Wholesale Market - Danish Energy Association

... 2. Market-based procurement of non-frequency ancillary services2 Non-frequency ancillary services – reactive power, inertia, black-start capability – become increasingly scarce as power station capacity is reduced. There is a need to find ways to endure continued provision of these services. The EC ...

... 2. Market-based procurement of non-frequency ancillary services2 Non-frequency ancillary services – reactive power, inertia, black-start capability – become increasingly scarce as power station capacity is reduced. There is a need to find ways to endure continued provision of these services. The EC ...

International financial and foreign exchange markets Tentative

... FX market efficiency and the art of exchange rate forecasting (A. Ziliotto) Theoretical overview and available empirical evidence: could there be profitable trading strategies? Textbook chapter: XVI The infrastructure of international finance: historical evolution and current situation (G. Schlitzer ...

... FX market efficiency and the art of exchange rate forecasting (A. Ziliotto) Theoretical overview and available empirical evidence: could there be profitable trading strategies? Textbook chapter: XVI The infrastructure of international finance: historical evolution and current situation (G. Schlitzer ...

The incumbent presentation shall attempt to delineate

... Given the above, our understanding is that we have to view the issue of collective behaviour from an alternative point. Let us assume, for a moment, that an investor trades to the direction of past prices (i.e. buys when prices go up and sells when they go down). By definition, this investor will ad ...

... Given the above, our understanding is that we have to view the issue of collective behaviour from an alternative point. Let us assume, for a moment, that an investor trades to the direction of past prices (i.e. buys when prices go up and sells when they go down). By definition, this investor will ad ...

Problem Set 5

... Calculate the optimal economic dispatch. Show that the solution satisfies the necessary and sufficient conditions for optimality. 4. Peak and off-peak pricing and planning problems are common place for firms with capacity constrained production processes. Usually the firm has invested in capacity i ...

... Calculate the optimal economic dispatch. Show that the solution satisfies the necessary and sufficient conditions for optimality. 4. Peak and off-peak pricing and planning problems are common place for firms with capacity constrained production processes. Usually the firm has invested in capacity i ...

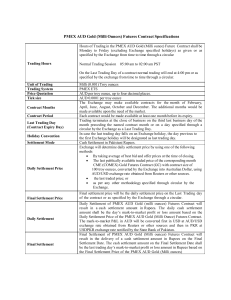

PMEX AUD Gold Futures Contract

... Final settlement price will be the daily settlement price on the Last Trading day of the contract or as specified by the Exchange through a circular. Daily Settlement of PMEX AUD Gold (milli ounces) Futures Contract will result in a cash settlement amount in Rupees. The daily cash settlement amount ...

... Final settlement price will be the daily settlement price on the Last Trading day of the contract or as specified by the Exchange through a circular. Daily Settlement of PMEX AUD Gold (milli ounces) Futures Contract will result in a cash settlement amount in Rupees. The daily cash settlement amount ...

ppt

... Cross-listing shares on more than one stock exchange can increase demand and enhance share price U.S. companies listing abroad experience less of an adverse price reaction than similar companies issuing equity in the United States Non-U.S. companies listing in the United States often increase in ...

... Cross-listing shares on more than one stock exchange can increase demand and enhance share price U.S. companies listing abroad experience less of an adverse price reaction than similar companies issuing equity in the United States Non-U.S. companies listing in the United States often increase in ...

Circular 2013/8 Market conduct rules Supervisory rules on

... Nostro-nostro in-house crosses where equal and opposite trades are matched in the stock exchange system independently of one another and without any previous agreement. ...

... Nostro-nostro in-house crosses where equal and opposite trades are matched in the stock exchange system independently of one another and without any previous agreement. ...

Market Trading in India - Customer Perception

... commodity. It is a contract to make or take delivery of a product in the future, at a price set in the present. In formalized trading of futures contracts on exchanges, agreements specify price, quantity and the month of delivery. Futures can be used either to hedge or to speculate on the price move ...

... commodity. It is a contract to make or take delivery of a product in the future, at a price set in the present. In formalized trading of futures contracts on exchanges, agreements specify price, quantity and the month of delivery. Futures can be used either to hedge or to speculate on the price move ...

MAD Regulation in the UK The Impact of EU Law on the Regulation

... » true insiders, or » those who “could reasonably be expected to know” that it is inside information – Specific /precise / price sensitivity – No need to prove » knowledge of significance of information – but dealing must be “on the basis of” the information » intention to profit • Market manipulati ...

... » true insiders, or » those who “could reasonably be expected to know” that it is inside information – Specific /precise / price sensitivity – No need to prove » knowledge of significance of information – but dealing must be “on the basis of” the information » intention to profit • Market manipulati ...

Exam March 13, 2015

... -i- (0.7 pt.) The fair price of the option. -ii- (0.7 pt.) The hedging strategy for the seller. -iii- (0.7 pt.) The optimal exercise times for the buyer. (d) (0.5 pt.) One of the criteria to decide which option is more convenient is to compare the expected net market payoff for each option. That is, ...

... -i- (0.7 pt.) The fair price of the option. -ii- (0.7 pt.) The hedging strategy for the seller. -iii- (0.7 pt.) The optimal exercise times for the buyer. (d) (0.5 pt.) One of the criteria to decide which option is more convenient is to compare the expected net market payoff for each option. That is, ...

2010 Flash Crash

The May 6, 2010, Flash Crash also known as The Crash of 2:45, the 2010 Flash Crash or simply the Flash Crash, was a United States trillion-dollar stock market crash, which started at 2:32 and lasted for approximately 36 minutes. Stock indexes, such as the S&P 500, Dow Jones Industrial Average and Nasdaq 100, collapsed and rebounded very rapidly.The Dow Jones Industrial Average had its biggest intraday point drop (from the opening) up to that point, plunging 998.5 points (about 9%), most within minutes, only to recover a large part of the loss. It was also the second-largest intraday point swing (difference between intraday high and intraday low) up to that point, at 1,010.14 points. The prices of stocks, stock index futures, options and ETFs were volatile, thus trading volume spiked. A CFTC 2014 report described it as one of the most turbulent periods in the history of financial markets.On April 21, 2015, nearly five years after the incident, the U.S. Department of Justice laid ""22 criminal counts, including fraud and market manipulation"" against Navinder Singh Sarao, a trader. Among the charges included was the use of spoofing algorithms; just prior to the Flash Crash, he placed thousands of E-mini S&P 500 stock index futures contracts which he planned on canceling later. These orders amounting to about ""$200 million worth of bets that the market would fall"" were ""replaced or modified 19,000 times"" before they were canceled. Spoofing, layering and front-running are now banned.The Commodity Futures Trading Commission (CFTC) investigation concluded that Sarao ""was at least significantly responsible for the order imbalances"" in the derivatives market which affected stock markets and exacerbated the flash crash. Sarao began his alleged market manipulation in 2009 with commercially available trading software whose code he modified ""so he could rapidly place and cancel orders automatically."" Traders Magazine journalist, John Bates, argued that blaming a 36-year-old small-time trader who worked from his parents' modest stucco house in suburban west London for sparking a trillion-dollar stock market crash is a little bit like blaming lightning for starting a fire"" and that the investigation was lengthened because regulators used ""bicycles to try and catch Ferraris."" Furthermore, he concluded that by April 2015, traders can still manipulate and impact markets in spite of regulators and banks' new, improved monitoring of automated trade systems.As recently as May 2014, a CFTC report concluded that high-frequency traders ""did not cause the Flash Crash, but contributed to it by demanding immediacy ahead of other market participants.""Recent research shows that Flash Crashes are not isolated occurrences, but have occurred quite often over the past century. For instance, Irene Aldridge, the author of High-Frequency Trading: A Practical Guide to Algorithmic Strategies and Trading Systems, 2nd ed., Wiley & Sons, shows that Flash Crashes have been frequent and their causes predictable in market microstructure analysis.