Monopolistic Competition

... Price exceeds marginal cost in LR P=ATC b/c entry/exit Possesses excess capacity Evaluate based upon deadweight loss, consumer surplus ...

... Price exceeds marginal cost in LR P=ATC b/c entry/exit Possesses excess capacity Evaluate based upon deadweight loss, consumer surplus ...

Chapter 23 – Perfect Competition What are the characteristics of

... • Agricultural products (wheat, corn, etc.), metals, stocks, foreign currency, etc. ...

... • Agricultural products (wheat, corn, etc.), metals, stocks, foreign currency, etc. ...

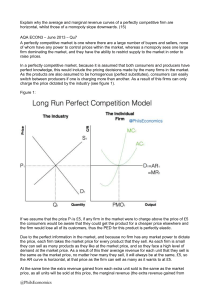

AQA ECON3 – June 2013 – Q7 – Model Answer

... If we assume that the price P1 is £5, if any firm in the market were to charge above the price of £5 the consumers would be aware that they could get the product for a cheaper price elsewhere and the firm would lose all of its customers, thus the PED for this product is perfectly elastic. Due to the ...

... If we assume that the price P1 is £5, if any firm in the market were to charge above the price of £5 the consumers would be aware that they could get the product for a cheaper price elsewhere and the firm would lose all of its customers, thus the PED for this product is perfectly elastic. Due to the ...

Chapter 11 Perfect Competition

... of incumbents, or regulations that inhibit entry or exit. -we don’t assume malicious competition, just firms competing in profit max/costs -we also note that there are not any true examples of perfect competition. Many markets may exhibit many qualities and come close to mimicking it, but it is more ...

... of incumbents, or regulations that inhibit entry or exit. -we don’t assume malicious competition, just firms competing in profit max/costs -we also note that there are not any true examples of perfect competition. Many markets may exhibit many qualities and come close to mimicking it, but it is more ...

Document

... If let to the private market, too little would be produced, not enough resources would be allocated, therefore output would be below the efficient amount. MSB>MSC at the unregulated output MSB>MPB or there is the Free-rider problem. Solutions: Public production of defense, tax to finance production, ...

... If let to the private market, too little would be produced, not enough resources would be allocated, therefore output would be below the efficient amount. MSB>MSC at the unregulated output MSB>MPB or there is the Free-rider problem. Solutions: Public production of defense, tax to finance production, ...

File

... If let to the private market, too little would be produced, not enough resources would be allocated, therefore output would be below the efficient amount. MSB>MSC at the unregulated output MSB>MPB or there is the Free-rider problem. Solutions: Public production of defense, tax to finance production, ...

... If let to the private market, too little would be produced, not enough resources would be allocated, therefore output would be below the efficient amount. MSB>MSC at the unregulated output MSB>MPB or there is the Free-rider problem. Solutions: Public production of defense, tax to finance production, ...

File

... 8. Marginal Cost is the: A) total costs divided by the quantity produced. B) change in fixed cost from producing one additional unit of output. C) market value of all resources used to produce a good. D) change in total cost from producing one additional unit of output. ...

... 8. Marginal Cost is the: A) total costs divided by the quantity produced. B) change in fixed cost from producing one additional unit of output. C) market value of all resources used to produce a good. D) change in total cost from producing one additional unit of output. ...

Slide 1 - McGraw Hill Higher Education - McGraw

... • Marginal revenue (MR) is the change in total revenue that results from a one-unit increase in quantity sold. • Price equals marginal revenue only for perfectly competitive firms. • Marginal revenue is always less than price for a monopolist. ...

... • Marginal revenue (MR) is the change in total revenue that results from a one-unit increase in quantity sold. • Price equals marginal revenue only for perfectly competitive firms. • Marginal revenue is always less than price for a monopolist. ...

Slide 1

... • Why do competitive firms stay in business if they make zero profit? – Profit = total revenue – total cost – Total cost – includes all opportunity costs – Zero-profit equilibrium • Economic profit is zero • Accounting profit is positive ...

... • Why do competitive firms stay in business if they make zero profit? – Profit = total revenue – total cost – Total cost – includes all opportunity costs – Zero-profit equilibrium • Economic profit is zero • Accounting profit is positive ...

Question 1 Economists tend to focus on one structural aspect of

... demand curve for its product to the marketplace. average cost of product in both the short and long run. fixed cost. 4 points Question 6 The shut down condition - the point at which the company finds it is no longer viable to produce and sell a product - for a competitive firm is where price is: Ans ...

... demand curve for its product to the marketplace. average cost of product in both the short and long run. fixed cost. 4 points Question 6 The shut down condition - the point at which the company finds it is no longer viable to produce and sell a product - for a competitive firm is where price is: Ans ...

Quiz1

... Question 1. [5 marks] Suppose the market demand curve for a product is given by Qd=1000-10P and the market supply curve is given by Qs = -50+25P a) [2 marks] What are the equilibrium price and quantity in this market? To find the equilibrium set Qd=Qs 1000-10P=-50+25P P=30 At a price of 30, the mark ...

... Question 1. [5 marks] Suppose the market demand curve for a product is given by Qd=1000-10P and the market supply curve is given by Qs = -50+25P a) [2 marks] What are the equilibrium price and quantity in this market? To find the equilibrium set Qd=Qs 1000-10P=-50+25P P=30 At a price of 30, the mark ...

Monopolies MONOPOLY Pure Monopolies

... Since TR rises while P falls =====> Demand is elastic 2) MR does not equal P as it does in perfect competition MR < P always in a monopolist setting Using these 2 facts, what is the monopolists profit maximizing output? ...

... Since TR rises while P falls =====> Demand is elastic 2) MR does not equal P as it does in perfect competition MR < P always in a monopolist setting Using these 2 facts, what is the monopolists profit maximizing output? ...

Chapter 17 - Effingham County Schools

... Monopolistic vs. Perfect Competition 1. Excess Capacity – firms produce on the downward-sloping portion of ATC, not at efficient scale. Therefore, they could produce more and decrease costs. 2. Markup – P > MC because firm always has some market power, so an extra unit sold = higher profit ...

... Monopolistic vs. Perfect Competition 1. Excess Capacity – firms produce on the downward-sloping portion of ATC, not at efficient scale. Therefore, they could produce more and decrease costs. 2. Markup – P > MC because firm always has some market power, so an extra unit sold = higher profit ...

11extra - U of L Class Index

... A) maintain its current plant size, and other firms will enter the industry. B) increase its plant size, and other firms will exit the industry. C) increase its plant size, and other firms will enter the industry. D) maintain its current plant size, and other firms will exit the industry. E) exit fr ...

... A) maintain its current plant size, and other firms will enter the industry. B) increase its plant size, and other firms will exit the industry. C) increase its plant size, and other firms will enter the industry. D) maintain its current plant size, and other firms will exit the industry. E) exit fr ...

apecon ch9 pure competiton final primer alloc prod lr

... purchased was “valued” by the consumer at $6.00. So MB>MC, society would be better off if more hamburgers were produced and consumed. The last hamburger I produced cost $5 extra and the next consumer (downward sloping Industry Demand Curve) values it at $5.00 MB=MC Graph- equilibrium position—consum ...

... purchased was “valued” by the consumer at $6.00. So MB>MC, society would be better off if more hamburgers were produced and consumed. The last hamburger I produced cost $5 extra and the next consumer (downward sloping Industry Demand Curve) values it at $5.00 MB=MC Graph- equilibrium position—consum ...

Constant cost industry

... firms either exit or adopt the new technology. • Optimal sized firm could be either larger or smaller • Industry supply increases and the industry supply curve shifts rightward. • The price falls and the quantity increases. • Eventually, a new long-run equilibrium emerges in which all the firms us ...

... firms either exit or adopt the new technology. • Optimal sized firm could be either larger or smaller • Industry supply increases and the industry supply curve shifts rightward. • The price falls and the quantity increases. • Eventually, a new long-run equilibrium emerges in which all the firms us ...

chap007Answers

... adding to profits or reducing losses (provided price is not less than minimum AVC). When MC has risen to precise equality with MR, the production of this last (marginal) unit will neither add nor reduce profits. In pure competition, the demand curve is perfectly elastic; price is constant regardless ...

... adding to profits or reducing losses (provided price is not less than minimum AVC). When MC has risen to precise equality with MR, the production of this last (marginal) unit will neither add nor reduce profits. In pure competition, the demand curve is perfectly elastic; price is constant regardless ...

1.3 Choosing to spend

... • When buyers and sellers come together, a market is formed. • For most goods and services, the market price is determined by the amount buyers are willing to pay and the price that businesses need to be paid to cover their costs. • Eventually, the price will settle at a point where supply equals de ...

... • When buyers and sellers come together, a market is formed. • For most goods and services, the market price is determined by the amount buyers are willing to pay and the price that businesses need to be paid to cover their costs. • Eventually, the price will settle at a point where supply equals de ...

Jason Majewski

... produced rises. Fixed costs are costs that do not change when the firm alters the quantity of output produced. Variable costs are costs that do change when the firm alters the quantity of output produced. Average total cost is total cost divided by the quantity of output. Marginal cost is the amou ...

... produced rises. Fixed costs are costs that do not change when the firm alters the quantity of output produced. Variable costs are costs that do change when the firm alters the quantity of output produced. Average total cost is total cost divided by the quantity of output. Marginal cost is the amou ...