure way, their misspecification leads, in principle, to an arbitrage opportunity. The questions are whether this opportunity can be realized with a feasible strategy, and how to construct a strategy maximizing the arbitrage gain under suitable ...

Chapter 5

... Using continuous compounding to revalue the call option from the previous example: ...

... Using continuous compounding to revalue the call option from the previous example: ...

ch05 - U of L Class Index

... Using continuous compounding to revalue the call option from the previous example: ...

... Using continuous compounding to revalue the call option from the previous example: ...

testimony of christine a - North American Securities Administrators

... Top Emerging Investor Threats Binary Options: Binary options are securities in the form of options contracts that have a payout that depends on whether the underlying asset – for example, a company’s stock or a stock index – increases or decreases in value. In such an all-or nothing payout structur ...

... Top Emerging Investor Threats Binary Options: Binary options are securities in the form of options contracts that have a payout that depends on whether the underlying asset – for example, a company’s stock or a stock index – increases or decreases in value. In such an all-or nothing payout structur ...

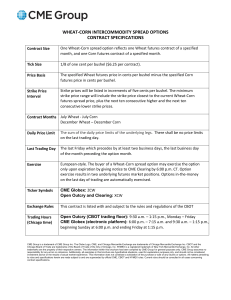

VARIABLE STRIKE OPTIONS and GUARANTEES in LIFE

... and hedging strategies, overcoming the traditional risk profile. The innovation process leads to new kinds of exotic options and it modifies the typical elements such as the underlying, the strike price, the maturity. In this note, we are especially interested with the development of the strike pric ...

... and hedging strategies, overcoming the traditional risk profile. The innovation process leads to new kinds of exotic options and it modifies the typical elements such as the underlying, the strike price, the maturity. In this note, we are especially interested with the development of the strike pric ...

Answers to Chapter 23 Questions

... -(LIBOR + 1.5%) which is less than its current variable rate payment. Bank 2 can issue floating rate CDs at (LIBOR + 3%), pay 13%, and receive (LIBOR + 3.5%). Its net cost is 12.5% which is less than its current fixed payment. 17. A hedge with futures contracts produces symmetric gains and losses wi ...

... -(LIBOR + 1.5%) which is less than its current variable rate payment. Bank 2 can issue floating rate CDs at (LIBOR + 3%), pay 13%, and receive (LIBOR + 3.5%). Its net cost is 12.5% which is less than its current fixed payment. 17. A hedge with futures contracts produces symmetric gains and losses wi ...

colour ppt

... Options A Brief History of Options Markets • The concept of an option existed in ancient Greece and Rome. • Options were used by speculators in the tulip craze of seventeenthcentury Holland. Tulips bulbs were traded as a speculative commodity by many of the Dutch, with prices reaching 1000 times th ...

... Options A Brief History of Options Markets • The concept of an option existed in ancient Greece and Rome. • Options were used by speculators in the tulip craze of seventeenthcentury Holland. Tulips bulbs were traded as a speculative commodity by many of the Dutch, with prices reaching 1000 times th ...

Recovering Risk-Neutral Densities from Exchange Rate Options: Evidence in Turkey

... European Monetary System to assess the credibility of commitments to exchange rate target zones and determine whether the bandwidths are consistent with the market expectations. The RND could also be utilized in testing the rationality and measuring risk attitude of investors, which are highly impor ...

... European Monetary System to assess the credibility of commitments to exchange rate target zones and determine whether the bandwidths are consistent with the market expectations. The RND could also be utilized in testing the rationality and measuring risk attitude of investors, which are highly impor ...