Trade Size and the Cross Section of Stock Returns

... Researchers have also presented opposing evidence of trade size impact on stock returns. On one hand, trade size is significant in addition to number of trades and trade imbalance so that trade size and information set are positively correlated (Kim and Verrecchia, 1991; Chan and Fong, 2000), advers ...

... Researchers have also presented opposing evidence of trade size impact on stock returns. On one hand, trade size is significant in addition to number of trades and trade imbalance so that trade size and information set are positively correlated (Kim and Verrecchia, 1991; Chan and Fong, 2000), advers ...

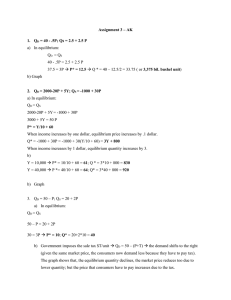

1 Suggested Answers to Review Questions

... production is not a large enough proportion of the total farm product to have much impact on the price. As a result, price does not change (or changes by only a slight amount), while the output of Thai farmers declines, thus reducing their income. c. With a price elasticity of demand of 0.4, reducin ...

... production is not a large enough proportion of the total farm product to have much impact on the price. As a result, price does not change (or changes by only a slight amount), while the output of Thai farmers declines, thus reducing their income. c. With a price elasticity of demand of 0.4, reducin ...

Stock Price Manipulation Detection Based on Mathematical Models

... their passive orders. These actions allow the manipulators to sell their stock at a price higher than usual. The effectiveness of manipulation detection depends on how much the information we have. We rely on using the price data that buyers and sellers sent to the market. The trade data can be clas ...

... their passive orders. These actions allow the manipulators to sell their stock at a price higher than usual. The effectiveness of manipulation detection depends on how much the information we have. We rely on using the price data that buyers and sellers sent to the market. The trade data can be clas ...

Profit Maximization, Perfect Competition (Version 2)

... we first have to lay out the assumptions of the model: A1. Price Taking A2. Product Homogeneity A3. Free Entry and Exit with infinitely many potential entrants A1 gives us the supply curve for each individual seller. A2 tells us that they are selling in the exact same market. Finally, A3 tells us th ...

... we first have to lay out the assumptions of the model: A1. Price Taking A2. Product Homogeneity A3. Free Entry and Exit with infinitely many potential entrants A1 gives us the supply curve for each individual seller. A2 tells us that they are selling in the exact same market. Finally, A3 tells us th ...

Volatility and Risk Management

... These typically are wholesale and retail distributors who make buy-sell transactions in the cash market as they move a commodity through the supply chain. They are in the business of providing what economists call time, place and form utility. They may move a commodity into a warehouse and store it ...

... These typically are wholesale and retail distributors who make buy-sell transactions in the cash market as they move a commodity through the supply chain. They are in the business of providing what economists call time, place and form utility. They may move a commodity into a warehouse and store it ...

Answer Key

... producers to produce more output at any price level. Without a decline in demand, this cost reduction would result in lower price and higher quantity. However, at the same time, demand reduces, meaning that at every price level, the quantity demanded becomes lower. This effect ...

... producers to produce more output at any price level. Without a decline in demand, this cost reduction would result in lower price and higher quantity. However, at the same time, demand reduces, meaning that at every price level, the quantity demanded becomes lower. This effect ...

What is Financial Mathematics? 1

... • Financial Mathematics has been established as a separate academic discipline only since the late eighties, with a number of dedicated journals. ...

... • Financial Mathematics has been established as a separate academic discipline only since the late eighties, with a number of dedicated journals. ...

Morgan Stanley Memorandum/Facsimile Template

... execution that is tied to a particular benchmark or price level, which is an unconditional contract, we may transact for our own account using similar means as described above. When we accept an order for execution on a guaranteed benchmark basis (for example, a guaranteed opening, closing, volume w ...

... execution that is tied to a particular benchmark or price level, which is an unconditional contract, we may transact for our own account using similar means as described above. When we accept an order for execution on a guaranteed benchmark basis (for example, a guaranteed opening, closing, volume w ...

Behavioral Idiosyncrasies and How They May Affect Investment

... may seem a small number, the study’s authors cautioned that their scope was limited, confined to market movements of only two-day periods. They speculated that many more occurrences would likely be found if other research examined longer time frames of 10, 100, or even more trading days. In other st ...

... may seem a small number, the study’s authors cautioned that their scope was limited, confined to market movements of only two-day periods. They speculated that many more occurrences would likely be found if other research examined longer time frames of 10, 100, or even more trading days. In other st ...

Multimarket Trading and Market Liquidity Author(s): Bhagwan

... fourth markets" in some stocks. Also, there often exist active markets in derivative securities, such as futures and options. An investor with private information about a stock could trade, for example, on one or more exchanges on which the stock is listed, while simultaneously trading in off-the-ex ...

... fourth markets" in some stocks. Also, there often exist active markets in derivative securities, such as futures and options. An investor with private information about a stock could trade, for example, on one or more exchanges on which the stock is listed, while simultaneously trading in off-the-ex ...

Stocks

... Used to compare corporate earnings to the market price of a corporation’s stock Key factor that serious investors as well as beginners can use to decide to invest in stock A low PE ratio indicates that a stock may be a good investment; the company has a lot of earnings compared to the price of ...

... Used to compare corporate earnings to the market price of a corporation’s stock Key factor that serious investors as well as beginners can use to decide to invest in stock A low PE ratio indicates that a stock may be a good investment; the company has a lot of earnings compared to the price of ...

Ban on short selling

... short selling under these provisions. Overthe-counter (OTC) transactions do fall within the scope of the prohibition, whereas credit default swaps do not. The AFM says that it does not impose restrictions on stock lending activities. At the same time, the AFM urges pension funds and other stock lend ...

... short selling under these provisions. Overthe-counter (OTC) transactions do fall within the scope of the prohibition, whereas credit default swaps do not. The AFM says that it does not impose restrictions on stock lending activities. At the same time, the AFM urges pension funds and other stock lend ...

Practice Questions

... A) APT stipulates B) CAPM stipulates C) Both CAPM and APT stipulate D) Neither CAPM nor APT stipulate E) No pricing model has found 2. The exploitation of security mispricing in such a way that risk-free economic profits may be earned is called ___________. A) arbitrage B) capital asset pricing C) f ...

... A) APT stipulates B) CAPM stipulates C) Both CAPM and APT stipulate D) Neither CAPM nor APT stipulate E) No pricing model has found 2. The exploitation of security mispricing in such a way that risk-free economic profits may be earned is called ___________. A) arbitrage B) capital asset pricing C) f ...

Download attachment

... The development of a yield curve on a wide range of actively traded debt securities will result in a benchmark security which market participants will use in setting up their trading, investment / lending and borrowing policies. The financial markets thrive on information. An efficient secondary mar ...

... The development of a yield curve on a wide range of actively traded debt securities will result in a benchmark security which market participants will use in setting up their trading, investment / lending and borrowing policies. The financial markets thrive on information. An efficient secondary mar ...

Title Is Times New Roman 28 Pt., Line Spacing .9 Lines

... Note: Core Inflation is a 5-year moving average; headline inflation prior to 1963. Past performance is not a guarantee of future results. For illustrative purposes only and does not reflect any specific product. The Standard & Poor’s 500 Index (S&P 500) is an unmanaged group of large company stocks. ...

... Note: Core Inflation is a 5-year moving average; headline inflation prior to 1963. Past performance is not a guarantee of future results. For illustrative purposes only and does not reflect any specific product. The Standard & Poor’s 500 Index (S&P 500) is an unmanaged group of large company stocks. ...

Chapter 02 Asset Classes and Financial Instruments

... C. carry a rate that is usually about one percentage point lower than the rate on U.S. T-bills. D. are funds used by individuals who wish to buy stocks on margin and are funds borrowed by the broker from the bank, with the agreement to repay the bank immediately if requested to ...

... C. carry a rate that is usually about one percentage point lower than the rate on U.S. T-bills. D. are funds used by individuals who wish to buy stocks on margin and are funds borrowed by the broker from the bank, with the agreement to repay the bank immediately if requested to ...

Stocks, Bonds, Options

... over a two-day period, when the Dow Jones Industrial Average fell 12.8% on October 28, 1929 and 11.7% on October ...

... over a two-day period, when the Dow Jones Industrial Average fell 12.8% on October 28, 1929 and 11.7% on October ...

The Rise and Fall of Trading Exchanges

... buyer more efficiently. It’s like a global e-marketplace. Wider implications can be seen in the reduction of geographical barriers that previously prevented buyers and sellers from interacting. In cyberspace there are no barriers. So information exchange is now as fast as it can be –- in principle. ...

... buyer more efficiently. It’s like a global e-marketplace. Wider implications can be seen in the reduction of geographical barriers that previously prevented buyers and sellers from interacting. In cyberspace there are no barriers. So information exchange is now as fast as it can be –- in principle. ...

Trading Fees and Slow-Moving Capital - Search Faculty

... stochastic process of the liquidity of securities is as important to investment and valuation as is the exogenous stochastic process of their future cash ‡ows. That is, when purchasing a security an investor needs not only have in mind the cash ‡ows that the security will pay into the inde…nite futu ...

... stochastic process of the liquidity of securities is as important to investment and valuation as is the exogenous stochastic process of their future cash ‡ows. That is, when purchasing a security an investor needs not only have in mind the cash ‡ows that the security will pay into the inde…nite futu ...

is the SEC adequately protecting the nation’s capital markets

... stress could amplify rather than mitigate the shock, induce larger moves in asset prices, or cause broader damage to the functioning of markets when it is most important they function well. Second is the possibility that the failure of a major hedge fund or group of funds could significantly damage ...

... stress could amplify rather than mitigate the shock, induce larger moves in asset prices, or cause broader damage to the functioning of markets when it is most important they function well. Second is the possibility that the failure of a major hedge fund or group of funds could significantly damage ...

Bulgarian Academy of Sciences Economic Research Institute

... listed companies and the fall of equity prices. • Bulgarian Stock Exchange became a public company in 2010, and the first transaction in securities was in January 2011. ...

... listed companies and the fall of equity prices. • Bulgarian Stock Exchange became a public company in 2010, and the first transaction in securities was in January 2011. ...

Stock Price - Brooklyn Public Library

... If stock currently trading at $7.69 Ex. If you place limit order to sell at $7.49;it will execute at price higher than $7.69 or higher Buy Stop: Order to buy stock above the current price Sell Stop: Order to sell stock at a price lower than current price Good Till Cancelled: A limit order that is op ...

... If stock currently trading at $7.69 Ex. If you place limit order to sell at $7.49;it will execute at price higher than $7.69 or higher Buy Stop: Order to buy stock above the current price Sell Stop: Order to sell stock at a price lower than current price Good Till Cancelled: A limit order that is op ...

The Round-the-Clock Market for US Treasury Securities

... market for Treasury securities. Customers include nonprimary dealers, other financial institutions (such as banks, insurance companies, pension funds, and mutual funds), nonfinancial institutions, and individuals. Although trading with customers is no longer a requirement, primary dealers remain the ...

... market for Treasury securities. Customers include nonprimary dealers, other financial institutions (such as banks, insurance companies, pension funds, and mutual funds), nonfinancial institutions, and individuals. Although trading with customers is no longer a requirement, primary dealers remain the ...

How to view electricity

... ST- Generation resource optimization and helps transfer power from surplus to deficit region in a geographically seasonally diverse country like India Is short term market a procurement market or a balancing market? Utilities to decided their own expectation of the market prices and demand projectio ...

... ST- Generation resource optimization and helps transfer power from surplus to deficit region in a geographically seasonally diverse country like India Is short term market a procurement market or a balancing market? Utilities to decided their own expectation of the market prices and demand projectio ...