Muni Bonds: Off to a Good Start in 2017

... What will happen with interest rates? As we have highlighted many times, accurately predicting the direction of interest rates historically has been very dif f icult to do. Many have anticipated higher rates f or most of the past eight years, only to be disappointed thus f ar. Yes, it would seem r ...

... What will happen with interest rates? As we have highlighted many times, accurately predicting the direction of interest rates historically has been very dif f icult to do. Many have anticipated higher rates f or most of the past eight years, only to be disappointed thus f ar. Yes, it would seem r ...

![[Presentation Subject]](http://s1.studyres.com/store/data/004542315_1-1026bbe0061976fe5bee402d431f0480-300x300.png)

[Presentation Subject]

... and are not intended as a solicitation with respect to the purchase or sale of any instrument. The information contained in this presentation may include results of analyses from a quantitative model which represent potential future events that may or may not be realized, and is not a complete analy ...

... and are not intended as a solicitation with respect to the purchase or sale of any instrument. The information contained in this presentation may include results of analyses from a quantitative model which represent potential future events that may or may not be realized, and is not a complete analy ...

Chapter 5

... modeling default: default occurs when the market value of assets fall below debt value • Reduced form models: Decompose risky debt prices to estimate the stochastic default intensity function. No structural explanation of why default occurs. ...

... modeling default: default occurs when the market value of assets fall below debt value • Reduced form models: Decompose risky debt prices to estimate the stochastic default intensity function. No structural explanation of why default occurs. ...

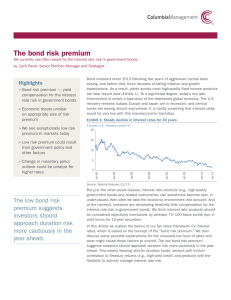

The bond risk premium

... The ex-post bond risk premium is simply the historical excess return of longterm bonds over bills. This calculation is straightforward, but estimates of excess returns vary because of different sample periods and the specific securities considered. For the best estimates we want to consider long sam ...

... The ex-post bond risk premium is simply the historical excess return of longterm bonds over bills. This calculation is straightforward, but estimates of excess returns vary because of different sample periods and the specific securities considered. For the best estimates we want to consider long sam ...

Triennial Review of VRR Curve Shape

... (2) Relative to a vertical demand curve, the downward‐slope of the current VRR curve is consistent with its design objectives: prices above net CONE when the system is short resources (capacity less than IRM), prices below net CONE when the system is long (capacity greater than IRM), and working ...

... (2) Relative to a vertical demand curve, the downward‐slope of the current VRR curve is consistent with its design objectives: prices above net CONE when the system is short resources (capacity less than IRM), prices below net CONE when the system is long (capacity greater than IRM), and working ...

ADD-ON 9B - Ateneonline

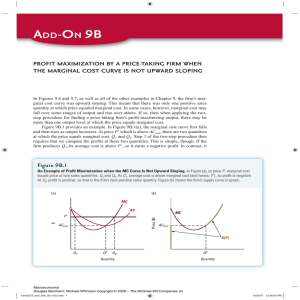

... In Figures 9.6 and 9.7, as well as all of the other examples in Chapter 9, the firm’s marginal cost curve was upward sloping. This meant that there was only one positive sales quantity at which price equaled marginal cost. In some cases, however, marginal cost may fall over some ranges of output and ...

... In Figures 9.6 and 9.7, as well as all of the other examples in Chapter 9, the firm’s marginal cost curve was upward sloping. This meant that there was only one positive sales quantity at which price equaled marginal cost. In some cases, however, marginal cost may fall over some ranges of output and ...

A Primer on Bonds Bond Prices and Yields

... Therefore, the bond sells for 0.4071 times Par, and Market value = Par value x 0.4071 => $5.8 million = Par value x 0.4071 => Par value = $14.25 million. Another way to see this is to note that each bond with a par value of $1,000 sells for $407.11. If the total market value is $5.8 million, then yo ...

... Therefore, the bond sells for 0.4071 times Par, and Market value = Par value x 0.4071 => $5.8 million = Par value x 0.4071 => Par value = $14.25 million. Another way to see this is to note that each bond with a par value of $1,000 sells for $407.11. If the total market value is $5.8 million, then yo ...

Hedging with Interest Rate Futures

... Liquidity breeds liquidity • Euribor Futures Contract STIR Liquidity ...

... Liquidity breeds liquidity • Euribor Futures Contract STIR Liquidity ...

StrongPCMP4e-ch11

... inflation premium theory states that risk comes from the uncertainty associated with future inflation rates Investors who commit funds for long periods are bearing more purchasing power risk than short-term investors • More inflation risk means longer-term investment will carry a higher yield ...

... inflation premium theory states that risk comes from the uncertainty associated with future inflation rates Investors who commit funds for long periods are bearing more purchasing power risk than short-term investors • More inflation risk means longer-term investment will carry a higher yield ...

Outline

... Domestic Equities vs Domestic Bonds (Stock-Bonds) Domestic Bonds vs Cash (Bonds-Cash) Assume Asset Limits of +/- 5% from Benchmark Weight ...

... Domestic Equities vs Domestic Bonds (Stock-Bonds) Domestic Bonds vs Cash (Bonds-Cash) Assume Asset Limits of +/- 5% from Benchmark Weight ...

Bonds

... that US Savings Bonds are the single most widely held security in the world and that over 55 million Americans own them. Over the last 60 years, posters have helped to promote the sale of savings bonds. Instruct students to refer to the website ...

... that US Savings Bonds are the single most widely held security in the world and that over 55 million Americans own them. Over the last 60 years, posters have helped to promote the sale of savings bonds. Instruct students to refer to the website ...

Chapter 11 Practice Exam Solutions

... D is the before-tax demand curve for labour, S is the before-tax supply curve and w1 is the before-tax equilibrium wage rate. The employer tax shifts the effective demand curve downwards to D′. The employee tax shifts the effective supply curve upwards by the amount of the tax to S′, which coincides ...

... D is the before-tax demand curve for labour, S is the before-tax supply curve and w1 is the before-tax equilibrium wage rate. The employer tax shifts the effective demand curve downwards to D′. The employee tax shifts the effective supply curve upwards by the amount of the tax to S′, which coincides ...

Slide 1

... -LEFTWARD SHIFTS OF THE SHORT RUN AGGREGATE SUPPLY CURVE MAKE A DIFFERENCE. THE PHILLIPS CURVE TRADEOFF IS DERIVED FROM SHIFTING THE AGGREGATE DEMAND CURVE ALONG A STABLE SHORT RUN AGGREGATE SUPPLY CURVE -THE “GREAT STAGFLATION” OF THE 1970s MADE IT CLEAR THAT THE PHILLIPS CURVE DID NOT REPRESENT A ...

... -LEFTWARD SHIFTS OF THE SHORT RUN AGGREGATE SUPPLY CURVE MAKE A DIFFERENCE. THE PHILLIPS CURVE TRADEOFF IS DERIVED FROM SHIFTING THE AGGREGATE DEMAND CURVE ALONG A STABLE SHORT RUN AGGREGATE SUPPLY CURVE -THE “GREAT STAGFLATION” OF THE 1970s MADE IT CLEAR THAT THE PHILLIPS CURVE DID NOT REPRESENT A ...

cm24e perfect competition

... setters" or "price seekers".) This raises a problem as to who, or what, determines the price in a pure market system. (4) There is complete freedom of entry and exit into the industry – firms can move into or out of the industry at will; there are no barriers to entry as there are under monopoly, m ...

... setters" or "price seekers".) This raises a problem as to who, or what, determines the price in a pure market system. (4) There is complete freedom of entry and exit into the industry – firms can move into or out of the industry at will; there are no barriers to entry as there are under monopoly, m ...

The Term Structure of Interest Rates

... • John Moody began the modern bond rating business by publishing Moody’s Analyses of Railroad Investments in 1909. • By the 1920s, the work of rating agencies expanded to cover an increasing number of industries. • In the post-World War II period, prosperity diminished the role of rating agencies, b ...

... • John Moody began the modern bond rating business by publishing Moody’s Analyses of Railroad Investments in 1909. • By the 1920s, the work of rating agencies expanded to cover an increasing number of industries. • In the post-World War II period, prosperity diminished the role of rating agencies, b ...

Financial Markets

... A market for short-term instruments such as T-bills, commercial paper, banker’s acceptance, etc A subsector of fixed-income securities Money market instruments are highly marketable, offer low-return, posses low-risk Trade in large denominations, so are out of the reach of small investors ...

... A market for short-term instruments such as T-bills, commercial paper, banker’s acceptance, etc A subsector of fixed-income securities Money market instruments are highly marketable, offer low-return, posses low-risk Trade in large denominations, so are out of the reach of small investors ...

Are higher global interest rates a thing of the past

... rise. Increases in prices and the rate of inflation often lead to interest rate rises. Inflation can result from increasing supply costs. Supply costs may rise due to increases in wages. In the UK for example wage inflation has been kept low due to reform of trade union power and both in Europe and ...

... rise. Increases in prices and the rate of inflation often lead to interest rate rises. Inflation can result from increasing supply costs. Supply costs may rise due to increases in wages. In the UK for example wage inflation has been kept low due to reform of trade union power and both in Europe and ...

Answers to Chapter 23 Questions

... options markets, thereby affording the FI greater liquidity. This may be a result of the regulatory environment. Financial futures options are regulated by the CFTC while cash market options are regulated by the SEC. To the extent that the CFTC is perceived by FIs to be less strict than its SEC coun ...

... options markets, thereby affording the FI greater liquidity. This may be a result of the regulatory environment. Financial futures options are regulated by the CFTC while cash market options are regulated by the SEC. To the extent that the CFTC is perceived by FIs to be less strict than its SEC coun ...

Yield curve

In finance, the yield curve is a curve showing several yields or interest rates across different contract lengths (2 month, 2 year, 20 year, etc...) for a similar debt contract. The curve shows the relation between the (level of) interest rate (or cost of borrowing) and the time to maturity, known as the ""term"", of the debt for a given borrower in a given currency. For example, the U.S. dollar interest rates paid on U.S. Treasury securities for various maturities are closely watched by many traders, and are commonly plotted on a graph such as the one on the right which is informally called ""the yield curve"". More formal mathematical descriptions of this relation are often called the term structure of interest rates.The shape of the yield curve indicates the cumulative priorities of all lenders relative to a particular borrower, (such as the US Treasury or the Treasury of Japan) or the priorities of a single lender relative to all possible borrowers. With other factors held equal, lenders will prefer to have funds at their disposal, rather than at the disposal of a third party. The interest rate is the ""price"" paid to convince them to lend. As the term of the loan increases, lenders demand an increase in the interest received. In addition, lenders may be concerned about future circumstances, e.g. a potential default (or rising rates of inflation), so they offer higher interest rates on long-term loans than they offer on shorter-term loans to compensate for the increased risk. Occasionally, when lenders are seeking long-term debt contracts more aggressively than short-term debt contracts, the yield curve ""inverts"", with interest rates (yields) being lower for the longer periods of repayment so that lenders can attract long-term borrowing.The yield of a debt instrument is the overall rate of return available on the investment. In general the percentage per year that can be earned is dependent on the length of time that the money is invested. For example, a bank may offer a ""savings rate"" higher than the normal checking account rate if the customer is prepared to leave money untouched for five years. Investing for a period of time t gives a yield Y(t).This function Y is called the yield curve, and it is often, but not always, an increasing function of t. Yield curves are used by fixed income analysts, who analyze bonds and related securities, to understand conditions in financial markets and to seek trading opportunities. Economists use the curves to understand economic conditions.The yield curve function Y is actually only known with certainty for a few specific maturity dates, while the other maturities are calculated by interpolation (see Construction of the full yield curve from market data below).