Document

... Government Policies That Alter the Private Market Outcome • Price controls • Price ceiling: a legal maximum on the price of a good or service Example: rent control • Price floor: a legal minimum on the price of a good or service Example: minimum wage • Taxes • The government can make buyers or sell ...

... Government Policies That Alter the Private Market Outcome • Price controls • Price ceiling: a legal maximum on the price of a good or service Example: rent control • Price floor: a legal minimum on the price of a good or service Example: minimum wage • Taxes • The government can make buyers or sell ...

Figure 6

... Decrease in the number of producers and increased numbers of consumers Decrease in the number of producers and an increase in the price of a substitute good An increase in the price of other goods that could be made by the producer and an increase in the incomes of the consumers of the good in quest ...

... Decrease in the number of producers and increased numbers of consumers Decrease in the number of producers and an increase in the price of a substitute good An increase in the price of other goods that could be made by the producer and an increase in the incomes of the consumers of the good in quest ...

18.2 labor markets

... Can Unions Restrict the Supply of Labor The union’s ability to restrict the supply of labor is limited by how well it can prevent nonunion workers from offering their labor in the same market as union workers. It is difficult for unions to operate in markets where there is an abundant supply of will ...

... Can Unions Restrict the Supply of Labor The union’s ability to restrict the supply of labor is limited by how well it can prevent nonunion workers from offering their labor in the same market as union workers. It is difficult for unions to operate in markets where there is an abundant supply of will ...

Foundations of Economics I: Introduction and Microeconomics

... Economic systems and “Social Market Economy” Consumers decision making and the demand curve Production and cost functions, profit maximization and the supply curve Perfect and imperfect competition, monopoly and monopolistic markets, oligopolies and game theory Government intervention in c ...

... Economic systems and “Social Market Economy” Consumers decision making and the demand curve Production and cost functions, profit maximization and the supply curve Perfect and imperfect competition, monopoly and monopolistic markets, oligopolies and game theory Government intervention in c ...

Calculating the price elasticity of demand

... however some of the general rules include: (Bamford and Munday, 2002) Substitute availability: There is a simple relationship here, greater the substitute greater is the elasticity. For example if we consider butter and margarine, an increase in the price of margarine while the butter remains same c ...

... however some of the general rules include: (Bamford and Munday, 2002) Substitute availability: There is a simple relationship here, greater the substitute greater is the elasticity. For example if we consider butter and margarine, an increase in the price of margarine while the butter remains same c ...

Chapter 11 Economic Change in a Competitive Industry in the

... by a shift from the D 1 to the D 2 curve. The problem we face in this part is to show the effects of this change in the short run and in the long run. The technique of using both short and long run supply curves on the same graph enables us to represent a two-stage adjustment to a change in demand o ...

... by a shift from the D 1 to the D 2 curve. The problem we face in this part is to show the effects of this change in the short run and in the long run. The technique of using both short and long run supply curves on the same graph enables us to represent a two-stage adjustment to a change in demand o ...

ExamView - CH5 short answer for students.tst

... 1. When does a decrease in supply raise the price more: When demand is elastic or when demand is inelastic? When OPEC decreases the supply of oil, the price of gasoline skyrockets. Hence is the demand for gasoline elastic or inelastic? 2. What factors determine the size of the price elasticity of de ...

... 1. When does a decrease in supply raise the price more: When demand is elastic or when demand is inelastic? When OPEC decreases the supply of oil, the price of gasoline skyrockets. Hence is the demand for gasoline elastic or inelastic? 2. What factors determine the size of the price elasticity of de ...

INSTRUCTIONAL PACKAGE

... The Demand Curve Shifts in Demand The Supply Curve and Shifts in Supply Market Equilibrium Market Imbalances (Temporary Surplus and Shortages) Shifts in Equilibrium By the end of this chapter students will be able to: 1. Identify and explain what is meant by a competitive market 2. Identify the non- ...

... The Demand Curve Shifts in Demand The Supply Curve and Shifts in Supply Market Equilibrium Market Imbalances (Temporary Surplus and Shortages) Shifts in Equilibrium By the end of this chapter students will be able to: 1. Identify and explain what is meant by a competitive market 2. Identify the non- ...

Practice Exam for Chapter 14 on Firms in Competitive Markets

... 33) For a firm in a perfectly competitive industry, A) both short-run and long-run economic profits may be negative. B) short-run economic profits must be zero. C) short-run economic profits may be positive, but long-run economic profits must be zero. D) short-run and long-run economic profits must ...

... 33) For a firm in a perfectly competitive industry, A) both short-run and long-run economic profits may be negative. B) short-run economic profits must be zero. C) short-run economic profits may be positive, but long-run economic profits must be zero. D) short-run and long-run economic profits must ...

(考試日期: 節次: 份數: ) 命題老師簽 章:

... a. Calculate profit for each quantity. How much should the firm produce to maximize profit? b. Calculate marginal revenue and marginal cost for each quantity. Graph them. At what quantity do these curves cross? How does this relate to your answer to part(a)? c. Can you tell whether this firm is in a ...

... a. Calculate profit for each quantity. How much should the firm produce to maximize profit? b. Calculate marginal revenue and marginal cost for each quantity. Graph them. At what quantity do these curves cross? How does this relate to your answer to part(a)? c. Can you tell whether this firm is in a ...

Document

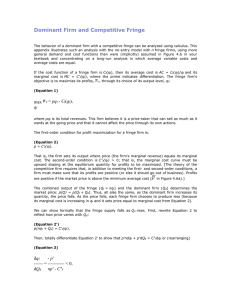

... Solve for Output 950 -2q1 - q2 = 950 - q1 - 2q2 So, q2 = q1 Then plug this into the demand equation we find: 950 - 2q1 - q1 = 950 - 3q1 = 50. Therefore ...

... Solve for Output 950 -2q1 - q2 = 950 - q1 - 2q2 So, q2 = q1 Then plug this into the demand equation we find: 950 - 2q1 - q1 = 950 - 3q1 = 50. Therefore ...

q 2

... Solve for Output 950 -2q1 - q2 = 950 - q1 - 2q2 So, q2 = q1 Then plug this into the demand equation we find: 950 - 2q1 - q1 = 950 - 3q1 = 50. Therefore ...

... Solve for Output 950 -2q1 - q2 = 950 - q1 - 2q2 So, q2 = q1 Then plug this into the demand equation we find: 950 - 2q1 - q1 = 950 - 3q1 = 50. Therefore ...

###Price, Income and Cross Elasticity

... price change influence the Es. The more rapidly the production cost rises and the less time elapses since a price change, the more inelastic the supply. The longer the time elapses, more adjustments can be made to the production process, the more elastic the supply. 2. Storage possibilities: Product ...

... price change influence the Es. The more rapidly the production cost rises and the less time elapses since a price change, the more inelastic the supply. The longer the time elapses, more adjustments can be made to the production process, the more elastic the supply. 2. Storage possibilities: Product ...

Natural Resources, the Environment and Economics

... Positive Economics: The study of what is, and how the economy works. Positive analysis in economics is used to forecast the impact of changes in economic policy or economic conditions on such things as production, sales, prices, and income, and to determine who wins and who loses as a result of thos ...

... Positive Economics: The study of what is, and how the economy works. Positive analysis in economics is used to forecast the impact of changes in economic policy or economic conditions on such things as production, sales, prices, and income, and to determine who wins and who loses as a result of thos ...

Shifts of the Supply Curve

... $10 that used to buy ten hamburgers can now buy only eight hamburgers. The higher price reduces your real income, or purchasing power, which has the tendency to induce you to purchase fewer units of the good. The inverse relationship between price and quantity demanded can be shown by a demand sched ...

... $10 that used to buy ten hamburgers can now buy only eight hamburgers. The higher price reduces your real income, or purchasing power, which has the tendency to induce you to purchase fewer units of the good. The inverse relationship between price and quantity demanded can be shown by a demand sched ...

Supply and demand

In microeconomics, supply and demand is an economic model of price determination in a market. It concludes that in a competitive market, the unit price for a particular good, or other traded item such as labor or liquid financial assets, will vary until it settles at a point where the quantity demanded (at the current price) will equal the quantity supplied (at the current price), resulting in an economic equilibrium for price and quantity transacted.The four basic laws of supply and demand are: If demand increases (demand curve shifts to the right) and supply remains unchanged, a shortage occurs, leading to a higher equilibrium price. If demand decreases (demand curve shifts to the left) and supply remains unchanged, a surplus occurs, leading to a lower equilibrium price. If demand remains unchanged and supply increases (supply curve shifts to the right), a surplus occurs, leading to a lower equilibrium price. If demand remains unchanged and supply decreases (supply curve shifts to the left), a shortage occurs, leading to a higher equilibrium price.↑