Job Type Description – Template

... Develop market risk assumptions to be applied in the firm-wide stress tests; provide guidelines for all businesses to follow; and check the business submitted results to ensure reasonableness. Expand the firm-wide stress testing to cover F/X and commodity risks in the future. Work with Risk An ...

... Develop market risk assumptions to be applied in the firm-wide stress tests; provide guidelines for all businesses to follow; and check the business submitted results to ensure reasonableness. Expand the firm-wide stress testing to cover F/X and commodity risks in the future. Work with Risk An ...

Some comments/observations: Borrower behaviour, mortgage terminations and the price of residential mortgages”

... “We need to know a lot more about the differences among borrowers” Especially their wealth compositions due to potential for differential effects on current and future consumption “Changes in house prices have a larger and more important impact on consumption than do changes in stock market pr ...

... “We need to know a lot more about the differences among borrowers” Especially their wealth compositions due to potential for differential effects on current and future consumption “Changes in house prices have a larger and more important impact on consumption than do changes in stock market pr ...

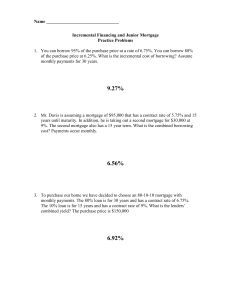

Adjustable Rate Mortgage

... is offering the property at 5.5% amortized over 15 years assuming a down payment of 20% is included up front. A balloon payment will be required in 5 years. Assuming you go to the bank and take out a mortgage with the same terms (except the banks interest rate is 7%), what should you be willing to p ...

... is offering the property at 5.5% amortized over 15 years assuming a down payment of 20% is included up front. A balloon payment will be required in 5 years. Assuming you go to the bank and take out a mortgage with the same terms (except the banks interest rate is 7%), what should you be willing to p ...

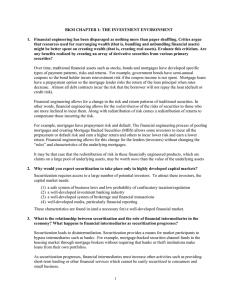

CHAPTER 1 : THE INVESTMENT ENVIRONMENT

... bond. The extra 25 basis points (0.25%) liquidity premium required by the investor is a cost born by the company issuing the bond (borrowing the money) in the form of higher coupon payments. Shares of a company’s stock entitle the investor to percentage of the earnings - either paid as dividends or ...

... bond. The extra 25 basis points (0.25%) liquidity premium required by the investor is a cost born by the company issuing the bond (borrowing the money) in the form of higher coupon payments. Shares of a company’s stock entitle the investor to percentage of the earnings - either paid as dividends or ...

Cybersecurity Risk Preparedness: Practical Steps for Financial

... are engaged in targeted examinations of cyber-security efforts. The New York Department of Financial Services has declared that it will be scrutinizing cybersecurity as an integral part of its bank examinations. Other regulators too are closely examining the depth and comprehensiveness of financial ...

... are engaged in targeted examinations of cyber-security efforts. The New York Department of Financial Services has declared that it will be scrutinizing cybersecurity as an integral part of its bank examinations. Other regulators too are closely examining the depth and comprehensiveness of financial ...

USCrisis

... investment banks collapse from losses AIG becomes unable to pay for all its “insured” defaulting bonds With a banking system in shock and hemorrhaging money, the credit system freezes Without credit available many companies and banks are faced with severe cash flow shortages leading to increasing la ...

... investment banks collapse from losses AIG becomes unable to pay for all its “insured” defaulting bonds With a banking system in shock and hemorrhaging money, the credit system freezes Without credit available many companies and banks are faced with severe cash flow shortages leading to increasing la ...

Grant versus Loans: from ex-ante to ex-post

... – Countries that can absorb large inflows and that can sustain higher levels of debt should get loans – Countries that have problems absorbing large inflows and that have debt sustainability problems should get more grants • This is the basic message of Cordella and Ulku (2004) ...

... – Countries that can absorb large inflows and that can sustain higher levels of debt should get loans – Countries that have problems absorbing large inflows and that have debt sustainability problems should get more grants • This is the basic message of Cordella and Ulku (2004) ...

Invitation to the Life Span by Kathleen Stassen Berger

... • The power of culture makes it difficult to assess whether adult morality changes with age because changing opinions can be judged as improvements or declines. • The process of moral thinking improves with age. ...

... • The power of culture makes it difficult to assess whether adult morality changes with age because changing opinions can be judged as improvements or declines. • The process of moral thinking improves with age. ...

impact of capping of interest rates

... • When the interest is capped the banks are likely to face two main risks: • Adverse selection as the demand for credit increases, they will not be able to differentiate to between higher risk and lower risk borrowers. The banks therefore charge an aggregated rate which is more attractive to the hig ...

... • When the interest is capped the banks are likely to face two main risks: • Adverse selection as the demand for credit increases, they will not be able to differentiate to between higher risk and lower risk borrowers. The banks therefore charge an aggregated rate which is more attractive to the hig ...

1 Japan`s Financial Countermeasures against the Great East Japan

... insurance policy for those who did not remember whether they were insured or by what insurance company they were insured, and (ii) expedited claim handling by using aerial/satellite photos so as to decide the degree of damage of properties without on-the-spot surveys. — The work of checking aerial/s ...

... insurance policy for those who did not remember whether they were insured or by what insurance company they were insured, and (ii) expedited claim handling by using aerial/satellite photos so as to decide the degree of damage of properties without on-the-spot surveys. — The work of checking aerial/s ...

Chapter 5 Understanding Risk

... Measuring Risk Case 1 An Investment can rise or fall in value. Assume that an asset purchased for $1000 is equally likely to fall to $700 or rise to ...

... Measuring Risk Case 1 An Investment can rise or fall in value. Assume that an asset purchased for $1000 is equally likely to fall to $700 or rise to ...

Slide 1

... • The prices of AAA tranches of securitizations went to levels that were very difficult to explain on the basis of fundamentals • The April 2008 Bank of England Financial Stability Report deduced that prices of these securities at that time implied a 38% loss rate – consistent with a 76% default ra ...

... • The prices of AAA tranches of securitizations went to levels that were very difficult to explain on the basis of fundamentals • The April 2008 Bank of England Financial Stability Report deduced that prices of these securities at that time implied a 38% loss rate – consistent with a 76% default ra ...

11.07.2008 - Erste Bank Analysts: Outlook for insurance markets in

... price/embedded value and price/premium multiples The European insurance industry has – according to the first studies available – not been seriously affected by the financial crisis. The total share of the worldwide insurance industry in the cost of the financial crisis should be around 12%, while t ...

... price/embedded value and price/premium multiples The European insurance industry has – according to the first studies available – not been seriously affected by the financial crisis. The total share of the worldwide insurance industry in the cost of the financial crisis should be around 12%, while t ...

FINANCIAL POLICY • CO-PAYS ARE DUE AT THE TIME OF

... It is our policy to bill your insurance company for you. However, we need your assistance in keeping us updated regarding any changes to your insurance information. Your policy is a contract between you and your insurance company. You will be responsible for any charges that are not covered by your ...

... It is our policy to bill your insurance company for you. However, we need your assistance in keeping us updated regarding any changes to your insurance information. Your policy is a contract between you and your insurance company. You will be responsible for any charges that are not covered by your ...

Slide 1

... – “High” versus “low” order entrepreneurship: implications . . . • in developing countries there is "an abundance of opportunity for low-order entrepreneuring because so many basic needs are unsatisfied • competition that varies in scope (e.g., international) brings the potential for differing value ...

... – “High” versus “low” order entrepreneurship: implications . . . • in developing countries there is "an abundance of opportunity for low-order entrepreneuring because so many basic needs are unsatisfied • competition that varies in scope (e.g., international) brings the potential for differing value ...

Ngoc Pham (Nathan) Professor Bernstein ECON 1901 November 23, 2015

... the repeal of the Glass-Steagall Act, collateralized mortgage obligations, deregulation of over-thecounter derivatives (e.g. credit default swaps) are considered to have tremendously contributed to the housing bubble which was a major cause for the crisis. The crisis can be traced back to the secula ...

... the repeal of the Glass-Steagall Act, collateralized mortgage obligations, deregulation of over-thecounter derivatives (e.g. credit default swaps) are considered to have tremendously contributed to the housing bubble which was a major cause for the crisis. The crisis can be traced back to the secula ...

Personal Finance Economics

... economic growth. Financial investment and real investment are connected, but they are not the same. Thus, when you hear a casual reference to "investment," be clear in your own mind on whether it is financial investment or real investment. SSEPF2 The student will explain that banks and other financi ...

... economic growth. Financial investment and real investment are connected, but they are not the same. Thus, when you hear a casual reference to "investment," be clear in your own mind on whether it is financial investment or real investment. SSEPF2 The student will explain that banks and other financi ...

Personal

... economic growth. Financial investment and real investment are connected, but they are not the same. Thus, when you hear a casual reference to "investment," be clear in your own mind on whether it is financial investment or real investment. SSEPF2 The student will explain that banks and other financi ...

... economic growth. Financial investment and real investment are connected, but they are not the same. Thus, when you hear a casual reference to "investment," be clear in your own mind on whether it is financial investment or real investment. SSEPF2 The student will explain that banks and other financi ...

The Origins of the U.S. Financial and Economic Crises

... even threatened some U.S. financial institutions that had lent to these countries. By their very nature, financial markets are prone to periods of euphoria where lending and speculation expand rapidly (the “boom”), alternating with periods of deep decline (“bust”), when lending collapses. This is be ...

... even threatened some U.S. financial institutions that had lent to these countries. By their very nature, financial markets are prone to periods of euphoria where lending and speculation expand rapidly (the “boom”), alternating with periods of deep decline (“bust”), when lending collapses. This is be ...

Basel II

... banks to make risky investments, such as the subprime mortgage market. Higher risks assets are moved to unregulated parts of holding companies. Alternatively, the risk can be transferred directly to investors by securitization, the process of taking a non-liquid asset or groups of assets and transfo ...

... banks to make risky investments, such as the subprime mortgage market. Higher risks assets are moved to unregulated parts of holding companies. Alternatively, the risk can be transferred directly to investors by securitization, the process of taking a non-liquid asset or groups of assets and transfo ...

Central Bank of Egypt Credit Risk

... able” corporate bonds and a US government bond of comparable maturity. • Spreads between interest rates on various private and public sector debt contain valuable information • Spreads widen during recession and contract during economic expansion • Contracting spreads is a positive sign for markets/ ...

... able” corporate bonds and a US government bond of comparable maturity. • Spreads between interest rates on various private and public sector debt contain valuable information • Spreads widen during recession and contract during economic expansion • Contracting spreads is a positive sign for markets/ ...