Video Information Choices & Change: Microeconomics Economics 1

... potential use of resources in the Gulf of Mexico. Conflicts associated with using and sustaining these resources are also examined. Economic growth in terms of the PPC and the benefits of trade gained from a country’s ability to reach beyond its own production possibilities are illustrated. Lesson 3 ...

... potential use of resources in the Gulf of Mexico. Conflicts associated with using and sustaining these resources are also examined. Economic growth in terms of the PPC and the benefits of trade gained from a country’s ability to reach beyond its own production possibilities are illustrated. Lesson 3 ...

Macroeconomics Topic 8: “Explain how slow price

... (defined as W/P) will rise. The rise in the cost of hiring labor will reduce the quantity of labor demanded. Consequently, employment and real output decrease when the price level rises. Sticky-Price Theory Suppose firms set price at the beginning of each period in anticipation of a certain level of ...

... (defined as W/P) will rise. The rise in the cost of hiring labor will reduce the quantity of labor demanded. Consequently, employment and real output decrease when the price level rises. Sticky-Price Theory Suppose firms set price at the beginning of each period in anticipation of a certain level of ...

Chapter 02 Study Guide

... One of the most significant factors that appears on both lists is the price of the product being considered. This makes it convenient to relate on the same graph the amount demanded and supplied. The relationship of price and consumer’s quantity demanded is inverse, as shown in Figure 2-1, while sup ...

... One of the most significant factors that appears on both lists is the price of the product being considered. This makes it convenient to relate on the same graph the amount demanded and supplied. The relationship of price and consumer’s quantity demanded is inverse, as shown in Figure 2-1, while sup ...

document

... 3. A monopolist does not have a supply curve: because price is determined endogenously by the demand: The monopolist picks a preferred point on the demand curve. Alternative view: the monopolist chooses output to maximize profits subject to the constraint that price be determined by the demand c ...

... 3. A monopolist does not have a supply curve: because price is determined endogenously by the demand: The monopolist picks a preferred point on the demand curve. Alternative view: the monopolist chooses output to maximize profits subject to the constraint that price be determined by the demand c ...

Aggregate Demand and Supply Analysis

... A permanent negative supply shock—such as an increase in ill-advised regulations that causes the economy to be less efficient, thereby reducing supply—would decrease potential output and shift the long-run aggregate supply curve to the left ...

... A permanent negative supply shock—such as an increase in ill-advised regulations that causes the economy to be less efficient, thereby reducing supply—would decrease potential output and shift the long-run aggregate supply curve to the left ...

Time Allowed : 3 Hours Maximum Marks : 100 General Instructions

... 13. What does the law of variable Proportions show? State the behavior of total product according to this law. Or Explain how changes in prices of the products influence the supply of a given product. (4) 14. Explain how do the following influence demand for a good: (i) Rise in income of the consum ...

... 13. What does the law of variable Proportions show? State the behavior of total product according to this law. Or Explain how changes in prices of the products influence the supply of a given product. (4) 14. Explain how do the following influence demand for a good: (i) Rise in income of the consum ...

Intermediate Microeconomic Theory

... Demand Curve – shows how quantity demanded for a given good changes as its price changes, holding other prices and income constant. How do we derive this graphically for good 1 given some set preferences given p2=4 and m=24? ...

... Demand Curve – shows how quantity demanded for a given good changes as its price changes, holding other prices and income constant. How do we derive this graphically for good 1 given some set preferences given p2=4 and m=24? ...

Micro Chapter 7 Study Guide Questions

... 2. Which of the following is true about marginal benefit? a. A consumer's marginal benefit is equal to the height of her demand curve. b. Consumers will continue to purchase up until the point where marginal benefit equals price. c. Marginal benefit declines as consumption increases because of the l ...

... 2. Which of the following is true about marginal benefit? a. A consumer's marginal benefit is equal to the height of her demand curve. b. Consumers will continue to purchase up until the point where marginal benefit equals price. c. Marginal benefit declines as consumption increases because of the l ...

Micro Chapter 7 study guide questions 15e

... 2. Which of the following is true about marginal benefit? a. A consumer's marginal benefit is equal to the height of her demand curve. b. Consumers will continue to purchase up until the point where marginal benefit equals price. c. Marginal benefit declines as consumption increases because of the l ...

... 2. Which of the following is true about marginal benefit? a. A consumer's marginal benefit is equal to the height of her demand curve. b. Consumers will continue to purchase up until the point where marginal benefit equals price. c. Marginal benefit declines as consumption increases because of the l ...

Chapter3

... • A profit-maximizing firm hires workers up to the point where the wage rate equals the value of marginal product of labor. • The demand curve for labor indicates how many workers the firm hires for each possible wage, holding capital constant. • The labor demand curve is downward sloping. This refl ...

... • A profit-maximizing firm hires workers up to the point where the wage rate equals the value of marginal product of labor. • The demand curve for labor indicates how many workers the firm hires for each possible wage, holding capital constant. • The labor demand curve is downward sloping. This refl ...

ECON 1110 Sanders

... Income inelastic – necessity goods where even if you consume more as income goes up, you do not consume them at the same rate ...

... Income inelastic – necessity goods where even if you consume more as income goes up, you do not consume them at the same rate ...

Elastic Demand

... Price Elasticity of Supply Elasticity of Supply• Elasticity of supply shows how sensitive producers are to a change in price. Which supply is more elastic, electricity or pool cleaning? Elasticity of supply is based on time limitations. Some producers need a lot of time to produce more. INelastic = ...

... Price Elasticity of Supply Elasticity of Supply• Elasticity of supply shows how sensitive producers are to a change in price. Which supply is more elastic, electricity or pool cleaning? Elasticity of supply is based on time limitations. Some producers need a lot of time to produce more. INelastic = ...

Product advertising

... A situation that occurs when the quantity supplied and the quantity demanded for a product are equal at the same price. At this equilibrium point, the needs of both producers and consumers are satisfied, and the forces of supply and demand are in balance. ...

... A situation that occurs when the quantity supplied and the quantity demanded for a product are equal at the same price. At this equilibrium point, the needs of both producers and consumers are satisfied, and the forces of supply and demand are in balance. ...

IR‐LWHN‐NLH‐008 NLH 2013 Interim Rates Application Page 1 of 1 Q.

... of the quantity demanded of a good or service to a change in its price. The price ...

... of the quantity demanded of a good or service to a change in its price. The price ...

Demand Curve

... would clear at zero or at shortage prices for very small changes in offered capacity ...

... would clear at zero or at shortage prices for very small changes in offered capacity ...

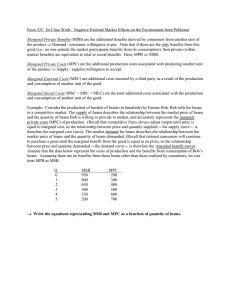

q A 1

... would have been demanded at P1. P2 also signals the typical firm to increase production from q1 to q2. ...

... would have been demanded at P1. P2 also signals the typical firm to increase production from q1 to q2. ...

Supply and demand

In microeconomics, supply and demand is an economic model of price determination in a market. It concludes that in a competitive market, the unit price for a particular good, or other traded item such as labor or liquid financial assets, will vary until it settles at a point where the quantity demanded (at the current price) will equal the quantity supplied (at the current price), resulting in an economic equilibrium for price and quantity transacted.The four basic laws of supply and demand are: If demand increases (demand curve shifts to the right) and supply remains unchanged, a shortage occurs, leading to a higher equilibrium price. If demand decreases (demand curve shifts to the left) and supply remains unchanged, a surplus occurs, leading to a lower equilibrium price. If demand remains unchanged and supply increases (supply curve shifts to the right), a surplus occurs, leading to a lower equilibrium price. If demand remains unchanged and supply decreases (supply curve shifts to the left), a shortage occurs, leading to a higher equilibrium price.↑