Securities Trading Policy

... The risk of Insider Trading, or the appearance of Insider Trading, is considered low for certain types of Dealing in Suncorp Securities. The following types of “Exempt Dealing” are exempt from the restriction on Dealing during Closed Periods and the requirement to obtain clearance to Deal as set out ...

... The risk of Insider Trading, or the appearance of Insider Trading, is considered low for certain types of Dealing in Suncorp Securities. The following types of “Exempt Dealing” are exempt from the restriction on Dealing during Closed Periods and the requirement to obtain clearance to Deal as set out ...

Concentration risks in financial market infrastructures – the

... positions are closed out. Situation 1 on the left-hand side of the graph is a situation with two CCPs where the margin requirements for the CM are calculated independently. CM 1 has positions in products that are economically identical (perfect correlation of 1, in order to avoid complexities of cor ...

... positions are closed out. Situation 1 on the left-hand side of the graph is a situation with two CCPs where the margin requirements for the CM are calculated independently. CM 1 has positions in products that are economically identical (perfect correlation of 1, in order to avoid complexities of cor ...

Leveraged and Inverse ETFs(Slides)

... effects of compounding, so that their risk profiles differ significantly vis-à-vis traditional ETFs Investors should be aware that leveraged and inverse ETFs do not seek to provide returns which are the 2x multiple or -1x inverse of a given index for periods longer than a day. These funds are not s ...

... effects of compounding, so that their risk profiles differ significantly vis-à-vis traditional ETFs Investors should be aware that leveraged and inverse ETFs do not seek to provide returns which are the 2x multiple or -1x inverse of a given index for periods longer than a day. These funds are not s ...

Equity Diversification:

... and prefer that their portfolio not be more volatile than the overall market. In fact, there are investment managers who are more than willing to capitalize on investor nervousness by constructing portfolios with an eye toward limiting relative volatility. Equity portfolio volatility can be quantifi ...

... and prefer that their portfolio not be more volatile than the overall market. In fact, there are investment managers who are more than willing to capitalize on investor nervousness by constructing portfolios with an eye toward limiting relative volatility. Equity portfolio volatility can be quantifi ...

Securities and Secrets: Insider Trading and the Law of Contracts

... securities law.1" Yet, these commentators have not struggled with a definition of fairness, but have settled for general descriptions, such as "equal access to information' 7 between insiders and out14 See Brudney, supra note 2, at 335-36. It has been argued that if the harm from insider trading had ...

... securities law.1" Yet, these commentators have not struggled with a definition of fairness, but have settled for general descriptions, such as "equal access to information' 7 between insiders and out14 See Brudney, supra note 2, at 335-36. It has been argued that if the harm from insider trading had ...

Hedging with Interest-Rate Forward Contracts

... financial derivatives, have payoffs that are linked to previously issued securities and are extremely useful risk reduction tools. In this chapter, we look at the most important financial derivatives that managers of financial institutions use to reduce risk: forward contracts, financial futures, op ...

... financial derivatives, have payoffs that are linked to previously issued securities and are extremely useful risk reduction tools. In this chapter, we look at the most important financial derivatives that managers of financial institutions use to reduce risk: forward contracts, financial futures, op ...

The High-Volume Return Premium - North American Business Press

... Gallant, Rossi, and Tauchen (1992) recommended that study in joint dynamics of stock returns and trading volumes is more helpful rather than focusing only on the variation in stock prices. The investor recognition hypothesis is proposed by Merton (1987), which demonstrates that security price change ...

... Gallant, Rossi, and Tauchen (1992) recommended that study in joint dynamics of stock returns and trading volumes is more helpful rather than focusing only on the variation in stock prices. The investor recognition hypothesis is proposed by Merton (1987), which demonstrates that security price change ...

A Model of Intertemporal Asset Prices Under Asymmetric

... the reaction of uninformed investors. Informed investors take advantage of the errors made by less-informed investors to make profits. The uninformed investors trade based on information extracted from prices and dividends. We find that in some cases, the uninformed investors rationally adopt tradin ...

... the reaction of uninformed investors. Informed investors take advantage of the errors made by less-informed investors to make profits. The uninformed investors trade based on information extracted from prices and dividends. We find that in some cases, the uninformed investors rationally adopt tradin ...

preface - The Cheap Investor

... Almost everyone has heard the old adage, “Buy low and sell high”. Logically, that is the only way an investor will make money. The problem most investors have is they don’t think for themselves. Instead, they follow the herd. They get caught up in momentum buying, where they buy a stock that has hit ...

... Almost everyone has heard the old adage, “Buy low and sell high”. Logically, that is the only way an investor will make money. The problem most investors have is they don’t think for themselves. Instead, they follow the herd. They get caught up in momentum buying, where they buy a stock that has hit ...

Robust Median Reversion Strategy for On

... which often designs algorithms following the Kelly investment because of its sequential nature, and has been actively explored in AI [Cover, 1991; Ordentlich and Cover, 1996] and machine learning communities [Agarwal et al., 2006; Borodin et al., 2004; Li and Hoi, 2012]. Some state-of-the-art on-lin ...

... which often designs algorithms following the Kelly investment because of its sequential nature, and has been actively explored in AI [Cover, 1991; Ordentlich and Cover, 1996] and machine learning communities [Agarwal et al., 2006; Borodin et al., 2004; Li and Hoi, 2012]. Some state-of-the-art on-lin ...

capital market and reserch unit

... as against N417.57 million shares worth N3,246.56 billion in 5,456 deals carried Friday. Topping in volume terms, United Bank for Africa Plc, Wema Bank Plc and Transnational Corporation of Nigeria Plc while Guaranty Trust Bank Plc and United Bank for Africa Plc ended trading as the most active stock ...

... as against N417.57 million shares worth N3,246.56 billion in 5,456 deals carried Friday. Topping in volume terms, United Bank for Africa Plc, Wema Bank Plc and Transnational Corporation of Nigeria Plc while Guaranty Trust Bank Plc and United Bank for Africa Plc ended trading as the most active stock ...

Adverse Selection and Competitive Market Making

... A market for a security is liquid if investors can buy or sell large amounts of the security at a low transaction cost. Liquidity is a valuable characteristic of a security because it allows investors to realize more of the gains from optimal risk sharing through dynamic trading.1 In many markets l ...

... A market for a security is liquid if investors can buy or sell large amounts of the security at a low transaction cost. Liquidity is a valuable characteristic of a security because it allows investors to realize more of the gains from optimal risk sharing through dynamic trading.1 In many markets l ...

Two Agency-Cost Explanations of Dividends

... o prosperous firms often withhold dividends because internal financing is cheaper than issuing dividends and floating new securities o however, dividends do not distinguish well-managed firms from others they are not irrational for poorly-managed or failing firms such firms should disinvest or l ...

... o prosperous firms often withhold dividends because internal financing is cheaper than issuing dividends and floating new securities o however, dividends do not distinguish well-managed firms from others they are not irrational for poorly-managed or failing firms such firms should disinvest or l ...

Information Disclosure in Speculative Markets

... the highest willingness to pay among the different investors – investors who think the asset is worth less cannot “make their voices heard” by way of short selling the asset, and thus are effectively crowded out of the market. Second, at any point in time, the price of the asset typically exceeds t ...

... the highest willingness to pay among the different investors – investors who think the asset is worth less cannot “make their voices heard” by way of short selling the asset, and thus are effectively crowded out of the market. Second, at any point in time, the price of the asset typically exceeds t ...

To Our Shareholders Notice of Convocation of the 10th Ordinary

... As a result of the above, net sales totaled 1,955,027 thousand yen for the fiscal year ended December 31, 2014, primarily reflecting product sales of SyB L-0501 in Japan and overseas markets. Net domestic sales of TREAKISYM® showed a year-on-year increase of 12.9%. While net overseas sales increased ...

... As a result of the above, net sales totaled 1,955,027 thousand yen for the fiscal year ended December 31, 2014, primarily reflecting product sales of SyB L-0501 in Japan and overseas markets. Net domestic sales of TREAKISYM® showed a year-on-year increase of 12.9%. While net overseas sales increased ...

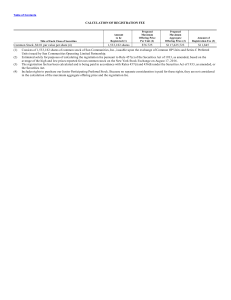

CALCULATION OF REGISTRATION FEE Common - corporate

... You should read this prospectus supplement, the accompanying prospectus and the additional information described under the headings “Where You Can Find More Information” and “Incorporation of Certain Documents by Reference” before you make a decision to invest in the shares of common stock being off ...

... You should read this prospectus supplement, the accompanying prospectus and the additional information described under the headings “Where You Can Find More Information” and “Incorporation of Certain Documents by Reference” before you make a decision to invest in the shares of common stock being off ...

Publication - Oxford Institute for Energy Studies

... delivery of the commodity”. The yield may not necessarily be a pecuniary return. It can be an implicit and indirectly measurable return that holders place on their ability to use inventories to meet contractual obligations, to minimise transformation costs, to prevent interruption of supplies to lon ...

... delivery of the commodity”. The yield may not necessarily be a pecuniary return. It can be an implicit and indirectly measurable return that holders place on their ability to use inventories to meet contractual obligations, to minimise transformation costs, to prevent interruption of supplies to lon ...

BARCLAYS BANK PLC (Form: 424B2, Received: 12/30

... and not to its consolidated subsidiaries. In this document, “Securities” refers to the Trigger Performance Securities linked to the S&P 500 ® Index that are offered hereby, unless the context otherwise requires. Additional Information Regarding Our Estimated Value of the Securities Our internal pric ...

... and not to its consolidated subsidiaries. In this document, “Securities” refers to the Trigger Performance Securities linked to the S&P 500 ® Index that are offered hereby, unless the context otherwise requires. Additional Information Regarding Our Estimated Value of the Securities Our internal pric ...

IIIS Discussion Paper No. 304

... Corresponding author: E-mail: [email protected] See section 2.2 for relevant literature. ...

... Corresponding author: E-mail: [email protected] See section 2.2 for relevant literature. ...

Jubilant LifesciencesJULS.NS JOL IN

... JOL started domestic formulation sales in FY15, with a field force of 200+. We are not factoring in any material upside from the business at this stage. We expect the business to take more than three years to scale up. Lifescience ingredients- Pricing assumed stable at current levels; assume increas ...

... JOL started domestic formulation sales in FY15, with a field force of 200+. We are not factoring in any material upside from the business at this stage. We expect the business to take more than three years to scale up. Lifescience ingredients- Pricing assumed stable at current levels; assume increas ...

Dividend Portfolio Strategy

... Favorable tax treatment recently has hedged dividend returns. For most of the last 80 years, dividends have been taxed at the individual marginal income tax rate. * ...

... Favorable tax treatment recently has hedged dividend returns. For most of the last 80 years, dividends have been taxed at the individual marginal income tax rate. * ...

Short (finance)

.png?width=300)

In finance, short selling (also known as shorting or going short) is the practice of selling securities or other financial instruments that are not currently owned, and subsequently repurchasing them (""covering""). In the event of an interim price decline, the short seller will profit, since the cost of (re)purchase will be less than the proceeds which were received upon the initial (short) sale. Conversely, the short position will be closed out at a loss in the event that the price of a shorted instrument should rise prior to repurchase. The potential loss on a short sale is theoretically unlimited in the event of an unlimited rise in the price of the instrument, however in practice the short seller will be required to post margin or collateral to cover losses, and any inability to do so on a timely basis would cause its broker or counterparty to liquidate the position. In the securities markets, the seller generally must borrow the securities in order to effect delivery in the short sale. In some cases, the short seller must pay a fee to borrow the securities and must additionally reimburse the lender for cash returns the lender would have received had the securities not been loaned out.Short selling is most commonly done with instruments traded in public securities, futures or currency markets, due to the liquidity and real-time price dissemination characteristic of such markets and because the instruments defined within each class are fungible.In practical terms, going short can be considered the opposite of the conventional practice of ""going long"", whereby an investor profits from an increase in the price of the asset. Mathematically, the return from a short position is equivalent to that of owning (being ""long"") a negative amount of the instrument. A short sale may be motivated by a variety of objectives. Speculators may sell short in the hope of realizing a profit on an instrument which appears to be overvalued, just as long investors or speculators hope to profit from a rise in the price of an instrument which appears undervalued. Traders or fund managers may hedge a long position or a portfolio through one or more short positions.