Document

... When we combine consumer surplus with the aggregate profits that producers obtain, we can evaluate both the costs and benefits not only of alternative market structures, but of public policies that alter the behavior of consumers and firms in those markets. ...

... When we combine consumer surplus with the aggregate profits that producers obtain, we can evaluate both the costs and benefits not only of alternative market structures, but of public policies that alter the behavior of consumers and firms in those markets. ...

12455_marshallian

... Limitations of the Law • It assumes money can be measurable in money terms. • Commodities are independent and utilities are also independent. • It is assumed consumer has perfect knowledge of the market. • There is no budget period. • It assumes prices are given and constant. • When commodities are ...

... Limitations of the Law • It assumes money can be measurable in money terms. • Commodities are independent and utilities are also independent. • It is assumed consumer has perfect knowledge of the market. • There is no budget period. • It assumes prices are given and constant. • When commodities are ...

Ch 8 possibilities, preferences, and choices I. Consumption

... b) If the negative income effect is stronger than the substitution effect, then a lower (higher) price for an inferior good does not lead to an increase (decrease) in the quantity of that good demanded. c) ...

... b) If the negative income effect is stronger than the substitution effect, then a lower (higher) price for an inferior good does not lead to an increase (decrease) in the quantity of that good demanded. c) ...

Chapter 3: Where Prices Come From: The Interaction of Demand

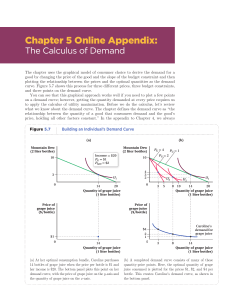

... product demanded. Quantity demanded The amount of a good or service that a consumer is willing and able to purchase at a given price. Demand curve A curve that shows the relationship between the price of a product and the quantity of the product demanded. Market demand The demand by all the consumer ...

... product demanded. Quantity demanded The amount of a good or service that a consumer is willing and able to purchase at a given price. Demand curve A curve that shows the relationship between the price of a product and the quantity of the product demanded. Market demand The demand by all the consumer ...

mish_5ce_ch05

... a rise in interest rates in response to the rise in the price level • The expected-inflation effect of an increase in the money supply is a rise in interest rates in response to the rise in the expected inflation rate ...

... a rise in interest rates in response to the rise in the price level • The expected-inflation effect of an increase in the money supply is a rise in interest rates in response to the rise in the expected inflation rate ...

Chapter 14: Monopolistic Competition and Oligopoly:

... Economic profits will not last due to easy entry/exit. Where a monopoly market has barriers to entry, a monopolistically competitive market does not. Therefore we should expect any economic profit to be reduced to zero due to entry of new ...

... Economic profits will not last due to easy entry/exit. Where a monopoly market has barriers to entry, a monopolistically competitive market does not. Therefore we should expect any economic profit to be reduced to zero due to entry of new ...

Chapter 9 Nontariff Barriers and the New Protectionism

... price elasticities of demand vary across countries. If domestic consumers generally prefer local goods (home-market bias) then the price elasticity of demand will be lower in local markets than in foreign markets. This produces an interesting pattern of international prices. An exporting nation will ...

... price elasticities of demand vary across countries. If domestic consumers generally prefer local goods (home-market bias) then the price elasticity of demand will be lower in local markets than in foreign markets. This produces an interesting pattern of international prices. An exporting nation will ...

Demand and Supply Applications

... FIGURE 4.6 Market Demand and Consumer Surplus As illustrated in (a), some consumers (see point A) are willing to pay as much as $5.00 each for hamburgers. Since the market price is just $2.50, they receive a consumer surplus of $2.50 for each hamburger that they consume. Others (see point B) are w ...

... FIGURE 4.6 Market Demand and Consumer Surplus As illustrated in (a), some consumers (see point A) are willing to pay as much as $5.00 each for hamburgers. Since the market price is just $2.50, they receive a consumer surplus of $2.50 for each hamburger that they consume. Others (see point B) are w ...

Chapter

... directly • The higher the price, the more elastic is demand • The lower the price, the less elastic is demand ...

... directly • The higher the price, the more elastic is demand • The lower the price, the less elastic is demand ...

short-run supply curve

... costs are higher, and as these areas enter the world market, the quantity of sugar supplied increases. The market for apartments is another example of an increasing-cost industry with a positively sloped supply curve. Most communities use zoning laws to restrict the amount of land available for apar ...

... costs are higher, and as these areas enter the world market, the quantity of sugar supplied increases. The market for apartments is another example of an increasing-cost industry with a positively sloped supply curve. Most communities use zoning laws to restrict the amount of land available for apar ...

Economics, Krugman Wells

... $550 per ticket and students willing to pay $150 per ticket. There are 2,000 of each kind of customer. Air Sunshine has constant marginal cost of $125 per seat. If Air Sunshine could charge these two types of customers different prices, it would maximize its profit by charging business travelers $55 ...

... $550 per ticket and students willing to pay $150 per ticket. There are 2,000 of each kind of customer. Air Sunshine has constant marginal cost of $125 per seat. If Air Sunshine could charge these two types of customers different prices, it would maximize its profit by charging business travelers $55 ...

Document

... The short-run industry supply curve is the horizontal sum of all firms’ short-run supply curves horizontal summation of the firm level marginal cost curves At a price below p, no output is supplied. At a price of p, each of the three firms supplies 10 units, for a market supply of 30 units, and at ...

... The short-run industry supply curve is the horizontal sum of all firms’ short-run supply curves horizontal summation of the firm level marginal cost curves At a price below p, no output is supplied. At a price of p, each of the three firms supplies 10 units, for a market supply of 30 units, and at ...

Corn Products

... production decision should compare each farm’s gain (contribution margin) with the opportunity cost of production ...

... production decision should compare each farm’s gain (contribution margin) with the opportunity cost of production ...

Profit Maximization

... demand curve. A monopoly can command any price or set any level of quantity so long as it meets demand, but the most efficient point of operation will be at the point where MR=MC. Price will generally be set higher, however. The monopolist will restrict output in order to maximize profit. By keeping ...

... demand curve. A monopoly can command any price or set any level of quantity so long as it meets demand, but the most efficient point of operation will be at the point where MR=MC. Price will generally be set higher, however. The monopolist will restrict output in order to maximize profit. By keeping ...

Document

... competition, or by taking over the monopoly and running it. Due to problems with each of these options, the best option may be to take no action. ...

... competition, or by taking over the monopoly and running it. Due to problems with each of these options, the best option may be to take no action. ...

Economic equilibrium

In economics, economic equilibrium is a state where economic forces such as supply and demand are balanced and in the absence of external influences the (equilibrium) values of economic variables will not change. For example, in the standard text-book model of perfect competition, equilibrium occurs at the point at which quantity demanded and quantity supplied are equal. Market equilibrium in this case refers to a condition where a market price is established through competition such that the amount of goods or services sought by buyers is equal to the amount of goods or services produced by sellers. This price is often called the competitive price or market clearing price and will tend not to change unless demand or supply changes and the quantity is called ""competitive quantity"" or market clearing quantity.