Joffe - Post Keynesian Study Group

... • price setting is thus highly dependent on what information is available • commonly this is trend extrapolation ...

... • price setting is thus highly dependent on what information is available • commonly this is trend extrapolation ...

ANSWER - Harper College

... B. upsloping because successive units of a specific product yield less and less extra utility. C. downsloping because of increasing marginal opportunity costs. D. downsloping because successive units of a specific product yield less and less extra utility. 10. The output of MP3 players should be: A. ...

... B. upsloping because successive units of a specific product yield less and less extra utility. C. downsloping because of increasing marginal opportunity costs. D. downsloping because successive units of a specific product yield less and less extra utility. 10. The output of MP3 players should be: A. ...

Lecture 3. Dual-track liberalization and its properties.

... • Consider first the case of limited liberalization (without secondary market). Intuitively, if consumers with willingness to pay below PE were served under the plan, higher than efficient demand will drive the market price upward bringing in inefficient producers. If producers with marginal cost ab ...

... • Consider first the case of limited liberalization (without secondary market). Intuitively, if consumers with willingness to pay below PE were served under the plan, higher than efficient demand will drive the market price upward bringing in inefficient producers. If producers with marginal cost ab ...

Krugman AP Section 11 Notes

... industry it is called a constant cost industry and the long-run supply curve is horizontal • It is probably more realistic to assume an increasing cost industry. Entry of new firms increases the input costs for all firms. • it is also possible for a market to have a downward sloping LRS curve. This ...

... industry it is called a constant cost industry and the long-run supply curve is horizontal • It is probably more realistic to assume an increasing cost industry. Entry of new firms increases the input costs for all firms. • it is also possible for a market to have a downward sloping LRS curve. This ...

Public Finance

... I believe that each baby needs to be securely buckled into a car seat while riding in a car, to be enforced by the government. I believe that each person in a moving car needs a seat belt on, to be enforced by the government. I believe each driver needs liability insurance, to be enforced by the gov ...

... I believe that each baby needs to be securely buckled into a car seat while riding in a car, to be enforced by the government. I believe that each person in a moving car needs a seat belt on, to be enforced by the government. I believe each driver needs liability insurance, to be enforced by the gov ...

Price of Related Products

... Type description here of how the product became innovative and why you would no longer have the demand for the original product ...

... Type description here of how the product became innovative and why you would no longer have the demand for the original product ...

AP Micro 6-2 Public Goods (cont)

... of a good or service that is borne by the producer. Marginal External Benefit (MEC) The cost of producing an additional unit of a good or service that falls on people other than the producer. ...

... of a good or service that is borne by the producer. Marginal External Benefit (MEC) The cost of producing an additional unit of a good or service that falls on people other than the producer. ...

Chapter 13

... opponent's quantity is given, an equilibrium can be seen where the two reaction curves intersect. The final output will be identical for each firm, and the total output will be one-third greater than the output that would have resulted from a single-price profitmaximizing monopolist. Another attempt ...

... opponent's quantity is given, an equilibrium can be seen where the two reaction curves intersect. The final output will be identical for each firm, and the total output will be one-third greater than the output that would have resulted from a single-price profitmaximizing monopolist. Another attempt ...

short-run supply curve

... increases, sugar production becomes profitable in areas where production costs are higher, and as these areas enter the world market, the quantity of sugar supplied increases. The market for apartments is another example of an increasing-cost industry with a positively sloped supply curve. Most comm ...

... increases, sugar production becomes profitable in areas where production costs are higher, and as these areas enter the world market, the quantity of sugar supplied increases. The market for apartments is another example of an increasing-cost industry with a positively sloped supply curve. Most comm ...

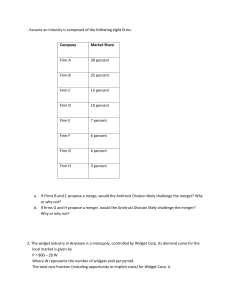

Assume an industry is composed of the following eight firms

... 2. The widget Industry in Anytown is a monopoly, controlled by Widget Corp. Its demand curve for the local market is given by P = 800 – 20 W Where W represents the number of widgets sold per period. The total cost function (including opportunity or implicit costs) for Widget Corp. is ...

... 2. The widget Industry in Anytown is a monopoly, controlled by Widget Corp. Its demand curve for the local market is given by P = 800 – 20 W Where W represents the number of widgets sold per period. The total cost function (including opportunity or implicit costs) for Widget Corp. is ...

chapter 3 - Choose your book for Principles of Economics, by Fred

... 4. An increase in demand causes a. an increase in supply as new firms enter the market b. an increase in price and an increase in supply c. an increase in price and an increase in the quantity supplied d. a decrease in demand in the future e. a decrease in price and an increase in the quantity suppl ...

... 4. An increase in demand causes a. an increase in supply as new firms enter the market b. an increase in price and an increase in supply c. an increase in price and an increase in the quantity supplied d. a decrease in demand in the future e. a decrease in price and an increase in the quantity suppl ...

View/Open

... The identification of social objectives and listing of criteria for assessing contributions of proposed or emerging technologies to those objectives can provide a useful framework for discussing the nature of impacts expected with a new technology. However, if the purpose of the technology assessmen ...

... The identification of social objectives and listing of criteria for assessing contributions of proposed or emerging technologies to those objectives can provide a useful framework for discussing the nature of impacts expected with a new technology. However, if the purpose of the technology assessmen ...

Chopra 2nd Edition, Chapter 2

... seeks to satisfy through its products and services Product development strategy: specifies the portfolio of new products that the company will try to develop Marketing and sales strategy: specifies how the market will be segmented and product positioned, priced, and promoted Supply chain strat ...

... seeks to satisfy through its products and services Product development strategy: specifies the portfolio of new products that the company will try to develop Marketing and sales strategy: specifies how the market will be segmented and product positioned, priced, and promoted Supply chain strat ...

wiki 2.3

... variable costs in the short and long run. In the short run, the fixed costs of the factory and the daily rent are already set therefore the lack of car sales is not affecting those fixed costs. In the long run, the ca manufacturers can take in consideration the decreased number of sales and it can o ...

... variable costs in the short and long run. In the short run, the fixed costs of the factory and the daily rent are already set therefore the lack of car sales is not affecting those fixed costs. In the long run, the ca manufacturers can take in consideration the decreased number of sales and it can o ...

Supply and demand

In microeconomics, supply and demand is an economic model of price determination in a market. It concludes that in a competitive market, the unit price for a particular good, or other traded item such as labor or liquid financial assets, will vary until it settles at a point where the quantity demanded (at the current price) will equal the quantity supplied (at the current price), resulting in an economic equilibrium for price and quantity transacted.The four basic laws of supply and demand are: If demand increases (demand curve shifts to the right) and supply remains unchanged, a shortage occurs, leading to a higher equilibrium price. If demand decreases (demand curve shifts to the left) and supply remains unchanged, a surplus occurs, leading to a lower equilibrium price. If demand remains unchanged and supply increases (supply curve shifts to the right), a surplus occurs, leading to a lower equilibrium price. If demand remains unchanged and supply decreases (supply curve shifts to the left), a shortage occurs, leading to a higher equilibrium price.↑