Survey

* Your assessment is very important for improving the workof artificial intelligence, which forms the content of this project

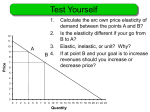

EconS 451: Lecture #7 Producer’s Goal Supply Review • Understand the relationship between average and marginal cost curves and supply (both long-run and short-run). • Be able to calculate the elasticity of supply and understand what values indicate Inelastic and Elastic supply. • Understand the relationship between product price and factor price and the quantity produced of a given product. • Be able to understand those factors which shift (or influence) supply……and how. • Describe the concept of “Supply Response”. • Describe…..in detail how changes in marketing margins impact producers relative to consumers. Max π s.t. Production Technology Profit Maximization Occurs: MR = MC Cost of Revenue / Unit Cost Curves and Supply Cost Curves and Supply Marginal Cost Curve $ Price Short Run Tim e Long Run P2 Average Total Cost P1 Average Variable Cost Q1 Q2 Quantity / Unit Time Quantity / Unit Time Changes in Supply Elasticity Percentage change in Quantity Supplied in response to a 1 percent change in price, all other factors held constant. Es = Es = 0 0 < Es < 1 Es > 1 ∂Q P ∂P Q $ Price Price Elasticity of Supply Perfectly Inelastic Inelastic Supply Elastic Supply Quantity / Unit Time 1 Cost Curves and Supply Factors influencing Supply Input prices • Technology S 1 Original Input Price $ Price • Change in returns from products that compete for productive resources. • S2 Lower Input Price P1 P2 Joint products • • • Soybean / Soybean Meal Lambs / Wool • Price and Yield Risk • Government Intervention Q1 Product – Factor Price Relationship M Px = Input Prices and Supply Factor Price Producer Optimizes Factor Use: • Pfactor Pproduct Quantity / Unit Time Sx P1 P2 D2 Optimum factor use (of input x) will change when relative factor input / product prices change. • D1 X1 X2 Input Prices and Supply Quantity Input X Supply Changes Factor Price • Shift • Parallel shifts from changes such as input costs. Q = α + β P − γX Sx P1 P2 D2 D1 X1 X2 Quantity Input X • Structural Change • Changes in the parameters or functional form (technology, government programs). Q = α + β P − γX 2 2 Supply Response Path Historical Supply Shifts S1 Price Increase Response S2 $ Price $ Price S2 S1 P2 P1 Price Decrease Response P3 P1 P2 Historically, changes in aggregate output have been associated with supply shifts rather than movements along the supply curve. D1 Q1 Q3 Q2 Q1 Quantity / Unit Time Marketing Margin Changes $ Price Quantity Methods for Reducing MM Derived Supply 2 (Retail) RP2 Q2 • Operational Changes • Reduce # of middlemen. • Reduce risk. • Modify marketing structure / organization. • Change laws for unfair trading practices. Derived Supply 1 (Retail) M2 Primary Supply (Farm) RP1 M1 FP1 FP2 • Improve Efficiency • Technological advancements. • # and location of firms. • Economies of size. Primary Demand (Retail) Derived Demand 1 (Farm) Derived Demand 2 (Farm) Q2 Q 1 Quantity / Unit Time Short Run Supply Elasticities Crops Elasticity Livestock Summary Questions • Are agricultural products such as wheat and feed grains generally have inelastic or elastic supply elasticities? • In describing the “supply response”, are the elasticities of supply equal for price increases and decreases? Why? • If output prices drop by 20% and input prices drop by 20%, how much will output change? • At low levels of output, is aggregate (or individual) supply more elastic or inelastic? Why? Elasticity Potatoes .8 Eggs 1.2 Soybeans .5 Poultry Meat .9 Feed Grains .4 Hogs .6 Cotton .4 Beef .5 Tobacco .4 Milk .3 Wheat .3 Fruits .2 3