presentation source

... differentiated products), new entrants will take away market share from the incumbents • The drop in revenue caused by entry will reduce the economic profit • If there is price competition (where products that are not well differentiated) the market mimics pure competition and the erosion of economi ...

... differentiated products), new entrants will take away market share from the incumbents • The drop in revenue caused by entry will reduce the economic profit • If there is price competition (where products that are not well differentiated) the market mimics pure competition and the erosion of economi ...

Answers to ECMC02 First Test, October 28, 2006

... consumer surplus and producer surplus that originally existed beyond 1000 rides per day are lost to society because of the quota. Therefore, the deadweight loss is (35 – 15) x (2000 – 1000)/2 = $10,000. The correct answer is (D). 5. The new purchasing policy will expand producer surplus, but it will ...

... consumer surplus and producer surplus that originally existed beyond 1000 rides per day are lost to society because of the quota. Therefore, the deadweight loss is (35 – 15) x (2000 – 1000)/2 = $10,000. The correct answer is (D). 5. The new purchasing policy will expand producer surplus, but it will ...

ECON 2010-020 Principles of Microeconomics

... handed in by the date due, your course score will be lowered 1% . If the exercise is not passed by the day of the exam, you will be graded Fail. If you subsequently pass the exercise within 6 months after the final, your grade will be changed to the grade earned in the midterms, the final and the ex ...

... handed in by the date due, your course score will be lowered 1% . If the exercise is not passed by the day of the exam, you will be graded Fail. If you subsequently pass the exercise within 6 months after the final, your grade will be changed to the grade earned in the midterms, the final and the ex ...

Lecture 3 Keynesian Models

... variables are given by the intersection of the IS and LM curves. In other words, the short-run equilibrium is given by the intersection of the IS and the LM curves. Thus, employment can be higher or lower than the full employment level temporarily. The long run equilibrium occurs at the point of the ...

... variables are given by the intersection of the IS and LM curves. In other words, the short-run equilibrium is given by the intersection of the IS and the LM curves. Thus, employment can be higher or lower than the full employment level temporarily. The long run equilibrium occurs at the point of the ...

Ch 8 possibilities, preferences, and choices I. Consumption

... b) The income effect is the effect of a change in income at the new relative price. This effect shifts the budget line outward (with no change in its slope) from the consumption reached by the substitution effect to the highest affordable indifference curve attainable on the new budget line reflecti ...

... b) The income effect is the effect of a change in income at the new relative price. This effect shifts the budget line outward (with no change in its slope) from the consumption reached by the substitution effect to the highest affordable indifference curve attainable on the new budget line reflecti ...

normal good. - Sackville School

... cause a change in the same direction in the demand for the good under study. • Complementary good/service = a good/service in joint demand that is often consumed together. • A change in the price of a complementary good will cause a change in the opposite direction in demand for the good under study ...

... cause a change in the same direction in the demand for the good under study. • Complementary good/service = a good/service in joint demand that is often consumed together. • A change in the price of a complementary good will cause a change in the opposite direction in demand for the good under study ...

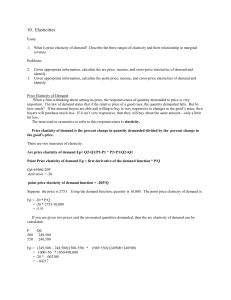

Elasticities - The Citadel

... identify. Given appropriate information, calculate the point price, income, and cross-price elasticities of demand and identify. ...

... identify. Given appropriate information, calculate the point price, income, and cross-price elasticities of demand and identify. ...

AP Micro Review Powerpoint

... The Basic Determinants of Demand are: 1) consumer tastes and preferences 2) number of consumers in the market 3) consumers’ money incomes 4) prices of related goods 5) consumer expectations about future prices and incomes ...

... The Basic Determinants of Demand are: 1) consumer tastes and preferences 2) number of consumers in the market 3) consumers’ money incomes 4) prices of related goods 5) consumer expectations about future prices and incomes ...

AP Micro Review Powerpoint

... The Basic Determinants of Demand are: 1) consumer tastes and preferences 2) number of consumers in the market 3) consumers’ money incomes 4) prices of related goods 5) consumer expectations about future prices and incomes ...

... The Basic Determinants of Demand are: 1) consumer tastes and preferences 2) number of consumers in the market 3) consumers’ money incomes 4) prices of related goods 5) consumer expectations about future prices and incomes ...

Supply and demand

In microeconomics, supply and demand is an economic model of price determination in a market. It concludes that in a competitive market, the unit price for a particular good, or other traded item such as labor or liquid financial assets, will vary until it settles at a point where the quantity demanded (at the current price) will equal the quantity supplied (at the current price), resulting in an economic equilibrium for price and quantity transacted.The four basic laws of supply and demand are: If demand increases (demand curve shifts to the right) and supply remains unchanged, a shortage occurs, leading to a higher equilibrium price. If demand decreases (demand curve shifts to the left) and supply remains unchanged, a surplus occurs, leading to a lower equilibrium price. If demand remains unchanged and supply increases (supply curve shifts to the right), a surplus occurs, leading to a lower equilibrium price. If demand remains unchanged and supply decreases (supply curve shifts to the left), a shortage occurs, leading to a higher equilibrium price.↑