8: The Black-Scholes Model - School of Mathematics and Statistics

... are increasing functions of the volatility parameter σ (if all other quantities are fixed). Hence the options become more expensive when the underlying stock becomes more risky. The price of a call (put) option is an increasing (decreasing) function of the interest rate r . 8: The Black-Scholes Mode ...

... are increasing functions of the volatility parameter σ (if all other quantities are fixed). Hence the options become more expensive when the underlying stock becomes more risky. The price of a call (put) option is an increasing (decreasing) function of the interest rate r . 8: The Black-Scholes Mode ...

Slides

... Crisis (Enron, Worldcom) push new regulations (observability of derivatives) which was the first reason to push an index tranche market and base correlation ...

... Crisis (Enron, Worldcom) push new regulations (observability of derivatives) which was the first reason to push an index tranche market and base correlation ...

Trading Corner - Eurex Exchange

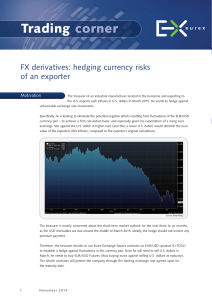

... a rate of 1.2770 compared to EUR 7,407,407.41 at a rate of 1.3500). At the same time, the futures contracts have generated a profit of USD 7,300 per contract – a total of USD 569,400 or EUR 421,777.78 at the prevailing market level. This profit virtually neutralizes the loss incurred on the underlyi ...

... a rate of 1.2770 compared to EUR 7,407,407.41 at a rate of 1.3500). At the same time, the futures contracts have generated a profit of USD 7,300 per contract – a total of USD 569,400 or EUR 421,777.78 at the prevailing market level. This profit virtually neutralizes the loss incurred on the underlyi ...

Investor Relations Communications Plan

... In Nasdaq Online, there are 13 possible styles, defined below, by which institutional investors are classified by the source of the data, the Carson Group. The Carson Group employs quantitative techniques based on key financial fundamentals of an investor's portfolio: primarily, the portions of the ...

... In Nasdaq Online, there are 13 possible styles, defined below, by which institutional investors are classified by the source of the data, the Carson Group. The Carson Group employs quantitative techniques based on key financial fundamentals of an investor's portfolio: primarily, the portions of the ...

the effect of exchange rate volatility on share price

... lagged squared residual terms, and on past values of itself, which are capture by lagged ht terms. If p=q=1 the model is GARCH(1,1) and Bollerslev (1986) noted that this specification usually performs very well and is easy to estimate. He also noted that the GARCH(1,1) model is equivalent to an infi ...

... lagged squared residual terms, and on past values of itself, which are capture by lagged ht terms. If p=q=1 the model is GARCH(1,1) and Bollerslev (1986) noted that this specification usually performs very well and is easy to estimate. He also noted that the GARCH(1,1) model is equivalent to an infi ...

高盛汉英词典 - 深圳市均达会计师事务所

... A latin term that translates into "for the sake of form." In the investing world, the term describes a method of calculating financial results in order to emphasize either current or projected figures. ...

... A latin term that translates into "for the sake of form." In the investing world, the term describes a method of calculating financial results in order to emphasize either current or projected figures. ...

Investor Expectations and the Volatility Puzzle in the Japanese

... where, VolaEq is the stock price volatility of stock i, MVi is its market capitalization, B/P is the book to price ratio, SDi,j is a dummy variable for industrial sector j, and the weight of each observation is set to 1. Table 4 Panel B reports the descriptive statistics for quintile portfolios base ...

... where, VolaEq is the stock price volatility of stock i, MVi is its market capitalization, B/P is the book to price ratio, SDi,j is a dummy variable for industrial sector j, and the weight of each observation is set to 1. Table 4 Panel B reports the descriptive statistics for quintile portfolios base ...

- Covenant University Repository

... the net present value of the future dividends. The models rely on mathematics rather than price observation, and specify an asset's intrinsic value, supplying a point estimate of value that can be compared with market price. Present value models of common stock (also called discounted cash flow mode ...

... the net present value of the future dividends. The models rely on mathematics rather than price observation, and specify an asset's intrinsic value, supplying a point estimate of value that can be compared with market price. Present value models of common stock (also called discounted cash flow mode ...

Economics Principles and Applications

... back the money plus interest in a year. Mike wants to charge a real return of 3%. Meanwhile, Mike expects the inflation rate to be 3% for the next year and Joe expects it to be 5%. So, Joe happily agrees to pay Mike 6% nominal interest rate. If the actual inflation rate is 4%, how will the purchasin ...

... back the money plus interest in a year. Mike wants to charge a real return of 3%. Meanwhile, Mike expects the inflation rate to be 3% for the next year and Joe expects it to be 5%. So, Joe happily agrees to pay Mike 6% nominal interest rate. If the actual inflation rate is 4%, how will the purchasin ...

K - Binus Repository

... Two approaches have developed 1. Discounted cash-flow valuation • Present value of some measure of cash flow, including dividends, operating cash flow, and free cash flow ...

... Two approaches have developed 1. Discounted cash-flow valuation • Present value of some measure of cash flow, including dividends, operating cash flow, and free cash flow ...

Option Pricing Theory and Applications

... The market value solution: When the subsidiaries are publicly traded, you could use their traded market capitalizations to estimate the values of the cross holdings. You do risk carrying into your valuation any mistakes that the market may be making in valuation. The relative value solution: When th ...

... The market value solution: When the subsidiaries are publicly traded, you could use their traded market capitalizations to estimate the values of the cross holdings. You do risk carrying into your valuation any mistakes that the market may be making in valuation. The relative value solution: When th ...

6) The Capital Asset Pricing Model

... investors have identical beliefs regarding the probability distribution of asset returns, that all risky assets can be traded, that there are no indivisibilities in asset holdings, and that there are no limits on borrowing or lending at the riskfree rate. We can now define an equilibrium as a situa ...

... investors have identical beliefs regarding the probability distribution of asset returns, that all risky assets can be traded, that there are no indivisibilities in asset holdings, and that there are no limits on borrowing or lending at the riskfree rate. We can now define an equilibrium as a situa ...

Financial Management

... process for valuation of any asset remains the same, However investment strategy differs in some ways. 1. Managerial finance It is the branch of finance that concerns itself with the managerial significance of financial techniques. It is focused on assessment rather than techniques. Why! because it ...

... process for valuation of any asset remains the same, However investment strategy differs in some ways. 1. Managerial finance It is the branch of finance that concerns itself with the managerial significance of financial techniques. It is focused on assessment rather than techniques. Why! because it ...

File

... of the risk free rate Lower levels of risk aversion lead to larger proportions of the portfolio of risky assets Willingness to accept high levels of risk for high levels of returns would result in leveraged combinations ...

... of the risk free rate Lower levels of risk aversion lead to larger proportions of the portfolio of risky assets Willingness to accept high levels of risk for high levels of returns would result in leveraged combinations ...

Derivatives pricing when one cannot borrow at the risk free rate

... pricing the uncollateralised position by replicating with the collateralised version. Note that our replicating portfolio should match all cashflows, including those occurring if the bank defaults. • Consider the situation where we have sold an uncollateralised option to a client, and then bought a ...

... pricing the uncollateralised position by replicating with the collateralised version. Note that our replicating portfolio should match all cashflows, including those occurring if the bank defaults. • Consider the situation where we have sold an uncollateralised option to a client, and then bought a ...