British Investment Overseas 1870-1913

... national income. Crafts, on more restrictive assumptions, made it 25 per cent.5 If this indeed was the case, then Britain would have enjoyed a higher standard of living had Victorian investors allocated a larger proportion of their portfolio to domestic issues. To explain why investment abroad was s ...

... national income. Crafts, on more restrictive assumptions, made it 25 per cent.5 If this indeed was the case, then Britain would have enjoyed a higher standard of living had Victorian investors allocated a larger proportion of their portfolio to domestic issues. To explain why investment abroad was s ...

World Selection® Portfolio Growth Portfolio

... The performance data of the HSBC World Selection Portfolio service model portfolios (“Portfolios”) is provided for information purposes only. Performance information is based on the performance of our standard Portfolios and not on a composite of actual client accounts. Past performance of the Portf ...

... The performance data of the HSBC World Selection Portfolio service model portfolios (“Portfolios”) is provided for information purposes only. Performance information is based on the performance of our standard Portfolios and not on a composite of actual client accounts. Past performance of the Portf ...

Pricing of Corporate Loan : Credit Risk and Liquidity cost

... This PhD thesis investigates the pricing of a corporate loan according to the credit risk, the liquidity cost and the embedded prepayment option. When a firm needs money it can turn to its bank which lends it against e.g., periodic payments in a form of a loan. A loan contract issued by a bank for i ...

... This PhD thesis investigates the pricing of a corporate loan according to the credit risk, the liquidity cost and the embedded prepayment option. When a firm needs money it can turn to its bank which lends it against e.g., periodic payments in a form of a loan. A loan contract issued by a bank for i ...

Private Sector Financing and the role of Risk

... Although the rapid GDP growth that occurred in Azerbaijan in the mid‐2000s was primarily driven by the oil sector, it ultimately led to strong growth in all sectors of the economy, benefiting SMEs as well as oil companies. Oil wealth helped mitigate the negative impact of the global fin ...

... Although the rapid GDP growth that occurred in Azerbaijan in the mid‐2000s was primarily driven by the oil sector, it ultimately led to strong growth in all sectors of the economy, benefiting SMEs as well as oil companies. Oil wealth helped mitigate the negative impact of the global fin ...

Guide to Private Equity and Venture Capital for

... as buyouts – that is, partnering with the management team, taking a majority stake and providing capital to buy the business from, for example, a corporate, another private equity house, the public markets or a family owner. At the larger end of the deal spectrum are the global buyout firms, many of ...

... as buyouts – that is, partnering with the management team, taking a majority stake and providing capital to buy the business from, for example, a corporate, another private equity house, the public markets or a family owner. At the larger end of the deal spectrum are the global buyout firms, many of ...

Institutional Investors and Corporate Behavior

... ter 3. Such an exploration can shed light on investor perceptions about these two questions and on how those perceptions might guide empirical research in corporate finance, law, and economics. Academic responses to the questions are mixed. At one level, it is not difficult to imagine why this might ...

... ter 3. Such an exploration can shed light on investor perceptions about these two questions and on how those perceptions might guide empirical research in corporate finance, law, and economics. Academic responses to the questions are mixed. At one level, it is not difficult to imagine why this might ...

Special Purpose Vehicle (SPV) Act (2002)

... Elimination of friction costs: (con’t) exemption of the SPE, which is not considered an FI, from the payment of gross receipts (GRT); exemption from VAT and DST on re-transfer of assets and collateral from the SPE to the Originator or Seller; and exemption from income tax on the yield of the i ...

... Elimination of friction costs: (con’t) exemption of the SPE, which is not considered an FI, from the payment of gross receipts (GRT); exemption from VAT and DST on re-transfer of assets and collateral from the SPE to the Originator or Seller; and exemption from income tax on the yield of the i ...

Pulling the Trigger: Default Option Exercise over the Business Cycle*

... Modification Program (HAMP. Analysis (below) suggests that HAMP loan modification opportunities may have boosted borrower exercise of the default option. This finding is consistent with the n ...

... Modification Program (HAMP. Analysis (below) suggests that HAMP loan modification opportunities may have boosted borrower exercise of the default option. This finding is consistent with the n ...

A Responsible Market for Housing Finance

... • Middle-market borrowers or tenants whose housing needs require secondary market liquidity and long-term finance, both of which can be achieved through a limited government backstop of the mortgage finance marketplace • Higher income and wealthy borrowers and tenants, whose housing needs require ...

... • Middle-market borrowers or tenants whose housing needs require secondary market liquidity and long-term finance, both of which can be achieved through a limited government backstop of the mortgage finance marketplace • Higher income and wealthy borrowers and tenants, whose housing needs require ...

Client Letter Aug 14

... times on above average earnings resulted in high valuations that helped in large fund raising in 2006 to 2008 period by corporate India. 02. The huge capacity expansion undertaken by Corporate India around 2008-2010 based on pre 2008 demand estimates took longer time to get utilised resulting in low ...

... times on above average earnings resulted in high valuations that helped in large fund raising in 2006 to 2008 period by corporate India. 02. The huge capacity expansion undertaken by Corporate India around 2008-2010 based on pre 2008 demand estimates took longer time to get utilised resulting in low ...

impact on the stability of European banks Anissa

... In its recent capital adequacy framework, the Basel Committee assigns market discipline an explicit and crucial role as one of the three “pillars” of capital regulation along with minimum capital requirements and supervisory review of capital adequacy (BIS (1999)). Despite the growing recognition of ...

... In its recent capital adequacy framework, the Basel Committee assigns market discipline an explicit and crucial role as one of the three “pillars” of capital regulation along with minimum capital requirements and supervisory review of capital adequacy (BIS (1999)). Despite the growing recognition of ...

Information Asymmetry and Discretionary Accounting in

... Bid-ask spreads and stock volatility are proxies for equity risk, whereas bond spreads and CDS spreads are indicators for credit risk. As pointed out by Beatty and Liao (2014), the main body of existing literature does not make a distinction between information asymmetry and the signaling hypothesi ...

... Bid-ask spreads and stock volatility are proxies for equity risk, whereas bond spreads and CDS spreads are indicators for credit risk. As pointed out by Beatty and Liao (2014), the main body of existing literature does not make a distinction between information asymmetry and the signaling hypothesi ...

simmons first national corp

... Purchases of premises and equipment, net Proceeds from sale of foreclosed assets held for sale Proceeds from sale of foreclosed assets held for sale, covered by FDIC loss share Proceeds from sale of available-for-sale securities Proceeds from maturities of available-for-sale securities Purchases of ...

... Purchases of premises and equipment, net Proceeds from sale of foreclosed assets held for sale Proceeds from sale of foreclosed assets held for sale, covered by FDIC loss share Proceeds from sale of available-for-sale securities Proceeds from maturities of available-for-sale securities Purchases of ...

May 2003 - Banco de España

... (1) Credit to the private sector, for the purposes of this Report, includes financing to residents and non-residents other than credit institutions and public authorities. It includes both loans and fixed-income securities. (2) Unless otherwise stated, the amounts relate to December 2002 and compari ...

... (1) Credit to the private sector, for the purposes of this Report, includes financing to residents and non-residents other than credit institutions and public authorities. It includes both loans and fixed-income securities. (2) Unless otherwise stated, the amounts relate to December 2002 and compari ...

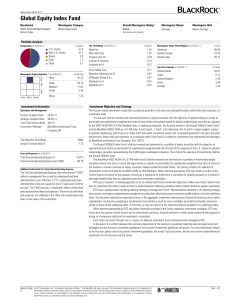

Global Equity Index Fund

... by the MSCI ACWI IMI US $ Net Dividend Index. In seeking its objective, the Account invests in the Russell 3000[rt] Index Fund E and the BlackRock MSCI ACWI ex-U.S. IMI Index Fund E (each, a "Fund", and collectively, the "Funds") in target weights, subject to periodic rebalancing. Each Fund is an "i ...

... by the MSCI ACWI IMI US $ Net Dividend Index. In seeking its objective, the Account invests in the Russell 3000[rt] Index Fund E and the BlackRock MSCI ACWI ex-U.S. IMI Index Fund E (each, a "Fund", and collectively, the "Funds") in target weights, subject to periodic rebalancing. Each Fund is an "i ...

Going Public, Selling Stock, and Buying Liquidity

... declines.14 Thus, underpricing may be intended to hedge against the possibility of litigation under the 1933 Act as a result of extraneous market fluctuations. If so, the problem would seem to be more with the 1933 Act than it is with underwriters.15 Third, underpricing may be used by underwriters a ...

... declines.14 Thus, underpricing may be intended to hedge against the possibility of litigation under the 1933 Act as a result of extraneous market fluctuations. If so, the problem would seem to be more with the 1933 Act than it is with underwriters.15 Third, underpricing may be used by underwriters a ...

BSL 4: Corporate finance

... • Because investing to earn market’s RoE is “produced” differently than investing to beat the market, we should treat them as different markets, or at least different segments of market • Competition for providing market RoE – Entry problem: anyone can make investments with same return (risk-adjuste ...

... • Because investing to earn market’s RoE is “produced” differently than investing to beat the market, we should treat them as different markets, or at least different segments of market • Competition for providing market RoE – Entry problem: anyone can make investments with same return (risk-adjuste ...

203k select - Primary Residential Mortgage

... Documentation needed for Properties which have “rapid appreciation”: The property value must be supported by improvements made to the property, through the following documentation: Verification of improvements, which can include contracts and receipts or, at a minimum, a listing of improvements by ...

... Documentation needed for Properties which have “rapid appreciation”: The property value must be supported by improvements made to the property, through the following documentation: Verification of improvements, which can include contracts and receipts or, at a minimum, a listing of improvements by ...

Nonbanks and Lending Standards in Mortgage Markets. The

... MBS. By law, only loans insured by the U.S. government (FHA, Veterans A¤airs, Rural Development and Public and Indian Housing) can be securitized into a GNMA-backed product. The theory that we test is as follows: 1) The LCR rule has increased demand from the institutions a¤ected by the rule (and fro ...

... MBS. By law, only loans insured by the U.S. government (FHA, Veterans A¤airs, Rural Development and Public and Indian Housing) can be securitized into a GNMA-backed product. The theory that we test is as follows: 1) The LCR rule has increased demand from the institutions a¤ected by the rule (and fro ...

The Origins and Severity of the Public Pension Crisis

... wake of the collapse of the housing bubble led to declines in government revenue of less than 10 percent even in the most hard hit states. Individual investors must also be concerned about market fluctuations since they only retire once. Much of the savings of individual investors are focused on ret ...

... wake of the collapse of the housing bubble led to declines in government revenue of less than 10 percent even in the most hard hit states. Individual investors must also be concerned about market fluctuations since they only retire once. Much of the savings of individual investors are focused on ret ...

Trading Fees and Slow-Moving Capital - Search Faculty

... We endow investors with an every-period motive for trading, over and above the longterm need to trade for lifetime planning purposes.4 Speci…cally, we assume that investors are long-lived and trade because they receive endowments that are not fully hedgeable as, even without trading fees, the market ...

... We endow investors with an every-period motive for trading, over and above the longterm need to trade for lifetime planning purposes.4 Speci…cally, we assume that investors are long-lived and trade because they receive endowments that are not fully hedgeable as, even without trading fees, the market ...

chapter 1 overview of the research thesis

... taking deposits with charge repay and use that money to lend, and of the discount as an intermediary for the payment of the economy. In particular, lending is one of the basic activities of the bank, according to which credit institutions delivered to customers in an amount to be used for the purpos ...

... taking deposits with charge repay and use that money to lend, and of the discount as an intermediary for the payment of the economy. In particular, lending is one of the basic activities of the bank, according to which credit institutions delivered to customers in an amount to be used for the purpos ...

money runs - Giorgia Piacentino

... no way to get liquidity if trade fails. As a result, he sells B’s debt at a discounted price, recovering less than his initial investment. If the horizon mismatch is severe, then this loss from selling at a discount is so likely that C0 is unwilling to lend in the first place. But if B’s debt is dem ...

... no way to get liquidity if trade fails. As a result, he sells B’s debt at a discounted price, recovering less than his initial investment. If the horizon mismatch is severe, then this loss from selling at a discount is so likely that C0 is unwilling to lend in the first place. But if B’s debt is dem ...

Toews

... assets, but were achieved by means of retroactive application of a backtested model that was designed with the benefit of hindsight. The performance results are hypothetical and should not be considered indicative of the skill of the adviser. Material market or economic factors have not been conside ...

... assets, but were achieved by means of retroactive application of a backtested model that was designed with the benefit of hindsight. The performance results are hypothetical and should not be considered indicative of the skill of the adviser. Material market or economic factors have not been conside ...

- PNC.com

... property types. For the year, the FTSE All Equity REIT Index generated a total return of 28.0% while the S&P 500 returned 13.7%. Looking at a 20-year history, REITs have consistently outperformed the S&P 500 while exhibiting only slightly higher volatility, returning an average of 13.5% per year ver ...

... property types. For the year, the FTSE All Equity REIT Index generated a total return of 28.0% while the S&P 500 returned 13.7%. Looking at a 20-year history, REITs have consistently outperformed the S&P 500 while exhibiting only slightly higher volatility, returning an average of 13.5% per year ver ...