Name

... a. If income increases people will purchase more; If income decreases they will purchase less. What type of goods will people buy regardless if their price doubles? a. Necessities What happens to demand if population increase? Why? a. Demand will increase because the number of people needed to cloth ...

... a. If income increases people will purchase more; If income decreases they will purchase less. What type of goods will people buy regardless if their price doubles? a. Necessities What happens to demand if population increase? Why? a. Demand will increase because the number of people needed to cloth ...

ECON-261 Principles of Microeconomics

... The main objectives of the course are to: • Develop an economic way of thinking • Introduce graphical analysis • Introduce the concepts of demand and supply • Introduce the decision-making process regarding the optimal level of output • Identify and distinguish among different market structures Lear ...

... The main objectives of the course are to: • Develop an economic way of thinking • Introduce graphical analysis • Introduce the concepts of demand and supply • Introduce the decision-making process regarding the optimal level of output • Identify and distinguish among different market structures Lear ...

Demand and Supply - Common Sense Economics

... their private advantages as consumers and producers, with almost no direct knowledge of, or interest in, the concerns and circumstances of others, are led to a completely coordinated pattern of decisions by responding to the information contained in market prices. Each consumer decides to consume an ...

... their private advantages as consumers and producers, with almost no direct knowledge of, or interest in, the concerns and circumstances of others, are led to a completely coordinated pattern of decisions by responding to the information contained in market prices. Each consumer decides to consume an ...

Chapter_03_Macro_13e_class_slides

... 1) Investigate and describe consumer behavior 2) Distinguish a change in demand from a change in quantity demanded 3) Investigate and describe firm behavior 4) Distinguish a change in supply from a change in quantity supplied 5) Build a market model and illustrate how equilibrium is reached 6) Demon ...

... 1) Investigate and describe consumer behavior 2) Distinguish a change in demand from a change in quantity demanded 3) Investigate and describe firm behavior 4) Distinguish a change in supply from a change in quantity supplied 5) Build a market model and illustrate how equilibrium is reached 6) Demon ...

Demand PPT 1

... • This saying will be used for 4 different definitions. All you will have to do is fill in the ...

... • This saying will be used for 4 different definitions. All you will have to do is fill in the ...

Market Demand Schedule for DVDs

... Markets An institution or mechanism that brings together buyers and sellers of particular goods and services. This chapter focuses on competitive markets. What is a competitive market? ...

... Markets An institution or mechanism that brings together buyers and sellers of particular goods and services. This chapter focuses on competitive markets. What is a competitive market? ...

What would happen to the price of diamonds if diamonds can be

... Ample supply of the good or service available Prices are reasonable and competitive Good or service must be conveniently located ...

... Ample supply of the good or service available Prices are reasonable and competitive Good or service must be conveniently located ...

Unit 1 Vocabulary

... relationship between the quantity demanded and the price 48. Law of demand: says that a higher price for a good/service, all other things being equal, leads people to demand a smaller quantity of that good/service 49. Change in demand: a shift of the demand curve, which changes the quantity demanded ...

... relationship between the quantity demanded and the price 48. Law of demand: says that a higher price for a good/service, all other things being equal, leads people to demand a smaller quantity of that good/service 49. Change in demand: a shift of the demand curve, which changes the quantity demanded ...

Supply and Market Equilibrium

... 2. “Falling oil prices have caused a sharp decrease in the supply of oil.” Speaking precisely, choose the statement that best describes this quotation. ...

... 2. “Falling oil prices have caused a sharp decrease in the supply of oil.” Speaking precisely, choose the statement that best describes this quotation. ...

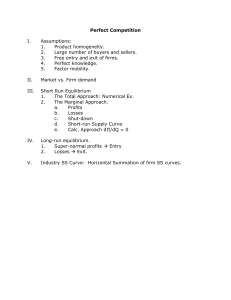

Perfect Competition

... No individual firm or buyer, no matter how large their sales or purchases, can influence market quantity. ...

... No individual firm or buyer, no matter how large their sales or purchases, can influence market quantity. ...

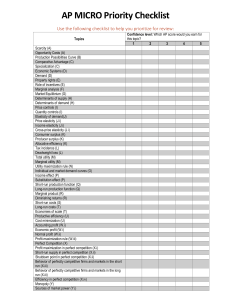

Topic Priority Checklist

... 4. Make a distinction between positive economics and normative economics. 5. List the three basic economic questions. 6. Define comparative advantage and specialization and benefits of exchange. 7. Use a production possibilities curve to demonstrate opportunity cost and growth. 8. List the determina ...

... 4. Make a distinction between positive economics and normative economics. 5. List the three basic economic questions. 6. Define comparative advantage and specialization and benefits of exchange. 7. Use a production possibilities curve to demonstrate opportunity cost and growth. 8. List the determina ...

Liberalism in a Post

... Implication: emphasis must be on shifting the entire demand curve, not just moving along the demand curve. ...

... Implication: emphasis must be on shifting the entire demand curve, not just moving along the demand curve. ...

Supply and demand

In microeconomics, supply and demand is an economic model of price determination in a market. It concludes that in a competitive market, the unit price for a particular good, or other traded item such as labor or liquid financial assets, will vary until it settles at a point where the quantity demanded (at the current price) will equal the quantity supplied (at the current price), resulting in an economic equilibrium for price and quantity transacted.The four basic laws of supply and demand are: If demand increases (demand curve shifts to the right) and supply remains unchanged, a shortage occurs, leading to a higher equilibrium price. If demand decreases (demand curve shifts to the left) and supply remains unchanged, a surplus occurs, leading to a lower equilibrium price. If demand remains unchanged and supply increases (supply curve shifts to the right), a surplus occurs, leading to a lower equilibrium price. If demand remains unchanged and supply decreases (supply curve shifts to the left), a shortage occurs, leading to a higher equilibrium price.↑