Survey

* Your assessment is very important for improving the workof artificial intelligence, which forms the content of this project

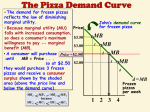

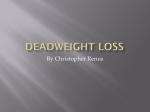

The Pizza Demand Curve • The demand for frozen pizzas reflects the law of diminishing marginal utility. • Because marginal utility (MU) falls with increased consumption, $3.50 so does a consumer’s maximum willingness to pay -- marginal $3.00 benefit (MB). • A consumer will purchase Price =$2.50 $2.50 until MB = Price . . . so at $2.50 $2.00 they would purchase 3 frozen pizzas and receive a consumer surplus shown by the shaded area (above the price line and below the demand curve). MB4 MU4 < MBbecause < MB <MB < MU < MU <MU 3 2 1 3 2 1 John’s demand curve for frozen pizza MB 1 MB MB 2 3 MB 4 d = MB Frozen pizzas per week 1 2 3 4 Consumer Surplus The total difference between what a consumer is willing to pay and how much they actually have to pay. Producer Surplus The total difference between what a supplier is willing to provide a good or service and how much they actually get for it. What Consumer Surplus and Producer Surplus Measure Consumer surplus measures the net benefit to consumers from participating in a market rather than the total benefit. Consumer surplus in a market is equal to the total benefit received by consumers minus the total amount they must pay to buy the good or service. Similarly, producer surplus measures the net benefit received by producers from participating in a market. Producer surplus in a market is equal to the total amount firms receive from consumers minus the cost of producing the good or service. Producer and Consumer Surplus Marginal Cost to Producer equals Marginal Benefit to Consumers P $10 9 8 7 6 5 4 3 2 1 Consumer surplus = area of blue triangle = ½($5)(5) = $12.5 S Producer surplus = area of red triangle = ½($5)(5) = $12.5 CS PS D 0 1 2 3 4 5 6 7 8 Q The combination of producer and consumer surplus is maximized at market equilibrium Inefficiency P $10 9 8 7 6 5 4 3 2 1 At Q = 3, consumers want more, and producers want to supply more S At Q = 8, consumers want less and producers are willing to supply less. CS PS Only at equilibrium are producer and consumer surplus maximized. D 0 1 2 3 4 5 6 7 8 Q Deadweight loss is the reduction in economic surplus resulting from a market not being in competitive equilibrium. Economic surplus is maximized when a market is in competitive equilibrium. When a market is not in equilibrium, there is a deadweight loss. When the price of chai tea is $2.20 instead of $2.00, consumer surplus declines from an amount equal to the sum of areas A, B, and C to just area A. Producer surplus increases from the sum of areas D and E to the sum of areas B and D. At competitive equilibrium, there is no deadweight loss. At a price of $2.20, there is a deadweight loss equal to the sum of areas C and E. Consumer Surplus Price 5 4 3 2 1 2nd 3rd 4th 1st Quantity 1 2 3 4 5 If the selling price is 3, the consumer surplus for the 1st item is 5-3=2, plus 4-3=1 for the 2nd and 3-3=0 for the 3rd, or 3 Government Intervention in the Market: Price Controls 1. Price Floors • Price floor is a legally established minimum price that buyers must pay. • It stops the price from dropping down to equilibrium level. • Example: minimum wage • The direct effect of a price floor above the equilibrium price is a surplus: quantity supplied exceeds quantity demanded. The Impact of a Price Floor Price • A price floor like P1 sets a price above market equilibrium P1 causing quantity supplied QD … S Surplus Price floor to exceed quantity demanded QS P0 … resulting in a surplus. •Non-price factors will become more important than prices in determining where scarce goods go. D QD QS Quantity Minimum Wage Effects • Direct effect: • Reduces employment of low-skilled labor. • Indirect effects: • Reduction in non-wage component of compensation. • Less on-the-job training. • May encourage students to drop out of school • A higher minimum wage does little to help the poor. Employment and the Minimum Wage • If a price (wage) of $4.00 could bring equilibrium. Price (wage) Excess supply • A minimum wage (price floor) $ 5.15 of $5.15 would increase the earnings of those who stayed employed (E1), but would reduce the employment of others. $ 4.00 S Minimum wage level • Those who lose their job (E0 to E1) would be pushed into either unemployment or some other less preferred form of employment. D E1 E0 Quantity (employment) 2. Price Ceilings • Price ceiling is a legally established maximum price that sellers may charge. • It stops the price from rising to the equilibrium level. • Example: rent control • The direct effect of a price ceiling is a shortage: quantity demanded exceeds quantity supplied. The Impact of a Price Ceiling Price (rent) • In the rental housing market the price (rent) P0 would bring the quantity of rental units demanded into balance with the quantity supplied. • A price ceiling like P1sets a price below equilibrium … quantity demanded QD … exceeds quantity supplied QS … resulting in a shortage. S Rental housing market P0 Price ceiling P1 Shortage D QS QD Quantity of housing units Effects of Rent Control • The future supply of housing will decline. • The quality of housing will deteriorate. • Non-price methods of rationing will increase in importance. • Long-term renters will benefit at the expense of newcomers. The Impact of a Tax Tax Incidence • Who pays a tax is called the incidence. Buyer Seller Impact of a Tax Imposed on Sellers Price • If in the used car market a price of $7,000 would bring the quantity of used cars demanded into balance with the quantity supplied. • When a $1,000 tax is imposed on sellers of used cars, the supply curve shifts vertically by the amount of the tax. • The new price for used cars is $7,400 … sellers netting $6,400 ($7,400 - $1000 tax). • Consumers end up paying $7,400 instead of $7,000 and bear $400 of the tax burden. • Sellers end up receiving $6,400 (after taxes) instead of $7000 and bear $600 of the tax burden. S plus tax S $7,400 $7,000 $1000 tax $6,400 D 500 750 # of used cars per month (in thousands) Impact of a Tax Imposed on Buyers Price • In the same used car market: • When a $1,000 tax is imposed on buyers of used cars, the demand curve shifts vertically by the amount of the tax. S $7,400 $7,000 • The new price for used cars is $6,400 … buyers then pay taxes $6,400 of $1000 making the total $7,400. • Consumers end up paying $7,400 (after taxes) instead of $7,000 and bear $400 of the tax burden. • Sellers end up receiving $6,400 instead of $7000 and bear $600 of the tax burden. $1000 tax D D minus tax 500 750 # of used cars per month (in thousands) Elasticity and Incidence of a Tax • The actual burden of a tax depends on the elasticity of supply and demand. • As supply becomes more inelastic, then more of the burden will fall on sellers. • As demand becomes more inelastic, then more of the burden will fall on buyers. Tax Burden and Elasticity • Consider the market for Gasoline and Luxury Boats individually. • We begin in equilibrium. • If we impose a $.20 tax on gasoline suppliers, the supply curve moves vertically the amount of the tax. Price goes up $.15 and output falls by 6 million gallons per week. • If we impose a $25K tax on Luxury Boat suppliers, the supply curve moves vertically the amount of the tax. Price goes up by $5K and output falls by 5 thousand units. • In the gas market, the demand is relatively more inelastic than its supply; hence, buyers bear a larger share of the burden of the tax. • In the luxury boats market, the supply curve is relatively more inelastic than its demand; hence, sellers bear a larger share of the tax burden. Price Gasoline market S plus tax $1.65 $1.60 $1.55 $1.50 $1.45 S D Quantity (millions of gallons) 194 200 Price (thousand $) S plus tax S 110 Luxury boat market 100 90 D 80 Quantity 5 10 15 (thousands 20 of boats) 1. Which of the following is a major disadvantage of setting the price of a good below equilibrium and using waiting in line rather than price to ration the good? a. Compared to price rationing, waiting in line is unfair since it is easier for those with higher incomes to wait in line. b. Waiting in line imposes a cost on the consumer; paying higher prices does not. c. Both waiting in line and higher prices are costly to consumers, but unlike the payment of a higher price, waiting in line does not provide suppliers with an incentive to expand future output. d. Waiting in line benefits consumers at the expense of producers. 2. When a price floor is above the equilibrium price, a. quantity demanded will exceed quantity supplied, so there will be a shortage. b. quantity supplied will exceed quantity demanded, so there will be a surplus. c. the market will be in equilibrium. d. This is a trick question because price floors are generally set below the equilibrium price. 3. Rent control applies to about two-thirds of the private rental housing in New York City. Economic theory suggests that the below-equilibrium prices established by rent controls would a.create a surplus of rental housing. b.promote a rapid increase in the future supply of housing. c. result in poor service and quality deterioration of many rental units. d.lead to a reduction in housing discrimination against minorities. 4. Which of the following is the most likely result of an increase in the minimum wage? a.an increase in the employment of unskilled workers b.a decrease in the number of workers seeking minimum wage jobs c. an increase in the demand for unskilled workers d.a decrease in the employment of unskilled workers 5. The benefit of a subsidy will go primarily to sellers when the a. demand for the product is highly inelastic and supply is relatively elastic. b. demand for the product is highly elastic and the supply is relatively inelastic. c. subsidy is legally (statutorily) granted to the seller of the product. d. subsidy is legally (statutorily) granted to the buyer of the product. 6. If there was an increase in the excise tax imposed on beer suppliers, what would be the effect on the equilibrium price and quantity of beer? a. price increases; quantity decreases b. price decreases; quantity decreases c. price increases; quantity increases d. price decreases; quantity increases 7. The more elastic the supply of a product, the more likely it is that the a. burden of a tax on the product will fall on sellers. b. burden of a tax on the product will fall on buyers. c. burden of a tax on the product will fall equally on both buyers and sellers. d. deadweight loss of the tax will be smaller.