Homework Answers Chapters 23, 3, and 27 Chapter 23 Questions 1

... Why was inflation kept within bounds? For the same reason that it got off to a slow start in the Unites States during World War II. Necessities were rationed and luxury goods were not easily available. Millions of men were at the front and not in the market for goods. Civilians worked hard and had l ...

... Why was inflation kept within bounds? For the same reason that it got off to a slow start in the Unites States during World War II. Necessities were rationed and luxury goods were not easily available. Millions of men were at the front and not in the market for goods. Civilians worked hard and had l ...

(a) Firm - Econ101-s13-Horn

... before those with higher costs. • Further increases in P make it worthwhile for higher-cost firms to enter the market, which increases market quantity supplied. • Hence, LR market supply curve slopes upward. • At any P, • For the marginal firm, P = minimum ATC and profit = 0. • For lower-cost firms, ...

... before those with higher costs. • Further increases in P make it worthwhile for higher-cost firms to enter the market, which increases market quantity supplied. • Hence, LR market supply curve slopes upward. • At any P, • For the marginal firm, P = minimum ATC and profit = 0. • For lower-cost firms, ...

A numerical example of the effects of an export subsidy

... curves, and no stocks or externalities. ...

... curves, and no stocks or externalities. ...

The McGraw-Hill Series Managerial Economics

... • Assume consumers have complete information about availability, prices, & utility levels of all goods & services • All bundles of goods can be ranked based on their ability to provide utility – for any pair of bundles A & B: • Prefer bundle A to bundle B • Prefer bundle B to bundle A • Indifferent ...

... • Assume consumers have complete information about availability, prices, & utility levels of all goods & services • All bundles of goods can be ranked based on their ability to provide utility – for any pair of bundles A & B: • Prefer bundle A to bundle B • Prefer bundle B to bundle A • Indifferent ...

Chapter - McGraw Hill Higher Education

... • Assume consumers have complete information about availability, prices, & utility levels of all goods & services • All bundles of goods can be ranked based on their ability to provide utility – for any pair of bundles A & B: • Prefer bundle A to bundle B • Prefer bundle B to bundle A • Indifferent ...

... • Assume consumers have complete information about availability, prices, & utility levels of all goods & services • All bundles of goods can be ranked based on their ability to provide utility – for any pair of bundles A & B: • Prefer bundle A to bundle B • Prefer bundle B to bundle A • Indifferent ...

Chapter 4.1 Notes

... Substitution Effect/Income Effect • The law of demand is the result of two separate patterns of behavior we all experience. – Substitution Effect – Income Effect ...

... Substitution Effect/Income Effect • The law of demand is the result of two separate patterns of behavior we all experience. – Substitution Effect – Income Effect ...

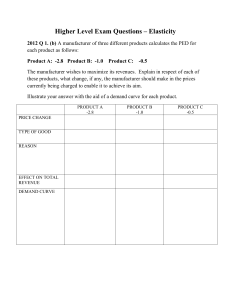

Inelastic Elastic Unit elastic 0 1 2 3

... than the total expenditure of $100,000/hr that occurred under the $1 toll. Example 8.4. Now suppose that the price elasticity had been not 2.0 but 0.5. How would the number of trips and total expenditure then be affected by a 10 percent increase in the toll? This time the number of trips will fall b ...

... than the total expenditure of $100,000/hr that occurred under the $1 toll. Example 8.4. Now suppose that the price elasticity had been not 2.0 but 0.5. How would the number of trips and total expenditure then be affected by a 10 percent increase in the toll? This time the number of trips will fall b ...

Chapter 6

... (an input into making gasoline) shifts the supply curve to the left from S 1 to S2. In an unregulated market, the price would have risen from P1 to P2. The price ceiling, however, prevents this from happening. At the binding price ceiling, consumers are willing to buy Q D, but producers of gasoline ...

... (an input into making gasoline) shifts the supply curve to the left from S 1 to S2. In an unregulated market, the price would have risen from P1 to P2. The price ceiling, however, prevents this from happening. At the binding price ceiling, consumers are willing to buy Q D, but producers of gasoline ...

Price Elasticity of Demand

... What is the optimal price to maximize total revenue? Answer: the price at the unit-elastic point. At any higher price – or any lower price – total revenue is ...

... What is the optimal price to maximize total revenue? Answer: the price at the unit-elastic point. At any higher price – or any lower price – total revenue is ...

review mon and after

... A) actions; rivals; reactions B) price changes; total revenue in a positive way; reactions C) actions rarely; rivals; actions D) price increases; total revenue in the long run only; large but not small price changes ...

... A) actions; rivals; reactions B) price changes; total revenue in a positive way; reactions C) actions rarely; rivals; actions D) price increases; total revenue in the long run only; large but not small price changes ...

Study all concepts!

... complements. If the prices of cars rise many people may not buy new cars and the demand for petrol will fall and vice versa. Therefore, if the price of a good rises the demand for its complement will fall and ...

... complements. If the prices of cars rise many people may not buy new cars and the demand for petrol will fall and vice versa. Therefore, if the price of a good rises the demand for its complement will fall and ...

Solution Solution

... a. Bob’s break-even price is $13.83 because this is the minimum average total cost. His shut-down price is $3, the minimum average variable cost, because below that price his revenue does not even cover his variable cost. b. If the price of Blu-rays is $2, the price is below Bob’s shut-down price of ...

... a. Bob’s break-even price is $13.83 because this is the minimum average total cost. His shut-down price is $3, the minimum average variable cost, because below that price his revenue does not even cover his variable cost. b. If the price of Blu-rays is $2, the price is below Bob’s shut-down price of ...

Demand power point

... Changes in consumers incomes affect demand. A normal good is a good that consumers demand more of when their incomes increase. An inferior good is a good that consumers demand less of when their income increases. 2. Population Changes in the size of the population also affects the demand for most pr ...

... Changes in consumers incomes affect demand. A normal good is a good that consumers demand more of when their incomes increase. An inferior good is a good that consumers demand less of when their income increases. 2. Population Changes in the size of the population also affects the demand for most pr ...

to study Chapter 2, Demand and Supply.

... In the very next growing season, farmer Ahmed discovers a new “Speedo” cabbage harvester is available and at a very reasonable price. He used to pay some boys from the nearby village to help pick his crops each year but now he can pick them all by himself using the machine. He estimates that this sa ...

... In the very next growing season, farmer Ahmed discovers a new “Speedo” cabbage harvester is available and at a very reasonable price. He used to pay some boys from the nearby village to help pick his crops each year but now he can pick them all by himself using the machine. He estimates that this sa ...

Elasticity

... Figure 5.2(a) shows a perfectly inelastic demand curve for insulin. Price elasticity of demand is zero. Quantity demanded is fixed; it does not change at all when price changes. Figure 5.2(b) shows a perfectly elastic demand curve facing a wheat farmer. A tiny price increase drives the quantity dema ...

... Figure 5.2(a) shows a perfectly inelastic demand curve for insulin. Price elasticity of demand is zero. Quantity demanded is fixed; it does not change at all when price changes. Figure 5.2(b) shows a perfectly elastic demand curve facing a wheat farmer. A tiny price increase drives the quantity dema ...

solution

... Undershooting occurs if the new short-run exchange rate is initially below its new long-run level. This happens only if the interest rate rises when the money supply rises—that is if GDP goes up so much that R does not fall, but increases. This is unlikely because the reason we tend to think that an ...

... Undershooting occurs if the new short-run exchange rate is initially below its new long-run level. This happens only if the interest rate rises when the money supply rises—that is if GDP goes up so much that R does not fall, but increases. This is unlikely because the reason we tend to think that an ...

Economic Data and the Identification Problem

... The estimation or identification of demand and supply curves is not simple. The approach of producing a scatter-plot of the price-quantity observations and then “connecting the dots” is definitely not the way to do it correctly. This is because, in general, demand and supply curves are often shiftin ...

... The estimation or identification of demand and supply curves is not simple. The approach of producing a scatter-plot of the price-quantity observations and then “connecting the dots” is definitely not the way to do it correctly. This is because, in general, demand and supply curves are often shiftin ...

Economic equilibrium

In economics, economic equilibrium is a state where economic forces such as supply and demand are balanced and in the absence of external influences the (equilibrium) values of economic variables will not change. For example, in the standard text-book model of perfect competition, equilibrium occurs at the point at which quantity demanded and quantity supplied are equal. Market equilibrium in this case refers to a condition where a market price is established through competition such that the amount of goods or services sought by buyers is equal to the amount of goods or services produced by sellers. This price is often called the competitive price or market clearing price and will tend not to change unless demand or supply changes and the quantity is called ""competitive quantity"" or market clearing quantity.